Answered step by step

Verified Expert Solution

Question

1 Approved Answer

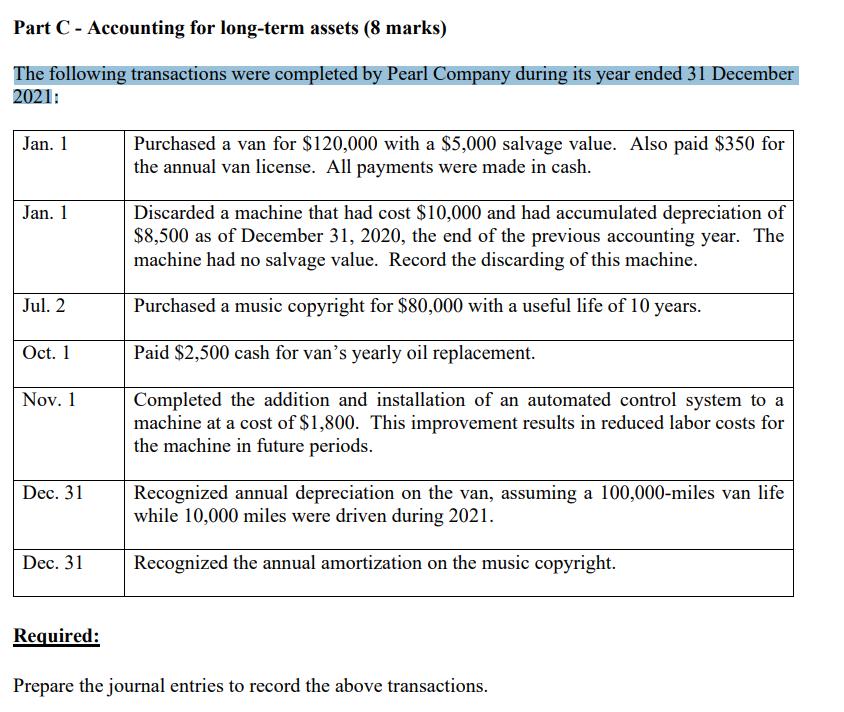

Part C - Accounting for long-term assets (8 marks) The following transactions were completed by Pearl Company during its year ended 31 December 2021:

Part C - Accounting for long-term assets (8 marks) The following transactions were completed by Pearl Company during its year ended 31 December 2021: Jan. 1 Jan. 1 Jul. 2 Oct. 1 Nov. 1 Dec. 31 Dec. 31 Required: Purchased a van for $120,000 with a $5,000 salvage value. Also paid $350 for the annual van license. All payments were made in cash. Discarded a machine that had cost $10,000 and had accumulated depreciation of $8,500 as of December 31, 2020, the end of the previous accounting year. The machine had no salvage value. Record the discarding of this machine. Purchased a music copyright for $80,000 with a useful life of 10 years. Paid $2,500 cash for van's yearly oil replacement. Completed the addition and installation of an automated control system to a machine at a cost of $1,800. This improvement results in reduced labor costs for the machine in future periods. Recognized annual depreciation on the van, assuming a 100,000-miles van life while 10,000 miles were driven during 2021. Recognized the annual amortization on the music copyright. Prepare the journal entries to record the above transactions.

Step by Step Solution

★★★★★

3.46 Rating (156 Votes )

There are 3 Steps involved in it

Step: 1

SOLU...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Accounting

Authors: Jonathan E. Duchac, James M. Reeve, Carl S. Warren

23rd Edition

978-0324662962