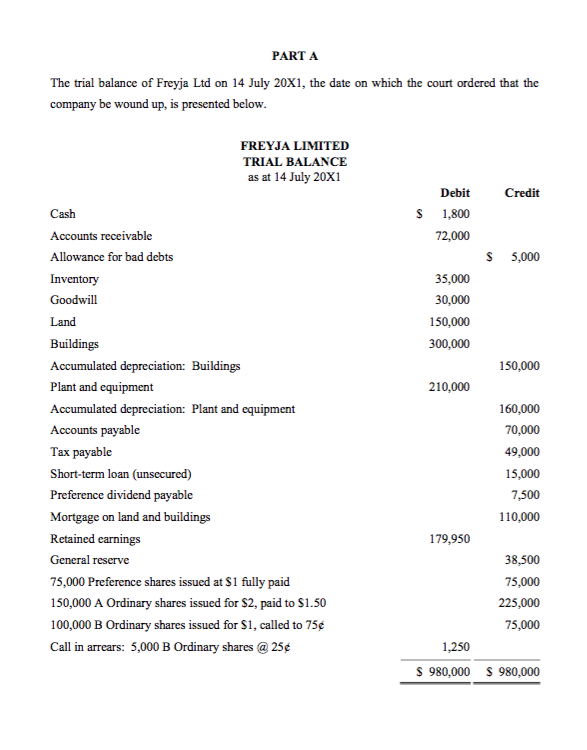

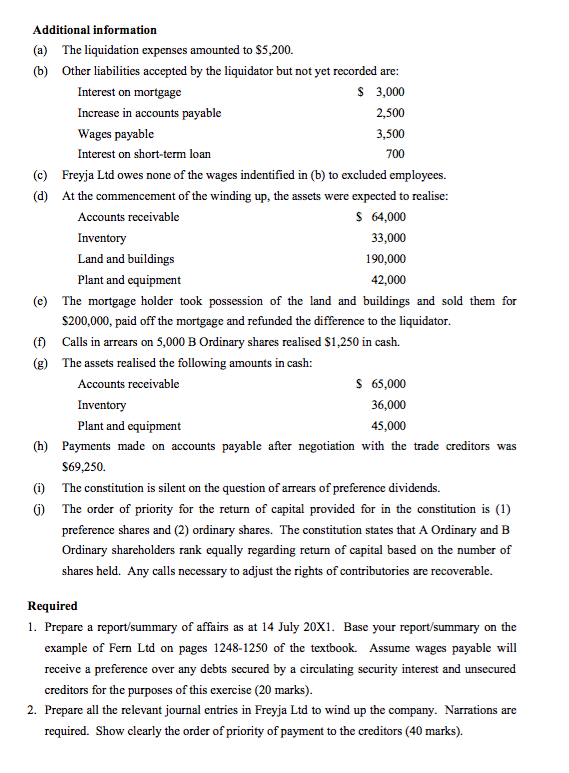

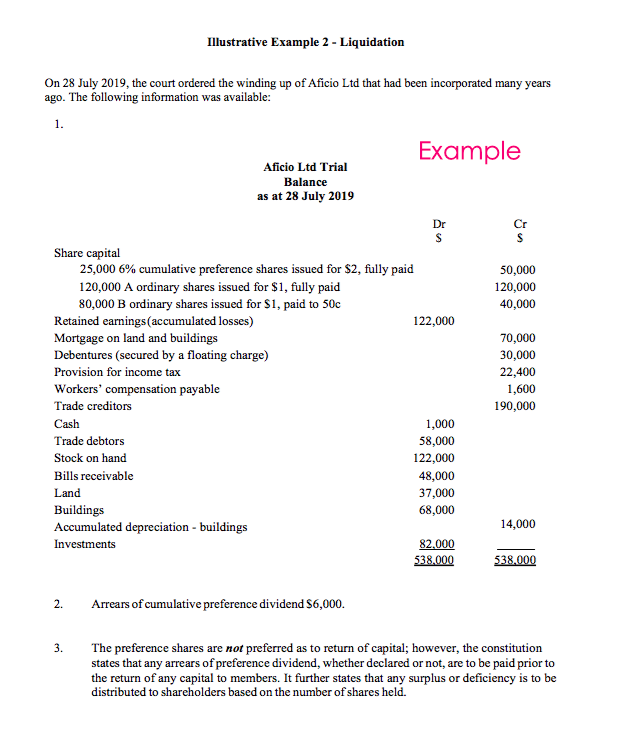

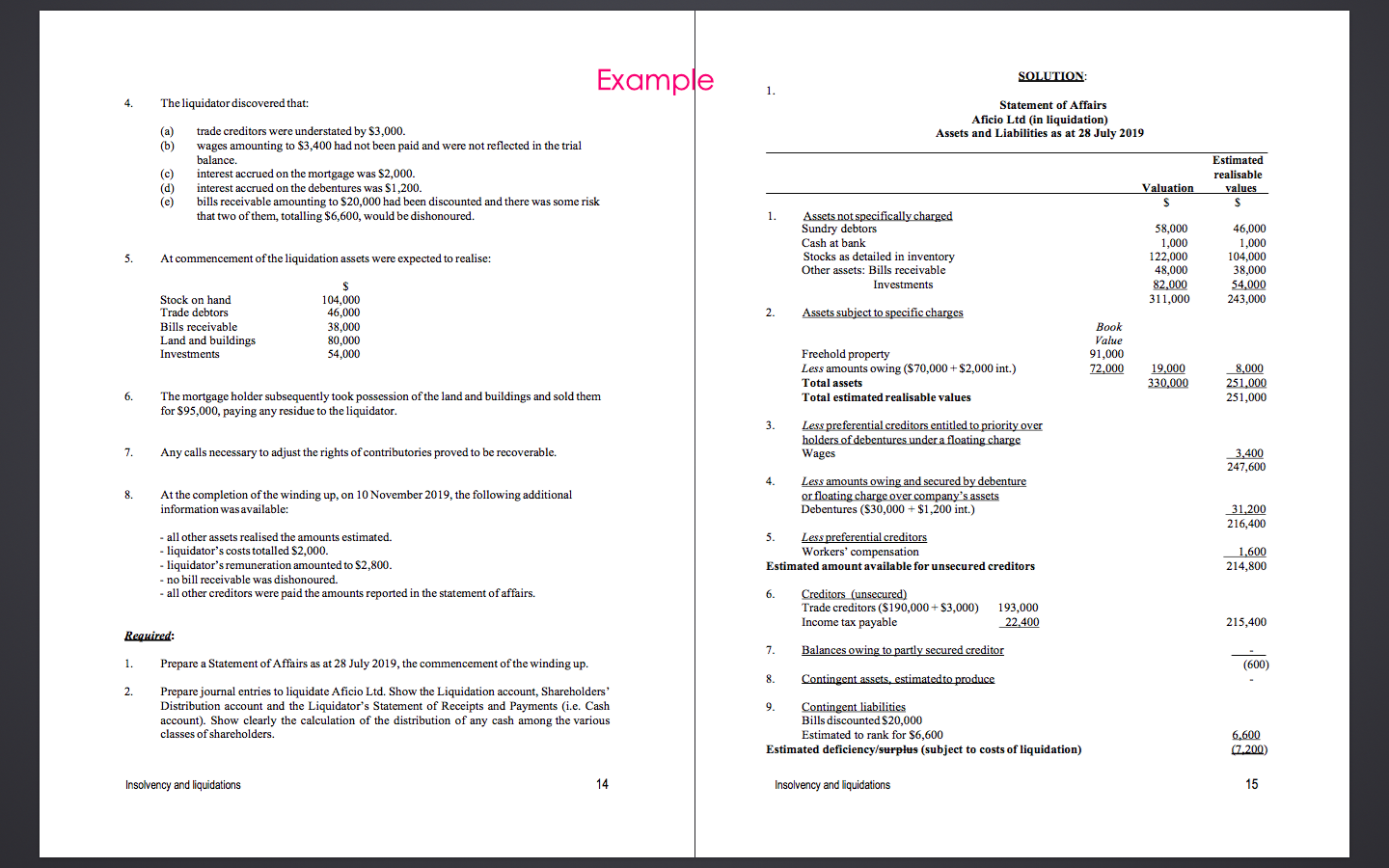

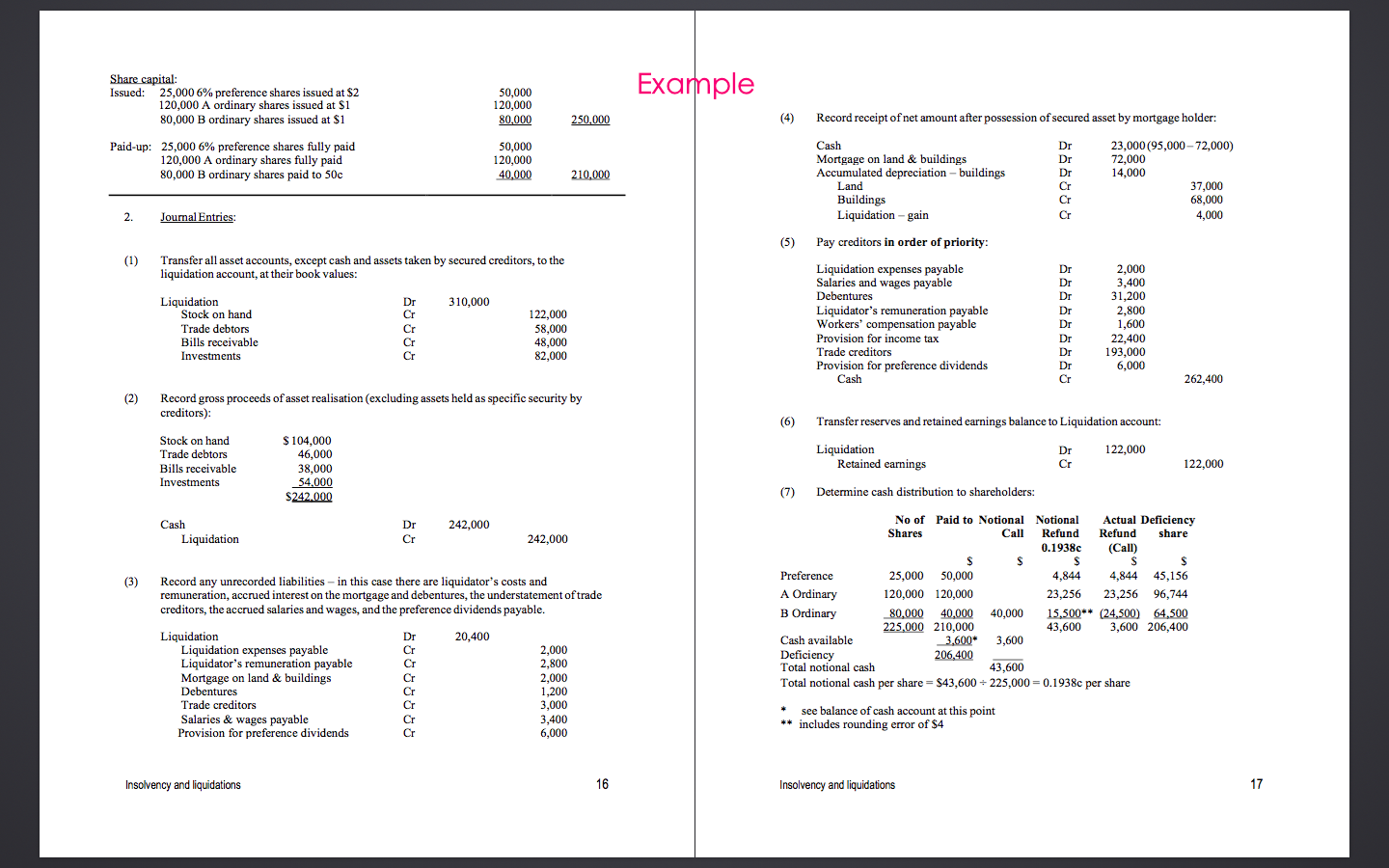

PART A The trial balance of Freyja Ltd on 14 July 20X1, the date on which the court ordered that the company be wound up, is presented below. FREYJA LIMITED TRIAL BALANCE as at 14 July 20x1 $ Cash Accounts receivable Allowance for bad debts Inventory Goodwill Land Buildings Accumulated depreciation: Buildings Plant and equipment Accumulated depreciation: Plant and equipment Accounts payable Tax payable Short-term loan (unsecured) Preference dividend payable Mortgage on land and buildings Retained earnings General reserve 75,000 Preference shares issued at $1 fully paid 150,000 A Ordinary shares issued for $2, paid to $1.50 100,000 B Ordinary shares issued for $1, called to 75 Call in arrears: 5,000 B Ordinary shares @ 25 Debit Credit 1,800 72,000 $ 5,000 35,000 30,000 150,000 300,000 150,000 210,000 160,000 70,000 49,000 15,000 7,500 110,000 179,950 38,500 75,000 225,000 75,000 1,250 $ 980,000 $980,000 Additional information (a) The liquidation expenses amounted to $5,200. (6) Other liabilities accepted by the liquidator but not yet recorded are: Interest on mortgage $ 3,000 Increase in accounts payable 2,500 Wages payable 3,500 Interest on short-term loan 700 c) Freyja Ltd owes none of the wages indentified in (b) to excluded employees. (d) At the commencement of the winding up, the assets were expected to realise: Accounts receivable $ 64,000 Inventory 33,000 Land and buildings 190,000 Plant and equipment 42,000 (e) The mortgage holder took possession of the land and buildings and sold them for $200,000, paid off the mortgage and refunded the difference to the liquidator. (1) Calls in arrears on 5,000 B Ordinary shares realised $1,250 in cash. (g) The assets realised the following amounts in cash: Accounts receivable $ 65,000 Inventory 36,000 Plant and equipment 45,000 (h) Payments made on accounts payable after negotiation with the trade creditors was $69,250. 1) The constitution is silent on the question of arrears of preference dividends. 6) The order of priority for the return of capital provided for in the constitution is (1) preference shares and (2) ordinary shares. The constitution states that A Ordinary and B Ordinary shareholders rank equally regarding return of capital based on the number of shares held. Any calls necessary to adjust the rights of contributories are recoverable. Required 1. Prepare a report/summary of affairs as at 14 July 20X1. Base your report/summary on the example of Fern Ltd on pages 1248-1250 of the textbook. Assume wages payable will receive a preference over any debts secured by a circulating security interest and unsecured creditors for the purposes of this exercise (20 marks). 