perusall reading comment on the article

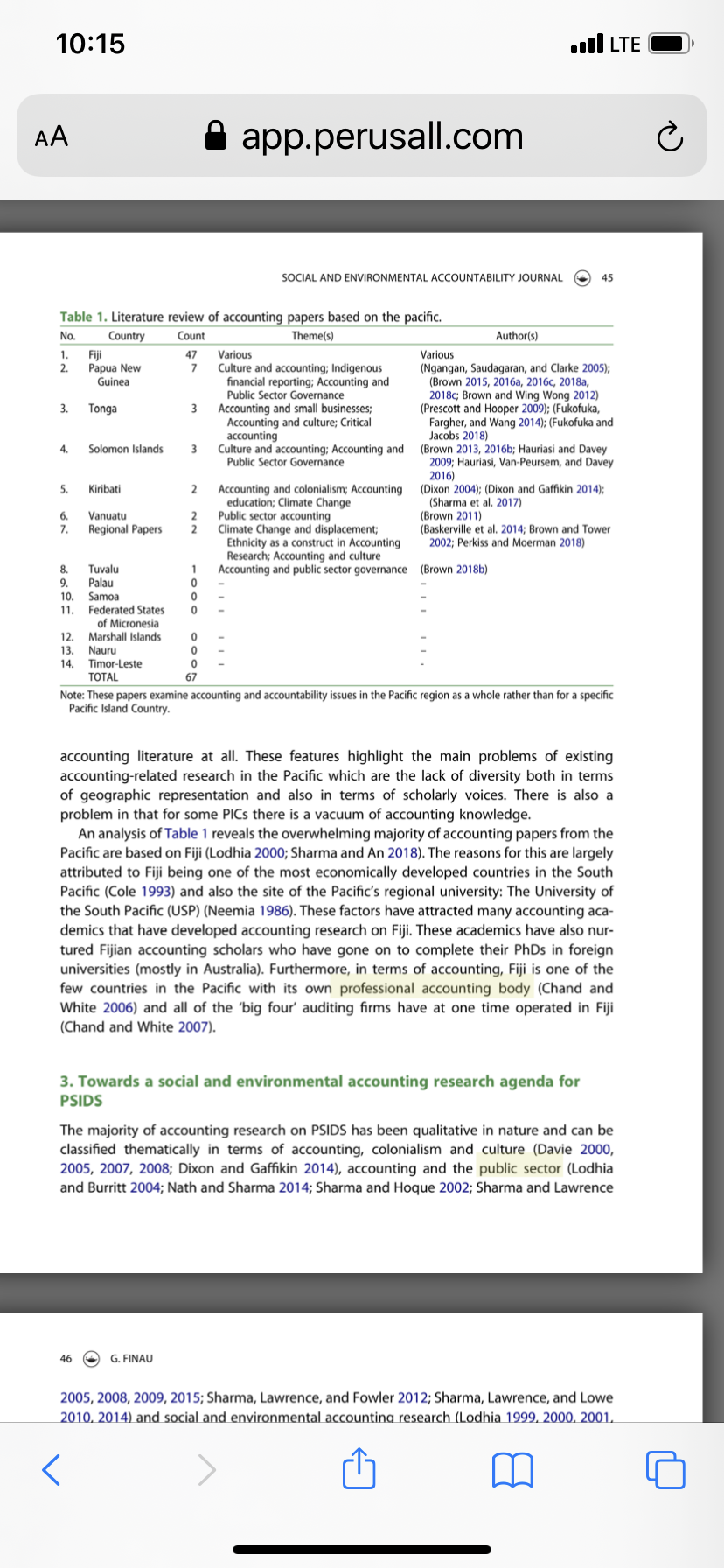

10:15 DOI LTE AA app.perusall.com C SOCIAL AND ENVIRONMENTAL ACCOUNTABILITY JOURNAL 45 Table 1. Literature review of accounting papers based on the pacific. No. Country Count Theme(s Author(s) 1. Fiji Various Various 2. Papua New Culture and accounting; Indigenous (Ngangan, Saudagaran, and Clarke 2005); Guinea financial reporting; Accounting and (Brown 2015, 2016a, 2016c, 2018a, Public Sector Governance 2018c; Brown and Wing Wong 2012) 3. Tonga 3 Accounting and small businesses; (Prescott and Hooper 2009); (Fukofuka, Accounting and culture; Critical Fargher, and Wang 2014); (Fukofuka and accounting Jacobs 2018) Solomon Islands Culture and accounting; Accounting and (Brown 2013, 2016b; Hauriasi and Davey Public Sector Governance 2009; Hauriasi, Van-Peursem, and Davey 2016) 5. Kiribati 2 Accounting and colonialism; Accounting (Dixon 2004); (Dixon and Gaffikin 2014); education; Climate Change (Sharma et al. 2017) 6. Vanuatu (Brown 2011) NN Public sector accounting 7 Regional Papers Climate Change and displacement; (Baskerville et al. 2014; Brown and Tower Ethnicity as a construct in Accounting 2002; Perkiss and Moerman 2018) Research; Accounting and culture 8. Tuvalu Accounting and public sector governance (Brown 2018b) 9. Palau 10. Samoa 11. Federated States of Micronesia 12. Marshall Islands 13. Nauru GOOD 14. Timor-Leste TOTAL Note: These papers examine accounting and accountability issues in the Pacific region as a whole rather than for a specific Pacific Island Country. accounting literature at all. These features highlight the main problems of existing accounting-related research in the Pacific which are the lack of diversity both in terms of geographic representation and also in terms of scholarly voices. There is also a problem in that for some PICs there is a vacuum of accounting knowledge. An analysis of Table 1 reveals the overwhelming majority of accounting papers from the Pacific are based on Fiji (Lodhia 2000; Sharma and An 2018). The reasons for this are largely attributed to Fiji being one of the most economically developed countries in the South Pacific (Cole 1993) and also the site of the Pacific's regional university: The University of the South Pacific (USP) (Neemia 1986). These factors have attracted many accounting aca- demics that have developed accounting research on Fiji. These academics have also nur- tured Fijian accounting scholars who have gone on to complete their PhDs in foreign universities (mostly in Australia). Furthermore, in terms of accounting, Fiji is one of the few countries in the Pacific with its own professional accounting body (Chand and White 2006) and all of the 'big four' auditing firms have at one time operated in Fiji (Chand and White 2007). 3. Towards a social and environmental accounting research agenda for PSIDS The majority of accounting research on PSIDS has been qualitative in nature and can be classified thematically in terms of accounting, colonialism and culture (Davie 2000, 2005, 2007, 2008; Dixon and Gaffikin 2014), accounting and the public sector (Lodhia and Burritt 2004; Nath and Sharma 2014; Sharma and Hoque 2002; Sharma and Lawrence G. FINAU 2005, 2008, 2009, 2015; Sharma, Lawrence, and Fowler 2012; Sharma, Lawrence, and Lowe 2010, 2014) and social and environmental accounting research (Lodhia 1999, 2000, 2001. A10:15 DOI LTE AA app.perusall.com C 44 G. FINAU Given the urgency of social and environmental issues impacting the region, all disciplines including accounting must respond by re-imagining research from its underlying philos- ophies to how it is practised. The following section presents the literature review of accounting research on PSIDS and the final section provides some future directions based on this review. 