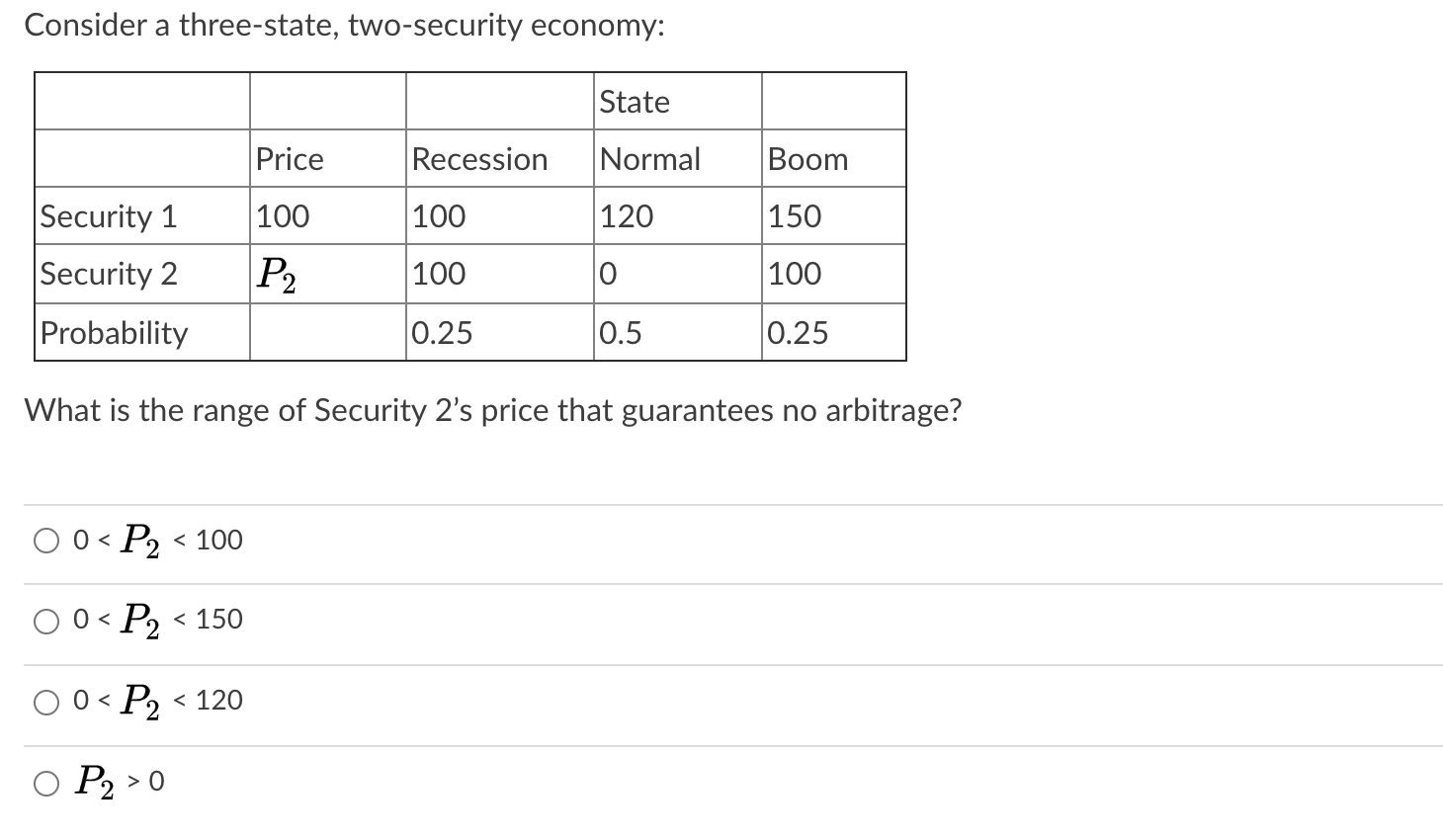

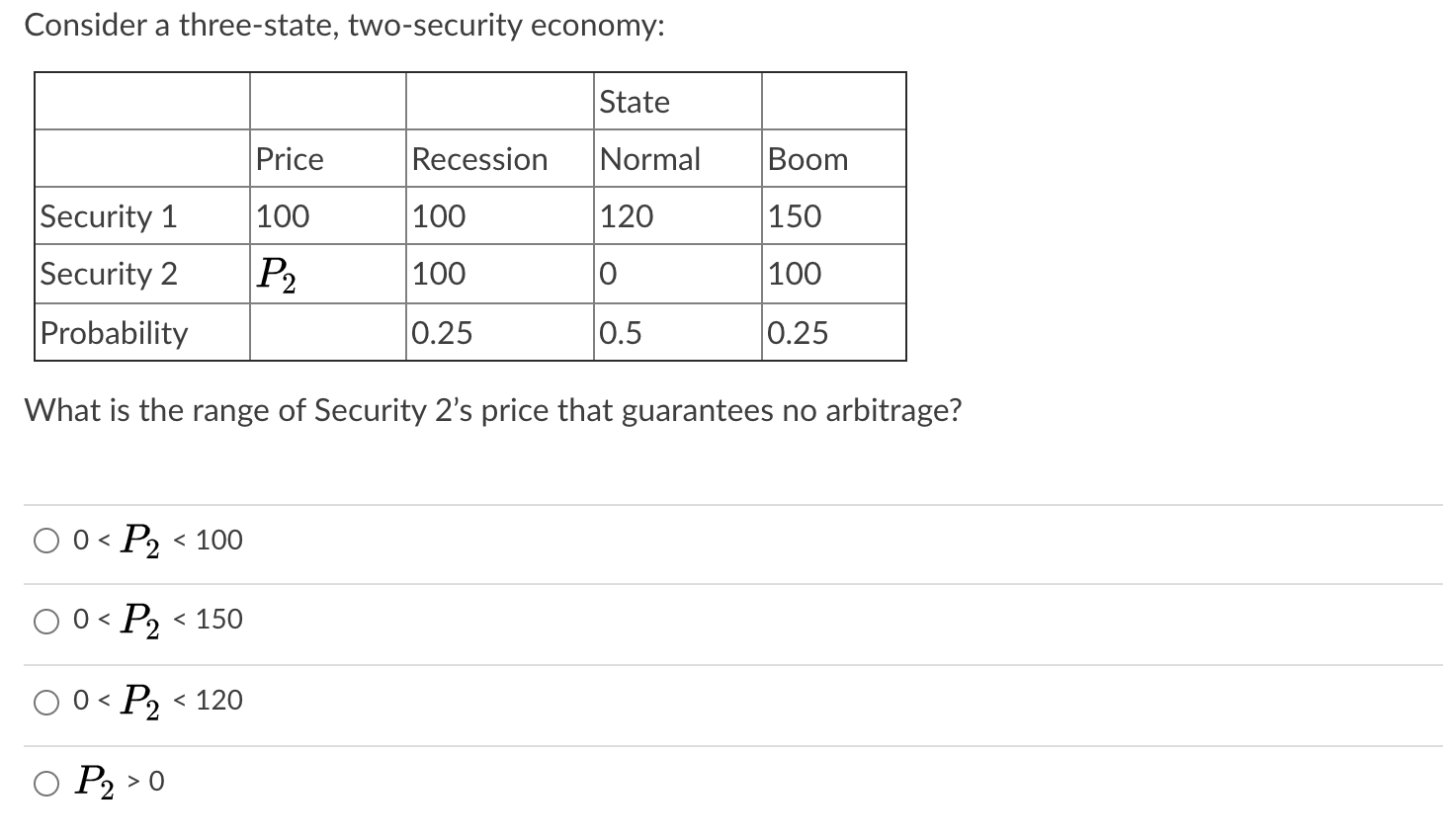

Question

Part II: Multiple Choice Each question is worth 4pt. Some questions may have more than one correct answer. 1.There is a risky gamble that will

Part II: Multiple Choice

Each question is worth 4pt.Some questions may have more than one correct answer.

1.There is a risky gamble that will pay either $80 or $120, each with equal probability. Consider an investor with utility function u(w) = ln(w) and no initial wealth. What is the investor's certainty equivalent for this gamble?

84.85

100

95.42

None of the above

97.98

2.Suppose you have $1000 invested in a stock portfolio in August. You have $200 invested in Stock A, $300 in Stock B and $500 in Stock C. The monthly return of August for Stock A was 2%, for Stock B was 4% and for Stock C was -5%. What is the monthly return for this portfolio in August?

Group of answer choices

-0.5%

-0.9%

1.3%

-1.2%

3.You currently have 40% of your money invested in a risky portfolio of stocks and the remaining 60% in the risk-free bonds. Suppose you adjust your portfolio to 70% in the same portfolio of risky stocks and 30% in the risk-free bonds. What will happen to the Sharpe ratio of your portfolio?

Group of answer choices

Sharpe ratio remains the same

We cannot determine what happens to the Sharpe ratio from this information

Sharpe ratio will increase

Sharpe ratio will decrease

4.

Consider an investor with mean-variance preferences whose total wealth consists of both riskless human capital (H) and financial wealth (W). Which of the following statements are true?

Group of answer choices

If volatility of the MVE portfolio increases, the investor should shift some of her financial wealth toward riskless bonds.

If H unexpectedly increases (but is still expected to be riskless going forward), the investor should reallocate some of her financial wealth to risky assets.

If W unexpectedly decreases, the investor should reallocate some of her financial wealth toward riskless bonds.

As the investor gets older (and H falls), she should allocate more of her financial wealth to riskless bonds.

5.Which of the following assumptions is not necessary for the CAPM to hold?

Group of answer choices

All investors have the same belief over the distribution of asset returns.

All investors are mean variance optimizers.

All investors have the same degree of risk aversion.

All assets are traded.

6.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

International Business The Challenges Of Globalization

Authors: John J. Wild, Kenneth L. Wild

9th Edition

0134729226, 978-0134729220