2. Prepare all the relevant journal entries in Freyja Ltd to wind up the company. Narrations are required. Show clearly the order of priority of payment to the creditors (40 marks). 3. Show clearly any workings in relation to the final distribution to shareholders (20 marks). 4. Prepare the liquidation account, the shareholder's distribution account and liquidator's receipts and payments (cash) account. Show all of the relevant detail in the account entries (i.e. do not aggregate transactions into one amount) (15 marks). Illustrative Example 2 - Liquidation On 28 July 2019, the court ordered the winding up of Aficio Ltd that had been incorporated many years ago. The following information was available: 1. Example Aficio Ltd Trial Balance as at 28 July 2019 Cr S 50,000 120,000 40,000 Dr S Share capital 25,000 6% cumulative preference shares issued for $2, fully paid 120,000 A ordinary shares issued for $1, fully paid 80,000 B ordinary shares issued for $1, paid to 50c Retained earnings (accumulated losses) 122,000 Mortgage on land and buildings Debentures (secured by a floating charge) Provision for income tax Workers' compensation payable Trade creditors Cash 1,000 Trade debtors 58,000 Stock on hand 122,000 Bills receivable 48,000 Land 37,000 Buildings 68,000 Accumulated depreciation - buildings Investments 82.000 538.000 70,000 30,000 22,400 1,600 190,000 14,000 538.000 2. Arrears of cumulative preference dividend $6,000. 3. The preference shares are not preferred as to return of capital; however, the constitution states that any arrears of preference dividend, whether declared or not, are to be paid prior to the return of any capital to members. It further states that any surplus or deficiency is to be distributed to shareholders based on the number of shares held. Example SOLUTION: 1. 4. The liquidator discovered that: Statement of Affairs Aficio Ltd (in liquidation) Assets and Liabilities as at 28 July 2019 (a) (b) (c) (d) (e) trade creditors were understated by $3,000. wages amounting to $3,400 had not been paid and were not reflected in the trial balance, interest accrued on the mortgage was $2,000. interest accrued on the debentures was $1,200. bills receivable amounting to $20,000 had been discounted and there was some risk that two of them, totalling $6,600, would be dishonoured. Estimated realisable values S Valuation S 1. 