2. A literature review of accounting research based on Pacific small Island developing states The dearth of accounting literature based on the Pacific has meant that there is a lack of any literature review of accounting papers based on PSIDS. There have been literature reviews conducted on broader regions in which the Pacific is a part of, such as the Asia Pacific region (Benson et al. 2015) and Australasia (de Villiers and Hsiao 2018), however, the literature on these regions are dominated by countries in the larger, more developed economies such as Australia and New Zealand. The issues and challenges of these countries are very different from those facing the Pacific. The PSIDS in contrast to Australia and New Zealand are under-developed and small in terms of population and land mass. And arguably some of the actions by the larger metropolitan economies of the Pacific are leading to the problems that PSIDS are facing (Connell 2003). Sharma and An (2018) conduct a literature review of accounting and accountability research based solely on Fiji. Focusing on papers published in accounting refereed jour- nals, the review synthesises 47 papers published since 1978. Their review finds that most papers focused on financial reporting and accountability (46.8%), followed by new public management (29.8%) and sustainability accounting was third (12.7%). Sharma and An (2018) limit their survey to selected journals which can be categorised as the most prominent journals in the field of accounting research and journals that publish on topics within the Asia-Pacific region. I have conducted a similar review of accounting and accountability research for the 13 independent countries that are listed as PSIDS. I have also included papers that examine accounting and accountability issues even if these papers were not published in specific accounting journals. To search for papers related to the context of the study, I used the search terms such as the name of the country and the terms 'accounting', 'auditing', 'accountability' and 'financial reporting'. For papers that were returned and matched the criteria of my review, I further conducted a citation analysis. Google scholar shows the number of times a paper has been cited by other authors. I analysed these citations to identify any papers that also matched the criteria of my literature review. Table 1 below summarises the results of this review. My review found 67 papers published on accounting-related issues on PSIDS. From Table 1, the following features of extant accounting-related research on the PSIDS can be ascertained. Firstly, research is dominated by one country - Fiji - with approximately 70% of papers published on the country. Secondly, there was also a dominance of certain authors. This is understandable as scholars invariably specialise on a particular geo- graphical context. Authors such as Sumit Lodhia and Umesh Sharma were the most prolific writers of SEA research in the Pacific. Alistair Brown wrote extensively on the tensions between traditional reporting models and Western reporting models using a number of PSIDS as his context of study. Lastly, almost half of the total PSIDS surveyed have no SOCIAL AND ENVIRONMENTAL ACCOUNTABILITY JOURNAL 45 Table 1. Literature review of accounting papers based on the pacific. No. Country Coun Theme(s) Author(s) 1. Fiji 47 Various Various 2. Papua New Culture and accounting; Indigenous (Ngangan, Saudagaran, and Clarke 2005); A10:15 IIII LTE Ci AA 3 app.perusa||.com C as (.9 ormau traditional knowledge from Indigenous peoples can provide key insights into dealing with the threat of climate change. Thus accounting research needs to draw from this rich, con- textualised Indigenous knowledge in developing solutions that are not only relevant to the Pacic but may also be relevant to countries around the world. Indigenous peoples must not be treated as mere objects of research but as co-creators of the knowledge through the research process. Thus imagining a future of SEA research in the Pacic must involve engaging with Indigenous peoples by respecting their agency and as noted by Buhr (2012i exploring how this agency can be enabled. 4. Conclusion Imagining a research agenda for climate change Involves developing a solution that can address the problem. The nature of the solution must be able to address the specic characteristics of the problem. The problem In this case Is climate change. The cause of the problem is human greed. human selshness and an ignorance of the destruction of the environment and the suffering that is inicted on other communities that are not directly part oi the country causing the pollution. To counter this problem. the solution must be based on the potential for good within humans - that Is the solution must be based on a communal spirit and a deep respect