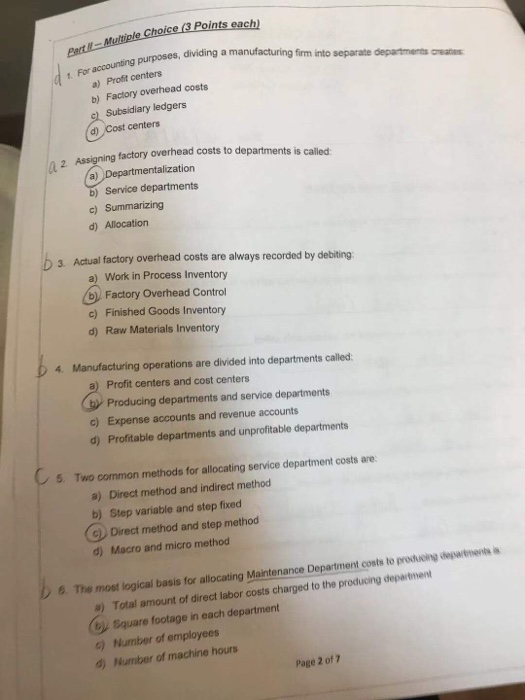

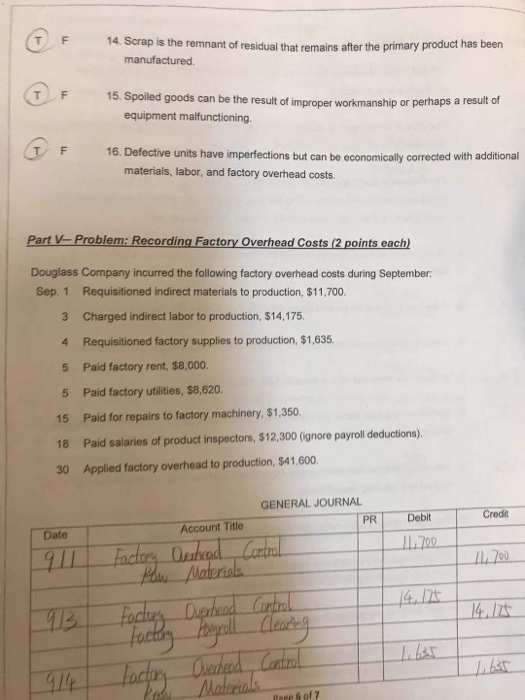

Part -Multiple Choice (3 Points each) 1. For accounting purposes, dividing a manufacturing firm into separate departments creates a) Profit centers b) Factory overhead costs e) Subsidiary ledgers d) Cost centers a 2 Assigning factory overhead costs to departments is calied: a) Departmentalization b) Service departments c) Summarizing d) Allocation 3. Actual factory overhead costs are always recorded by debiting: a) Work in Process Inventory bFactory Overhead Control Finished Goods Inventory d) Raw Materials Inventory 4 Manufacturing operations are divided into departments called: a) Profit centers and cost centers b Producing departments and service departments c) Expense accounts and revenue accounts d) Profitable departments and unprofitable departments Two common methods for allocating service department costs are 5 a) Direct method and indirect method b) Step variable and step fixed c Direct method and step method d) Macro and micro method 6. The most logical basis for allocating Maintenance Department costs to producing depatnents s a) Total amount of direct labor costs charged to the producing department by Square footage in each department Number of employees d Number of machine hours Page 2 of 7 F 14. Scrap is the remnant of residual that remains after the primary product has been manufactured 15. Spoiled goods can be the result of improper workmanship or perhaps a result of equipment malfunctioning T F 16. Defective units have imperfections but can be economically corrected with additional materials, labor, and factory overhead costs. Part V- Problem: Recording Factory Overhead Costs (2 points each) Douglass Company incurred the following factory overhead costs during September Sep. 1 Requisitioned indirect materials to production, $11,700 Charged indirect labor to production, $14,175. 3 Requisitioned factory supplies to production, $1,635 4 5 Paid factory rent, $8,000. Paid factory utilities, $8,620. 5 Paid for repairs to factory machinery, $1,350. 15 Paid salaries of product inspectors, $12,300 (ignore payroll deductions). 18 Applied factory overhead to production, $41,600. 30 GENERAL JOURNAL Debit Credit PR Account Title Date Fadury Orshead Cartral Phst platerials 700 911 700 Fochr Dighead Carrol Fuddla Pragall Cla'e'g Crerheod Centrol 14. 175 414 Focers Oadiad Malerials 9l4 Page 6 of 7 Part -Multiple Choice (3 Points each) 1. For accounting purposes, dividing a manufacturing firm into separate departments creates a) Profit centers b) Factory overhead costs e) Subsidiary ledgers d) Cost centers a 2 Assigning factory overhead costs to departments is calied: a) Departmentalization b) Service departments c) Summarizing d) Allocation 3. Actual factory overhead costs are always recorded by debiting: a) Work in Process Inventory bFactory Overhead Control Finished Goods Inventory d) Raw Materials Inventory 4 Manufacturing operations are divided into departments called: a) Profit centers and cost centers b Producing departments and service departments c) Expense accounts and revenue accounts d) Profitable departments and unprofitable departments Two common methods for allocating service department costs are 5 a) Direct method and indirect method b) Step variable and step fixed c Direct method and step method d) Macro and micro method 6. The most logical basis for allocating Maintenance Department costs to producing depatnents s a) Total amount of direct labor costs charged to the producing department by Square footage in each department Number of employees d Number of machine hours Page 2 of 7 F 14. Scrap is the remnant of residual that remains after the primary product has been manufactured 15. Spoiled goods can be the result of improper workmanship or perhaps a result of equipment malfunctioning T F 16. Defective units have imperfections but can be economically corrected with additional materials, labor, and factory overhead costs. Part V- Problem: Recording Factory Overhead Costs (2 points each) Douglass Company incurred the following factory overhead costs during September Sep. 1 Requisitioned indirect materials to production, $11,700 Charged indirect labor to production, $14,175. 3 Requisitioned factory supplies to production, $1,635 4 5 Paid factory rent, $8,000. Paid factory utilities, $8,620. 5 Paid for repairs to factory machinery, $1,350. 15 Paid salaries of product inspectors, $12,300 (ignore payroll deductions). 18 Applied factory overhead to production, $41,600. 30 GENERAL JOURNAL Debit Credit PR Account Title Date Fadury Orshead Cartral Phst platerials 700 911 700 Fochr Dighead Carrol Fuddla Pragall Cla'e'g Crerheod Centrol 14. 175 414 Focers Oadiad Malerials 9l4 Page 6 of 7