58,000 1,000 Assets not specifically charged Sundry debtors Cash at bank Stocks as detailed in inventory Other assets: Bills receivable Investments 5. At commencement of the liquidation assets were expected to realise: 122,000 48,000 82,000 311,000 46,000 1,000 104.000 38,000 54.000 243,000 2. $ 104,000 46,000 38.000 80,000 54,000 Stock on hand Trade debtors Bills receivable Land and buildings Investments Assets subject to specific charges Freehold property Less amounts owing ($70,000+$2,000 int.) Total assets Total estimated realisable values Book Value 91,000 72,000 19,000 330,000 8,000 251.000 251,000 6. The mortgage holder subsequently took possession of the land and buildings and sold them for $95,000, paying any residue to the liquidator. 3. Less preferential creditors entitled to priority over holders of debentures under a floating charge Wages 7. Any calls necessary to adjust the rights of contributories proved to be recoverable. 3,400 247,600 8. At the completion of the winding up, on 10 November 2019, the following additional information was available: Less amounts owing and secured by debenture or floating charge over company's assets Debentures ($30,000+ $1,200 int.) 31,200 216,400 all other assets realised the amounts estimated. - liquidator's costs totalled $2,000. - liquidator's remuneration amounted to $2,800. - no bill receivable was dishonoured. - all other creditors were paid the amounts reported in the statement of affairs. 5 5. Less preferential creditors Workers' compensation Estimated amount available for unsecured creditors 1,600 214,800 6. Creditors (unsecured) Trade creditors ($190,000+ $3,000) 193,000 Income tax payable 22.400 215,400 Required: 7. Balances owing to partly secured creditor 1. (600) 8. Contingent assets, estimated to produce 2. Prepare a Statement of Affairs as at 28 July 2019, the commencement of the winding up. Prepare journal entries to liquidate Aficio Ltd. Show the Liquidation account, Shareholders' Distribution account and the Liquidator's Statement of Receipts and Payments (i.e. Cash account). Show clearly the calculation of the distribution of any cash among the various classes of shareholders. 