for the environment. Furthermore, the nature of the problem Is not Isolated to one country but affects the entire Pacic region. Thus, luture research must examine the impacts of climate change and the poten- tial for accounting across the region as different countries will have different sets of chal- lenges and potential solutions. PSIDS are at the forefront of our modern global ecological crisis with global warming induced sea-level rise threatening low lying islands, climate change increasing the preva- lence and volatility of natural disasters and large-scale unsustainable resource extraction practices by foreign corporations. The accounting literature related to PSIDS has been largely based on Fijian experiences. This is due to Fiji considered by many as the hub of the South Pacic and the site of the main campus for the University of the South Pacic (USP) a regional university that is 'owned' by 12 countries of the Paclc.This has attracted many accounting scholars who have researched on accounting issues in Fiji and have also trained a generation of Fijian accounting academics. The result has been the overwhelm- ing majority of research on the South Pacic based on Fiji. While this has signicantly improved our understanding of accounting issues related to Fiji, more is required urgently, in Fiji and especially In other PSIDS. While Fiji is often seen as a model for other PSIDS, the Pacic is diverse and while countries in this region share common issues, there are also Issues which are unique to Individual countries' history, culture and context. Whlle climate change It indeed a pressing problem and seems to present insurmoun- table challenges. It is a problem that needs to be addressed for the future of the Pacic and the future of the world. Climate change is a complex and multidimensional phenomenon. Understanding the role of accounting in climate change requires academics to embrace diversity in terms of disciplinary knowledge. knowledge production processes and voices. This means working with people from different disciplines. working In a network that is focussed on the SEA issues related to PSIDS. and amplifying voices of previously silenced groups of people such as Indigenous peoples of the Pacic, SOCIAL AND ENVIRONMENTAL ACCOUNTABILITY JOURNAL E.) 49 N cites 1. Sovereign countries refer to independent countries that have the supreme power to formulate and uphold their laws. 10:15 .III LTE Ci AA 9 app.perusa||.com C'; 45 Q 6. FINAL! 2005, 2008, 2009, 2015; Shanna, lawrence. and Fowler 2012; Sharma, Lawrence. and Lowe 2010. 2014i and social and environmental accounting research (Lodhla 1999. 2000. 2001. 2003. 2004; Brita 2009; Shanna and Davey 2013: Sharma. Low, and Davey 2013). These three themes have emerged based on the Pacic's history, culture, economy and current state of environmental precarity. Of the three themes. I argue that the social and environmental accounting theme is the most Important because of the risks and threats of the climate crisis to PSIDS. And given the urgency of the Issue. more worlr needs to be done to help PSIDS deal with this threat. However, it is not just about Increas- lng the quantity of work but also trying to ensure that research ls relevant to the context of the Pacic and that solutions are tailored for each Pacic Island State. The next section out- lines possible Interventions that could reinvigorate SEA research on the Pacic especially in the face of the current climate emergency. 3.1. Towards inter-disciplinary, collaborative and indigenous inspired SEA research Climate change is a 'wiclred problem' and these types of problems are complex but are the most important problems that need to be addressed because of their persistent and per- vasive nature (Jacobs and Cuganesan 2014). The complex nature of 'wlcked problems' requires a shift In the modes of knowledge production from a parochial point-oi-view to a broader and holistic perspective. I thus make three Inter-related suggestions for how a new research agenda can be forged. These suggestions focus on the process by which these new forms of knowledge are created. The rst involves knowledge creation that draws from other disciplines to inform the practice of SEA accounting. The second relates to altering the structure of knowledge groups and networks to foster