Question

Part B - ReportBackgroundCurtainsMaster is a large proprietary company established in North Queensland in the 1990s, selling a wide range of high-quality fabric curtains for

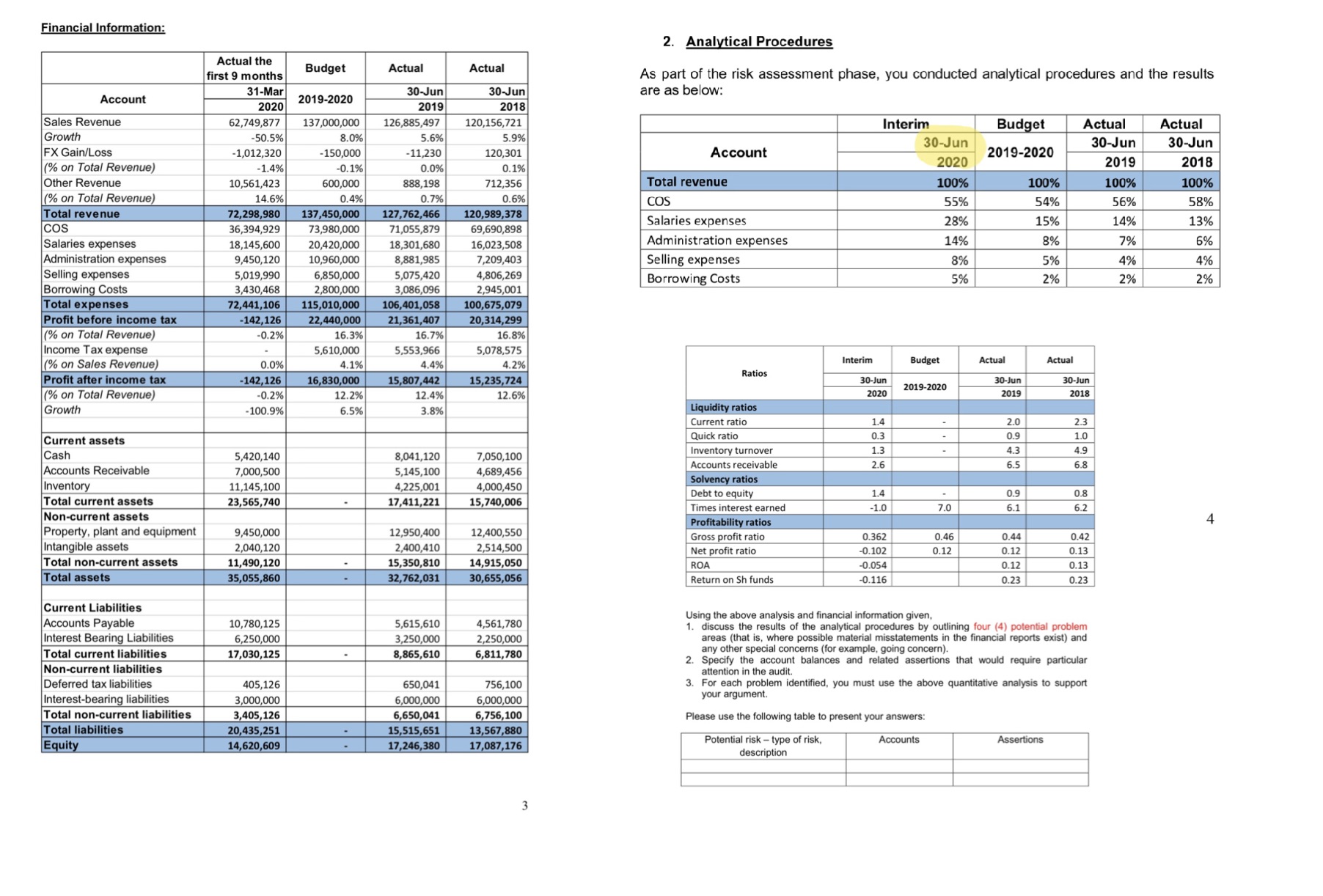

Part B - ReportBackgroundCurtainsMaster is a large proprietary company established in North Queensland in the 1990s, selling a wide range of high-quality fabric curtains for household decoration. The company purchases products from manufactures in Vietnam, Bangladesh, and China, and then sells its products to wholesales customers in Australia, Germany, and the United States. The company also places its products on consignment in various small retail storesin Queensland. Sales mainly peak from the second half of the financial year, generating an average of 60% of revenue for the whole year. In past years the company has performed well, with its profit rate at around 12% and an average increase in annual revenues of 5%.In the last two years, the company has extended its marketing from Germany to other countries in Europe. As a result of this, in the budget for the year 2019-2020, the company while aiming to maintain its profit rate, plans to increase its revenues by 8%. The company uses USD to pay its suppliers and EUR or USD or AUD in its dealings with customers.While the business is expanding in Europe, sales in Australia and US are struggling to reachtheir targets. These markets are quite competitive, providing more affordable products with a large range of designs and choices. Further, in recent years, countries like Vietnam and China have become more eco-conscious, attempting to reduce their industrial impact on the environment. As such, textile manufacturing has been discouraged with strict regulations. Some of CurtainsMaster's suppliers have reduced their production capacity and haveexperienced an increase in production costs. Managing inventory on consignment has been an issue for CurtainsMaster in the past 12 months. On several occasions, the company lost track of their inventory movements and status at the various retail premises. To support the business expansion and strengthen internal controls for inventory, in January 2020 the company installed a new inventory management system on the cloud, which allows inventory movements to be followed up, from production to end-users. The system will also help to follow up and calculate inventory ageing from the day the inventory was entered into the system. In the past five years, old and work-in-progress inventory has piled up due to new designs, orders cancelled by customers, or specification problems. When the new system was implemented these stock items, together with others, were entered into the system as the beginning balance for theinventorv.Since January 2020, CurtainsMaster has also experienced significant impact due to the COVID-19 pandemic. Approximately 50% of customer orders due to be delivered in May, June and July have been cancelled. Payments from customers have been delayed as they have also been impacted by the situation. Since the middle of February the company's sales at small retail stores have decreased dramatically, by approximately 70%. From the middleof March, 60% of staff (both casual and full-time) were made redundant. For the last three months of the current financial year, the company is expecting to have no sales but still pay another 10% of the current total expenses. To minimise the impact of a tight cashflow, in February, when the financial market was peak, the company sold all its financial investments and generated some extra cash for the business before the market dived in March.However, things can get worse; there is much uncertainty and no clear indication of when the pandemic will end.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Survey Of Accounting

Authors: Thomas Edmonds, Philip Olds, Frances McNair, Bor-Yi Tsay

1st Edition

0073526770, 9780073526775