9. Contingent liabilities Bills discounted $20,000 Estimated to rank for $6,600 Estimated deficiency/surplus (subject to costs of liquidation) 6,600 (7.200) Insolvency and liquidations 14 Insolvency and liquidations 15 Share capital: Issued: 25,000 6% preference shares issued at $2 120,000 A ordinary shares issued at $1 80,000 B ordinary shares issued at $1 Example 50,000 120,000 80,000 250,000 (4) Record receipt of net amount after possession of secured asset by mortgage holder: Paid-up: 25,000 6% preference shares fully paid 120,000 A ordinary shares fully paid 80,000 B ordinary shares paid to 50c 50,000 120,000 40,000 210,000 Cash Mortgage on land & buildings Accumulated depreciation - buildings Land Buildings Liquidation -gain Dr Dr Dr Cr Cr Cr 23,000 (95,000-72,000) 72,000 14,000 37,000 68,000 4,000 2. Joumal Entries: (5) (1) Transfer all asset accounts, except cash and assets taken by secured creditors, to the liquidation account, at their book values: 310,000 Liquidation Stock on hand Trade debtors Bills receivable Investments 20000 Cr Cr Cr Cr 122,000 58,000 48,000 82,000 Pay creditors in order of priority: Liquidation expenses payable Salaries and wages payable Debentures Liquidator's remuneration payable Workers' compensation payable Provision for income tax Trade creditors Provision for preference dividends Cash Dr Dr Dr Dr Dr Dr Dr Dr Cr 2,000 3,400 31,200 2,800 1,600 22,400 193,000 6,000 262,400 (2) Record gross proceeds of asset realisation (excluding assets held as specific security by creditors) (6) Transfer reserves and retained earnings balance to Liquidation account: Stock on hand Trade debtors Bills receivable Investments 122,000 $ 104,000 46,000 38,000 54.000 $242.000 Liquidation Retained earnings Dr Cr 122,000 (1) Determine cash distribution to shareholders: Cash Liquidation Dr Cr 242,000 242,000 (3) Record any unrecorded liabilities - in this case there are liquidator's costs and remuneration, accrued interest on the mortgage and debentures, the understatement of trade creditors, the accrued salaries and wages, and the preference dividends payable. No of Paid to Notional Notional Actual Deficiency Shares Call Refund Refund share 0.1938c (Call) $ S $ $ S $ Preference 25,000 50,000 4,844 4,844 45,156 A Ordinary 120,000 120,000 23,256 23,256 96,744 B Ordinary 80,000 40,000 40,000 15,500** (24,500) 64,500 225.000 210.000 43,600 3,600 206,400 Cash available 3,600" 3,600 Deficiency 206,400 Total notional cash 43,600 Total notional cash per share = $43,600 - 225,000 = 0.1938c per share Dr Cr 20,400 Liquidation Liquidation expenses payable Liquidator's remuneration payable Mortgage on land & buildings Debentures Trade creditors Salaries & wages payable Provision for preference dividends Cr Cr Cr Cr Cr 2,000 2,800 2,000 1,200 3,000 3,400 6,000 see balance of cash account at