a diversity of ideas, experiences and perspectives. And lastly, future SEA must engage with Indigen- ous peoples. Indigenous knowledge and Indigenous worldviews in a more meaningful manner. The rst suggestion relates to adopting a more inter-disciplinary approach. This involves accounting researchers going beyond accounting scholarship and engaging with research from other disciplines. These disciplines include those In the physical sciences such as environmental science, sustainability science and those In the social sciences such as sociology and anthropology. The social sciences in particular could be the most relevant for accounting researchers to engage with in trying to address climate change-related Issuer. While most literature user the analogy of combatting climate change, It Is not nature that we are ghting against but rather humans. For It Is the actions of humans that is causing the increasing volatility and effects of climate change. Specically. these are powerful corporations and countries that exploit the environment for economic gain and Ignore the extemalitles that affect other countries. Accounting can help PSIDS by providing a means by which Individuals, organisations and states can provide accounts of the impacts of climate change In the Paclc. These accounts do not necessarily have to be presented In quantitative terms but can also Include narratives and stories. These accounts and narratives can be incorporated In annual reports of entities and provide a means for both account-giving by those within the entities and also an opportunity for users of the reports to understand the accounts of those within the organisation. These accounts are important in telling the world SOCIAL AND ENVIRONMENTAL ACCOUNTABILITY JOURNAL Ct) 41 Pacic Island stories and are useful as evidence In lobbying at International Conferences 10:14 OOO LTE AA app.perusall.com C SOCIAL AND ENVIRONMENTAL ACCOUNTABILITY JOURNAL 2020, VOL. 40, NO. 1, 42-52 Routledge https://doi.org/10.1080/0969160X 2020.1719171 Taylor & Francis Group Check for updates Imagining the Future of Social and Environmental Accounting Research for Pacific Small Island Developing States Glenn Finau The University of New South Wales, Canberra, Australia ABSTRACT In this paper, I contribute to the conversation of imagining the future of Social and Environmental Accounting (SEA) research for Pacific Small Island Developing States (PSIDS). I focus on PSIDS as this region is arguably the most disadvantaged region given its low economic base, geographic isolation and environmental precarity. Initially, I conduct a literature review of accounting- related papers based on PSIDS and provide some suggestions for a research agenda of SEA for PSIDS. The literature review highlights that SEA research in the Pacific is an under-researched area and the few studies on SEA in the Pacific have largely been based on Fiji. For many countries in the Pacific, there is a vacuum of academic literature, however, there is a need to better understand the role of SEA in assisting these island nations address pertinent social and environmental issues, and no issue is as important as climate change. I make some inter-related suggestions for the future of SEA research for PSIDS. These suggestions emphasise the production of knowledge that draws on a diversity of perspectives from other disciplines and focuses on developing solutions based on the context of PSIDS and the lived realities of Pacific Island peoples. 1. Introduction Social and Environmental Accounting (SEA) research is a relatively young but an important field given the global environmental and ecological crisis of climate change and its related effects (Bebbington and Larrinaga-Gonzalez 2008). Nowhere else are the effects of climate change as visible and acute than in the Pacific region and especially by the region's low- lying island states (Pelling and Uitto 2001). While there is a burgeoning body of literature examining the impacts of climate change in the Pacific (Barnett 2005), there is a dearth of literature from the accounting discipline. This is unfortunate as accounting research has an important contribution to the academic discourse on climate change and the sustainabil ity agenda in general (Bebbington, Russell, and Thomson 2017). Accounting is more than a