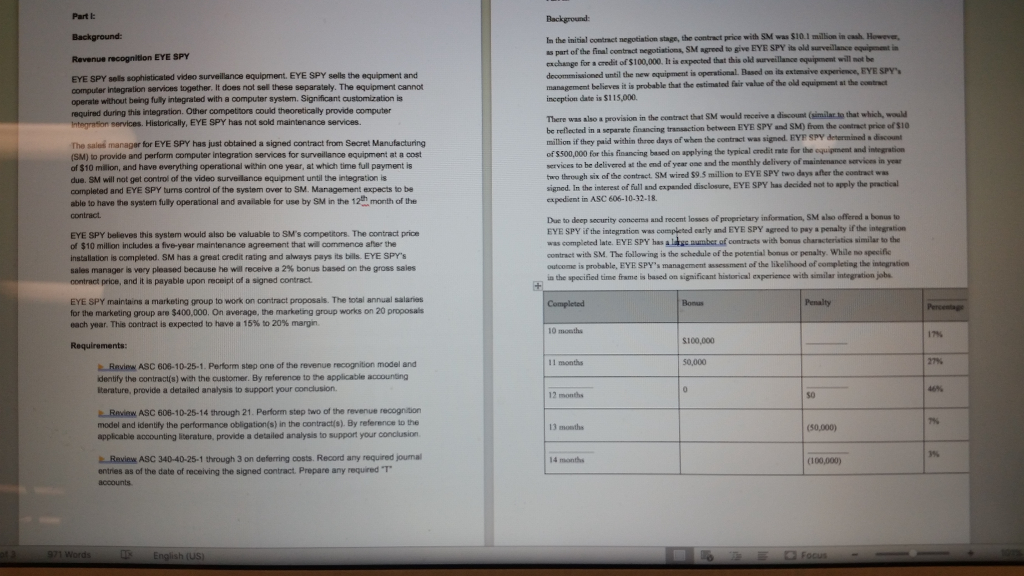

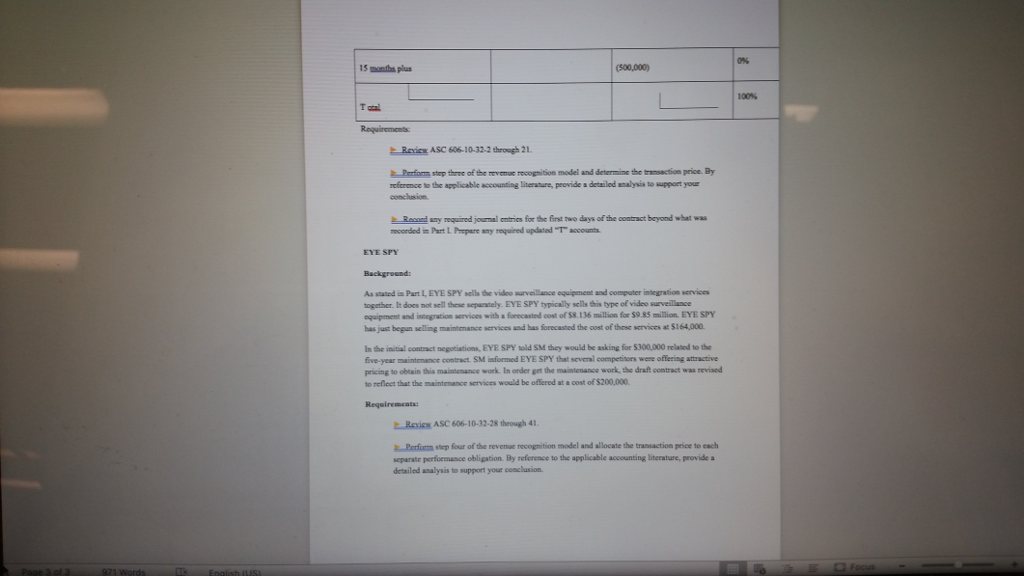

Part b In the initial contract negotiation stage, the contract price with SM was $10.1 million in cash Howeve part ofthe final contract segotiations, SM med to give EYE SPY it. oldlavellan exchange for a credit of $100,000. It is expected that this okd surveillance equipment will ot be Revenue recognition EYE SPY new equipment is operstional. Basod on its extmsive experience, EYE SPY EYE SPY sells sophisticated video surveillance equipment. EYE SPY sells the equipment and computer integration services together. It does not sell these separately. The equipment cannot operate without being fully integrated with a computer system. Significant customization is required during this integration. Other competors could theoretically provide computer ntegrasion services. Historically, EYE SPY has not sold maintenance services. management believes it is probable that the estimated air value of the old equipment st the contract inception date is $115,000 i that SM would receive a discount (similar to that which, would The sale manager for EYE SPY has just obtained a signed contract from Secret Manufacturing (SM) to provide and perform computer integration services for surveillance equipment at a cost of $10 million, and have everything operational within one year, at which time full payment is due. SM will not get control of the video surveilance equipment until the integration is completed and EYE SPY turns control of the system over to SM. Management expects to be able to have the system fully operational and available for use by SM in the 12 month of the be reflected inseparate financing transaction between EYE SPY nd SM) fun, the contract price of$10 million if they paid within throe days of when the contract was signed EYF SPY determined a discount of $500,000 for this financing based on applying the typical credit rate for the equipment and integration services to be delivered at the end of year one and the monthly delivery of maintenance services in year taro therough six of the contract. SM wired $9.5 million to EYE SPY two days after the contract was signed. In the interest of full and expanded disclosure, EYE SPY has decided not to apply the practical expedient in ASC 606-10-32-18. EYE SPY beleves this system would also be valuable to SM's competitors. The contract price of $10 million includes a five-year maintenance agreement that will commence after the installation is completed. SM has a great credit rating and always pays its bills. EYE SPY'S sales manager is very pleased because he will receive a 2% bonus based on the gross sales contract price, and it is payable upon receipt of a signed contract Due to deep security concerma and recent losses of proprietary information, SM also offered a bonus to EYE SPY if the integration was completed early and EYE SPY agreed to pay a penalty if the integration was completed late. EYE SPY ha contract with SM. The following is the schedule of the potential bonus or penalty. While no specific outcome is probable, EYE SPY's management assessment of the likelihood of completing the integration a the specified time frame is based on significant historical experience with similar integration jobs contracts with bonus characteristics similar to the EYE SPY maintains a marketing group to work on contract proposais. The total annual salaries for the marketing group are $400,000. On average, the marketing group works on 20 proposals each year This contract is expected to have a 15% to 20% marr. Percenag 10 months $100,000 11 months .. Revinm ASC 608-10-25-1. Perform step one of the revenue recognition model and dentify the contracts) with the customer. By reference to the applicable accounting terature, provide a detailed analysis to support your conclusion 12 months . Review ASC 606-10-25-14 through 21. Perform step two of the revenue recognition model and identily the performance obligation(s) in the contract(s). By reference to the applicable accounting literature, provide a detailed analysis to support your conclusion 13 months mele* ASC 34040-25-1 through 3 on deferring costs. Record any required journal 0ntres as of the date of receiving the signed contract, prepare