Answered step by step

Verified Expert Solution

Question

1 Approved Answer

part (i) and (iii) QUESTION 3 Q3(a) Use the data for two perfectly-negatively correlated risky securities, Securit.Pand Security B, shown in the table below to,

part (i) and (iii)

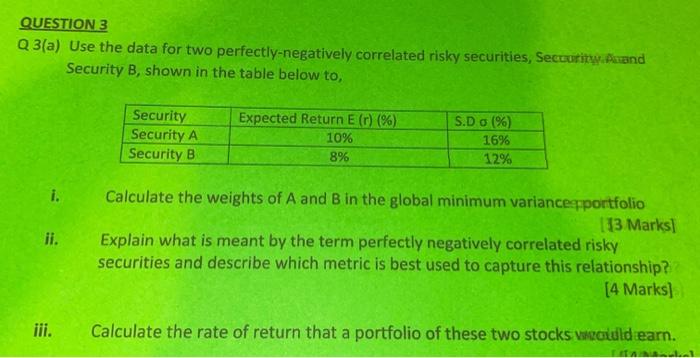

QUESTION 3 Q3(a) Use the data for two perfectly-negatively correlated risky securities, Securit.Pand Security B, shown in the table below to, Security Security A Security B Expected Return E (r) (%) 10% S.D. (%) 16% 12% 8% i. ii. Calculate the weights of A and B in the global minimum variance portfolio 113 Marks Explain what is meant by the term perfectly negatively correlated risky securities and describe which metric is best used to capture this relationship? [4 Marks] iii. Calculate the rate of return that a portfolio of these two stocks would earn Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Global Corporate Finance A Focused Approach

Authors: Suk Hi Kim, Kenneth A Kim

2nd Edition

9814618004, 9789814618007