Answered step by step

Verified Expert Solution

Question

1 Approved Answer

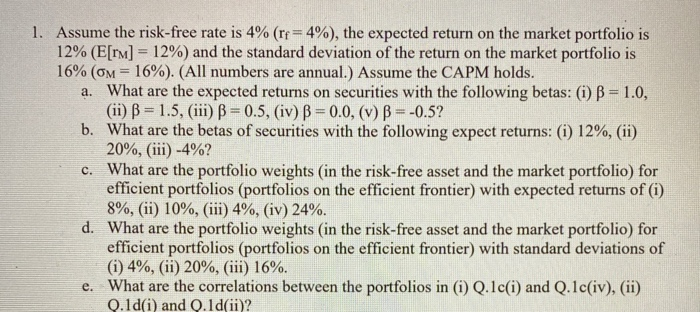

PART E ONLY PLZ 1. Assume the risk-free rate is 4% (re= 4%), the expected return on the market portfolio is 12% (E[mm] = 12%)

PART E ONLY PLZ

1. Assume the risk-free rate is 4% (re= 4%), the expected return on the market portfolio is 12% (E[mm] = 12%) and the standard deviation of the return on the market portfolio is 16% (om = 16%). (All numbers are annual.) Assume the CAPM holds. a. What are the expected returns on securities with the following betas: (1) B = 1.0, (ii) B = 1.5, (iii) = 0.5, (iv) B = 0.0, (v) = -0.5? b. What are the betas of securities with the following expect returns: (i) 12%, (ii) 20%, (iii) -4%? c. What are the portfolio weights (in the risk-free asset and the market portfolio) for efficient portfolios (portfolios on the efficient frontier) with expected returns of (i) 8%, (ii) 10%, (iii) 4%, (iv) 24%. d. What are the portfolio weights (in the risk-free asset and the market portfolio) for efficient portfolios (portfolios on the efficient frontier) with standard deviations of (i) 4%, (ii) 20%, (iii) 16%. e. What are the correlations between the portfolios in (i) Q.1c(i) and Q.1c(iv), (ii) Q.10(i) and Q.1d(ii) Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Strategies For Forex Trading How To Maximizing Your Potential Returns

Authors: Clifton Bemrich

1st Edition

979-8388676955