this point ** includes rounding error of $4 Insolvency and liquidations 16 Insolvency and liquidations 17 PART A The trial balance of Freyja Ltd on 14 July 20X1, the date on which the court ordered that the company be wound up, is presented below. FREYJA LIMITED TRIAL BALANCE as at 14 July 20x1 $ Cash Accounts receivable Allowance for bad debts Inventory Goodwill Land Buildings Accumulated depreciation: Buildings Plant and equipment Accumulated depreciation: Plant and equipment Accounts payable Tax payable Short-term loan (unsecured) Preference dividend payable Mortgage on land and buildings Retained earnings General reserve 75,000 Preference shares issued at $1 fully paid 150,000 A Ordinary shares issued for $2, paid to $1.50 100,000 B Ordinary shares issued for $1, called to 75 Call in arrears: 5,000 B Ordinary shares @ 25 Debit Credit 1,800 72,000 $ 5,000 35,000 30,000 150,000 300,000 150,000 210,000 160,000 70,000 49,000 15,000 7,500 110,000 179,950 38,500 75,000 225,000 75,000 1,250 $ 980,000 $980,000 Additional information (a) The liquidation expenses amounted to $5,200. (6) Other liabilities accepted by the liquidator but not yet recorded are: Interest on mortgage $ 3,000 Increase in accounts payable 2,500 Wages payable 3,500 Interest on short-term loan 700 c) Freyja Ltd owes none of the wages indentified in (b) to excluded employees. (d) At the commencement of the winding up, the assets were expected to realise: Accounts receivable $ 64,000 Inventory 33,000 Land and buildings 190,000 Plant and equipment 42,000 (e) The mortgage holder took possession of the land and buildings and sold them for $200,000, paid off the mortgage and refunded the difference to the liquidator. (1) Calls in arrears on 5,000 B Ordinary shares realised $1,250 in cash. (g) The assets realised the following amounts in cash: Accounts receivable $ 65,000 Inventory 36,000 Plant and equipment 45,000 (h) Payments made on accounts payable after negotiation with the trade creditors was $69,250. 1) The constitution is silent on the question of arrears of preference dividends. 6) The order of priority for the return of capital provided for in the constitution is (1) preference shares and (2) ordinary shares. The constitution states that A Ordinary and B Ordinary shareholders rank equally regarding return of capital based on the number of shares held. Any calls necessary to adjust the rights of contributories are recoverable. Required 1. Prepare a report/summary of affairs as at 14 July 20X1. Base your report/summary on the example of Fern Ltd on pages 1248-1250 of the textbook. Assume wages payable will receive a preference over any debts secured by a circulating security interest and unsecured creditors for the purposes of this exercise (20 marks). 