Answered step by step

Verified Expert Solution

Question

1 Approved Answer

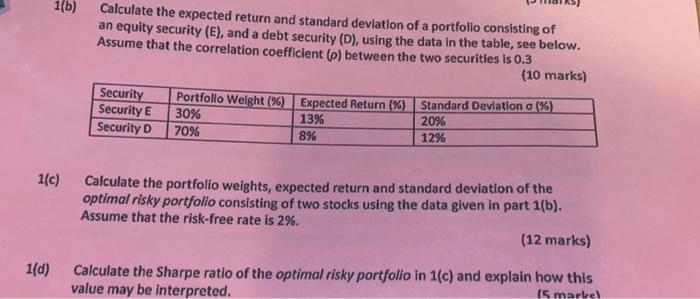

part C and D only 1(b) Calculate the expected return and standard deviation of a portfolio consisting of an equity security (E), and a debt

part C and D only

1(b) Calculate the expected return and standard deviation of a portfolio consisting of an equity security (E), and a debt security (D), using the data in the table, see below. Assume that the correlation coefficient (e) between the two securities is 0.3 (10 marks) Security Security E Security D Portfolio Weight %) Expected Return (%) 30% 13% 70% 8% Standard Deviation (%) 20% 1296 1(c) Calculate the portfolio weights, expected return and standard deviation of the optimal risky portfolio consisting of two stocks using the data given in part 1(b). Assume that the risk-free rate is 2%. (12 marks) 1(d) Calculate the Sharpe ratio of the optimal risky portfolio in 1(c) and explain how this value may be interpreted. (5 marvel Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals Of Futures And Options Markets

Authors: John C. Hull

8th Global Edition

1292155035, 9781292155036