system of inscribing values on assets and liabilities or keeping track of how money is spent. Accounting is an information system and thus produces valuable information that is crucial for resource owners and management in their decision-making processes. The design of such accounting systems also entails the design of appropriate accountability CONTACT Glenn Finaug.finau@student.adfa.edu.au 2020 Centre for Social and Environmental Accounting Research SOCIAL AND ENVIRONMENTAL ACCOUNTABILITY JOURNAL - 4310:15 DO LTE AA app.perusall.com C SOCIAL AND ENVIRONMENTAL ACCOUNTABILITY JOURNAL 43 structures. Therefore accounting as an information system and a system of organising shapes business practices and thus accountants are influential actors that can also be posi- tive agents of change within organisations and society as a whole (Lovell and Mackenzie 2011). In terms of SEA issues, the existential threat of the global climate crisis is the most pressing and urgent issue affecting PSIDS (Barnett 2001). However, there is a paucity of accounting research that examines these issues within PSIDS (Sharma et al. 2017; Sharma and Samkin 2018). Small Island Developing States (SIDS) is an analytical category created by the United Nations (UN) during the 1992 Earth Summit held in Brazil (United Nations 2014). The UN identified that within developing countries, certain shared characteristics created common disadvantages (United Nations 2014). SIDS are defined as small island states that are characterised by smallness, insularity, remoteness, geographic dispersion, narrow economic base and vulnerability to natural disasters (Briguglio 1995). The UN cat- egorises SIDS within the regions of the Caribbean, the Atlantic, Indian Ocean, Mediterra- nean and South China Sea (AIMS) and the Pacific (United Nations 2018). In this paper, I focus on the Pacific region, a region that is located in the Pacific Ocean and comprises of 13 sovereign' countries that are members of the UN (Manoa 2015). The SIDS of the Pacific region are known as PSIDS or Pacific Small Island Developing States. With the exception of Papua New Guinea (PNG), the PSIDS are small island masses with large bodies of water under their control. Some of the smallest countries in the world are from the Pacific region (Easterly and Kraay 2000). The UN's categorisation of countries into specific regions is a way to group countries based on shared problems of geography, circumstances and development status. Manoa (2015) states that the classification of countries into regional groups emerged from the need to raise funds for specific priority areas within the different regional groups. Such a system facilitates the allocation of resources and the development of plans to assist these regions in achieving the UN's Sustainability Development Goals (SDGs). There has also been an increasing call by accounting academics to examine the role of accounting in this endeavour and the way the UN's SDGs can inform the practices of accounting (Bebbington, Russell, and Thomson 2017; Bebbington and Unerman 2018). PSIDS are at the forefront of our modern global ecological crisis with global warming induced sea-level rise threatening low lying islands, climate change increasing the preva- lence and volatility of natural disasters and large-scale unsustainable resource extraction practices by foreign companies (Pelling and Uitto 2001). These are urgent problems facing the PSIDS and governments of these countries and the International Community are grappling with how best to address these pertinent issues that is not only leading to the degradation, erosion and loss of land but also the displacement of thousands of Pacific Island peoples (Perkiss and Moerman 2018). Research is needed from all fields to better understand how to address the complex social and environmental problems facing PSIDS. This paper conducts a review of the literature of accounting papers on PSIDS to identify what has been done and what can be done within the discipline for accounting to be relevant to addressing these issues. The literature review reveals a scarcity of literature on SEA research on the Pacific and the literature that does exist is largely based on one country: Fiji. This has led to Fiji being the centre of Pacific accounting research. Furthermore, SEA research