Answered step by step

Verified Expert Solution

Question

1 Approved Answer

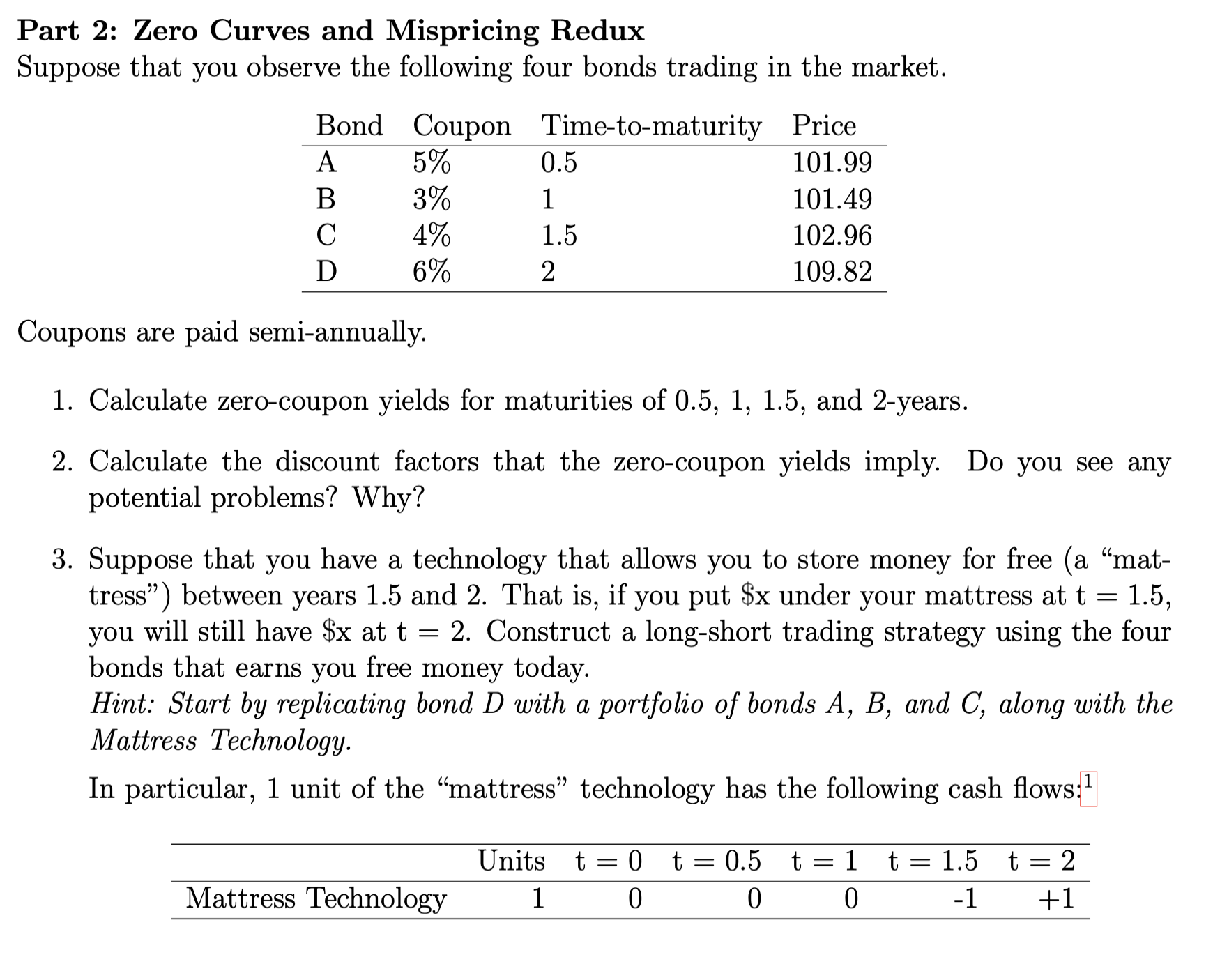

Part 2: Zero Curves and Mispricing Redux Suppose that you observe the following four bonds trading in the market. Coupons are paid semi-annually. 1. Calculate

Part 2: Zero Curves and Mispricing Redux Suppose that you observe the following four bonds trading in the market. Coupons are paid semi-annually. 1. Calculate zero-coupon yields for maturities of 0.5,1,1.5, and 2-years. 2. Calculate the discount factors that the zero-coupon yields imply. Do you see any potential problems? Why? 3. Suppose that you have a technology that allows you to store money for free (a "mattress") between years 1.5 and 2 . That is, if you put $x under your mattress at t=1.5, you will still have $x at t=2. Construct a long-short trading strategy using the four bonds that earns you free money today. Hint: Start by replicating bond D with a portfolio of bonds A,B, and C, along with the Mattress Technology. In particular, 1 unit of the "mattress" technology has the following cash flows: 1

Part 2: Zero Curves and Mispricing Redux Suppose that you observe the following four bonds trading in the market. Coupons are paid semi-annually. 1. Calculate zero-coupon yields for maturities of 0.5,1,1.5, and 2-years. 2. Calculate the discount factors that the zero-coupon yields imply. Do you see any potential problems? Why? 3. Suppose that you have a technology that allows you to store money for free (a "mattress") between years 1.5 and 2 . That is, if you put $x under your mattress at t=1.5, you will still have $x at t=2. Construct a long-short trading strategy using the four bonds that earns you free money today. Hint: Start by replicating bond D with a portfolio of bonds A,B, and C, along with the Mattress Technology. In particular, 1 unit of the "mattress" technology has the following cash flows: 1 Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Business Credit Handbook

Authors: Mr. Reid A. Nunn

1st Edition

1500542725, 978-1500542726