2. Prepare all the relevant journal entries in Freyja Ltd to wind up the company. Narrations are required. Show clearly the order of priority of payment to the creditors (40 marks). 3. Show clearly any workings in relation to the final distribution to shareholders (20 marks). 4. Prepare the liquidation account, the shareholder's distribution account and liquidator's receipts and payments (cash) account. Show all of the relevant detail in the account entries (i.e. do not aggregate transactions into one amount) (15 marks). Illustrative Example 2 - Liquidation On 28 July 2019, the court ordered the winding up of Aficio Ltd that had been incorporated many years ago. The following information was available: 1. Example Aficio Ltd Trial Balance as at 28 July 2019 Cr S 50,000 120,000 40,000 Dr S Share capital 25,000 6% cumulative preference shares issued for $2, fully paid 120,000 A ordinary shares issued for $1, fully paid 80,000 B ordinary shares issued for $1, paid to 50c Retained earnings (accumulated losses) 122,000 Mortgage on land and buildings Debentures (secured by a floating charge) Provision for income tax Workers' compensation payable Trade creditors Cash 1,000 Trade debtors 58,000 Stock on hand 122,000 Bills receivable 48,000 Land 37,000 Buildings 68,000 Accumulated depreciation - buildings Investments 82.000 538.000 70,000 30,000 22,400 1,600 190,000 14,000 538.000 2. Arrears of cumulative preference dividend $6,000. 3. The preference shares are not preferred as to return of capital; however, the constitution states that any arrears of preference dividend, whether declared or not, are to be paid prior to the return of any capital to members. It further states that any surplus or deficiency is to be distributed to shareholders based on the number of shares held. Example SOLUTION: 1. 4. The liquidator discovered that: Statement of Affairs Aficio Ltd (in liquidation) Assets and Liabilities as at 28 July 2019 (a) (b) (c) (d) (e) trade creditors were understated by $3,000. wages amounting to $3,400 had not been paid and were not reflected in the trial balance, interest accrued on the mortgage was $2,000. interest accrued on the debentures was $1,200. bills receivable amounting to $20,000 had been discounted and there was some risk that two of them, totalling $6,600, would be dishonoured. Estimated realisable values S Valuation S 1. 