any requred "T. 14 month (100,000) Part b In the initial contract negotiation stage, the contract price with SM was $10.1 million in cash Howeve part ofthe final contract segotiations, SM med to give EYE SPY it. oldlavellan exchange for a credit of $100,000. It is expected that this okd surveillance equipment will ot be Revenue recognition EYE SPY new equipment is operstional. Basod on its extmsive experience, EYE SPY EYE SPY sells sophisticated video surveillance equipment. EYE SPY sells the equipment and computer integration services together. It does not sell these separately. The equipment cannot operate without being fully integrated with a computer system. Significant customization is required during this integration. Other competors could theoretically provide computer ntegrasion services. Historically, EYE SPY has not sold maintenance services. management believes it is probable that the estimated air value of the old equipment st the contract inception date is $115,000 i that SM would receive a discount (similar to that which, would The sale manager for EYE SPY has just obtained a signed contract from Secret Manufacturing (SM) to provide and perform computer integration services for surveillance equipment at a cost of $10 million, and have everything operational within one year, at which time full payment is due. SM will not get control of the video surveilance equipment until the integration is completed and EYE SPY turns control of the system over to SM. Management expects to be able to have the system fully operational and available for use by SM in the 12 month of the be reflected inseparate financing transaction between EYE SPY nd SM) fun, the contract price of$10 million if they paid within throe days of when the contract was signed EYF SPY determined a discount of $500,000 for this financing based on applying the typical credit rate for the equipment and integration services to be delivered at the end of year one and the monthly delivery of maintenance services in year taro therough six of the contract. SM wired $9.5 million to EYE SPY two days after the contract was signed. In the interest of full and expanded disclosure, EYE SPY has decided not to apply the practical expedient in ASC 606-10-32-18. EYE SPY beleves this system would also be valuable to SM's competitors. The contract price of $10 million includes a five-year maintenance agreement that will commence after the installation is completed. SM has a great credit rating and always pays its bills. EYE SPY'S sales manager is very pleased because he will receive a 2% bonus based on the gross sales contract price, and it is payable upon receipt of a signed contract Due to deep security concerma and recent losses of proprietary information, SM also offered a bonus to EYE SPY if the integration was completed early and EYE SPY agreed to pay a penalty if the integration was completed late. EYE SPY ha contract with SM. The following is the schedule of the potential bonus or penalty. While no specific outcome is probable, EYE SPY's management assessment of the likelihood of completing the integration a the specified time frame is based on significant historical experience with similar integration jobs contracts with bonus characteristics similar to the EYE SPY maintains a marketing group to work on contract proposais. The total annual salaries for the marketing group are $400,000. On average, the marketing group works on 20 proposals each year This contract is expected to have a 15% to 20% marr. Percenag 10 months $100,000 11 months .. Revinm ASC 608-10-25-1. Perform step one of the revenue recognition model and dentify the contracts) with the customer. By reference to the applicable accounting terature, provide a detailed analysis to support your conclusion 12 months . Review ASC 606-10-25-14 through 21. Perform step two of the revenue recognition model and identily the performance obligation(s) in the contract(s). By reference to the applicable accounting literature, provide a detailed analysis to support your conclusion 13 months mele* ASC 34040-25-1 through 3 on deferring costs. Record any required journal 0ntres as of the date of receiving the signed contract, prepare any requred "T. 14 month (100,000)