Answered step by step

Verified Expert Solution

Question

1 Approved Answer

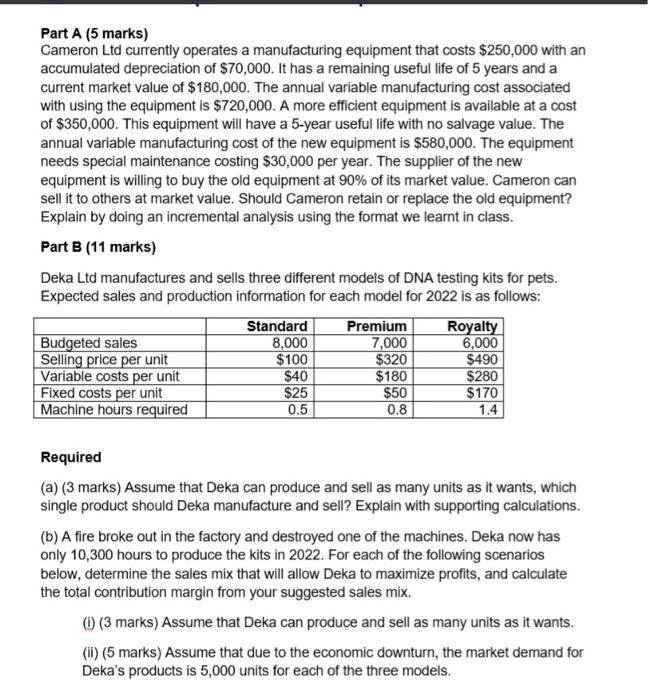

Part A (5 marks) Cameron Ltd currently operates a manufacturing equipment that costs $250,000 with an accumulated depreciation of $70,000. It has a remaining useful

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Designing Cost Management Systems To Support Business Decision-MakingIndustry Inspired Case Studies

Authors: Pieter Buys

1st Edition

9811617503, 9789811617508