58,000 1,000 Assets not specifically charged Sundry debtors Cash at bank Stocks as detailed in inventory Other assets: Bills receivable Investments 5. At commencement of the liquidation assets were expected to realise: 122,000 48,000 82,000 311,000 46,000 1,000 104.000 38,000 54.000 243,000 2. $ 104,000 46,000 38.000 80,000 54,000 Stock on hand Trade debtors Bills receivable Land and buildings Investments Assets subject to specific charges Freehold property Less amounts owing ($70,000+$2,000 int.) Total assets Total estimated realisable values Book Value 91,000 72,000 19,000 330,000 8,000 251.000 251,000 6. The mortgage holder subsequently took possession of the land and buildings and sold them for $95,000, paying any residue to the liquidator. 3. Less preferential creditors entitled to priority over holders of debentures under a floating charge Wages 7. Any calls necessary to adjust the rights of contributories proved to be recoverable. 3,400 247,600 8. At the completion of the winding up, on 10 November 2019, the following additional information was available: Less amounts owing and secured by debenture or floating charge over company's assets Debentures ($30,000+ $1,200 int.) 31,200 216,400 all other assets realised the amounts estimated. - liquidator's costs totalled $2,000. - liquidator's remuneration amounted to $2,800. - no bill receivable was dishonoured. - all other creditors were paid the amounts reported in the statement of affairs. 5 5. Less preferential creditors Workers' compensation Estimated amount available for unsecured creditors 1,600 214,800 6. Creditors (unsecured) Trade creditors ($190,000+ $3,000) 193,000 Income tax payable 22.400 215,400 Required: 7. Balances owing to partly secured creditor 1. (600) 8. Contingent assets, estimated to produce 2. Prepare a Statement of Affairs as at 28 July 2019, the commencement of the winding up. Prepare journal entries to liquidate Aficio Ltd. Show the Liquidation account, Shareholders' Distribution account and the Liquidator's Statement of Receipts and Payments (i.e. Cash account). Show clearly the calculation of the distribution of any cash among the various classes of shareholders. 9. Contingent liabilities Bills discounted $20,000 Estimated to rank for $6,600 Estimated deficiency/surplus (subject to costs of liquidation) 6,600 (7.200) Insolvency and liquidations 14 Insolvency and liquidations 15 Share capital: Issued: 25,000 6% preference shares issued at $2 120,000 A ordinary shares issued at $1 80,000 B ordinary shares issued at $1 Example 50,000 120,000 80,000 250,000 (4) Record receipt of net amount after possession of secured asset by mortgage holder: Paid-up: 25,000 6% preference shares fully paid 120,000 A ordinary shares fully paid 80,000 B ordinary shares paid to 50c 50,000 120,000 40,000 210,000 Cash Mortgage on land & buildings Accumulated depreciation - buildings Land Buildings Liquidation -gain Dr Dr Dr Cr Cr Cr 23,000 (95,000-72,000) 72,000 14,000 37,000 68,000 4,000 2. Joumal Entries: (5) (1) Transfer all asset accounts, except cash and assets taken by secured creditors, to the liquidation account, at their book values: 310,000 Liquidation Stock on hand Trade debtors Bills receivable Investments 20000 Cr Cr Cr Cr 122,000 58,000 48,000 82,000 Pay creditors in order of priority: Liquidation expenses payable Salaries and wages payable Debentures Liquidator's remuneration payable Workers' compensation payable Provision for income tax Trade creditors Provision for preference dividends Cash Dr Dr Dr Dr Dr Dr Dr Dr Cr 2,000 3,400 31,200 2,800 1,600 22,400 193,000 6,000 262,400 (2) Record gross proceeds of asset realisation (excluding assets held as specific security by creditors) (6) Transfer reserves and retained earnings balance to Liquidation account: Stock on hand Trade debtors Bills receivable Investments 122,000 $ 104,000 46,000 38,000 54.000 $242.000 Liquidation Retained earnings Dr Cr 122,000 (1) Determine cash distribution to shareholders: Cash Liquidation Dr Cr 242,000 242,000 (3) Record any unrecorded liabilities - in this case there are liquidator's costs and remuneration, accrued interest on the mortgage and debentures, the understatement of trade creditors, the accrued salaries and wages, and the preference dividends payable. No of Paid to Notional Notional Actual Deficiency Shares Call Refund Refund share 0.1938c (Call) $ S $ $ S $ Preference 25,000 50,000 4,844 4,844 45,156 A Ordinary 120,000 120,000 23,256 23,256 96,744 B Ordinary 80,000 40,000 40,000 15,500** (24,500) 64,500 225.000 210.000 43,600 3,600 206,400 Cash available 3,600" 3,600 Deficiency 206,400 Total notional cash 43,600 Total notional cash per share = $43,600 - 225,000 = 0.1938c per share Dr Cr 20,400 Liquidation Liquidation expenses payable Liquidator's remuneration payable Mortgage on land & buildings Debentures Trade creditors Salaries & wages payable Provision for preference dividends Cr Cr Cr Cr Cr 2,000 2,800 2,000 1,200 3,000 3,400 6,000 see balance of cash account at this point ** includes rounding error of $4 Insolvency and liquidations 16 Insolvency and liquidations 17