on PSIDS has been in a period of hiatus. Most SEA research on the Pacific was written more than ten years ago. 44 G. FINAU Given the urgency of social and environmental issues impacting the region, all disciplines including accounting must respond by re-imagining research from its underlying philos- ophies to how it is practised. The following section presents the literature review of accounting research on PSIDS and the final section provides some future directions based on this review. A m10:15 IIII LTE Ci AA 9 app.perusa||.com G SOCIAL AND ENVIRONMENTAL ACCOUNTAIILITV JOURNAL 41 Pacic Island stories and are useful as evidence In lobbying at International Conferences on Climate Change. Universities have also created programmes such as climate nance that seek to merge the elds of climate science with business related disciplines. However. the climate nance programmes that are offered focus more on the climate science dimension as opposed to the accounting-related implications of climate change. One of the challenges within this region for undertaking such inter-disciplinary research on Pacic-wide issues Is the lack of resources to conduct such research. The small size of PSIDS, the lack of research funds and human resource capacity has contributed to the rela- tively low output of accounting research that seeks to address climate change. Even the largest of the universities in the Pacic - USP - faces challenges of attracting and retaining academics and producing research given the high workloads of academic staff. These chal- lenges are even more acute in national universities of PSIDS. While accounting is relevant In addressing climate change, the complexity of climate change as a global environmental issue and the embryonic nature of accounting research in climate change mean that the SEA research for PSIDS would be best con- ducted collaboratively between researchers from different PSIDS. These projects would also benefit from academics in the larger developed economies such as the neighbour- ing metropolitan countries of Australia and New Zeaianci who possess requisite skills. knowledge and experience and also access to research funds. The importance of colla- borative work within the region can be facilitated by existing research networks such as The Australasian Center for Social and Environmental Accounting Research lACSEARI. The ACSEAR network has been instrumental in promoting SEA research within the Asia Pacic region. In 2018. the A-CSEAR conference was held in Fiji, the rst time an ACSEAR conference has been held outside of Australia and New Zealand. This high- lights A-CSEAR's increasing engagement with PSIDS. I believe that A-CSEAR is a relevant network that can be leveraged by PSIDS for building research networks to engage in collaborative projects that can address climate change Issues relating to PSIDS. A poss- ible alternative to creating a network within A-CSEAR is for a completely new research network to be established. A new research network that is based on a structure that is not tied to historic colonial power relations and western forms of knowledge but rather based on Indigenous world views and indigenous ways of knowing that can inform research practices. This new network could provide a space for the development of Indigenous research agendas. Furthermore, another example of a regional Inter-disci- plinary network is the University of the Arctic. The University of the Arctic is a collabora- tive network of tertiary institutions. research institutions and other organisations concerned with research and education about the circumpolar' North region (UArctlc 2019). Insights. experiences and lessons can also be drawn from this network in the for- mation of the PSIDS network on SEA. Lastly. future SEA research must seek to empower and amplify the voices of indigenous peoples of PSIDS. Most researchers have studied Indigenous people from a distance and depict them as disenfranchised objects lacking agency [Buhr 2012). This discourse [)2pr tuates the image of Indigenous peoples as impoverished and victims without power. However. Indigenous peoples of the Pacic have learned to adapt to their harsh environ ments. hundreds of years before the arrival of colonial settlers. Indigenous peoples have developed complex systems of adaptation and have lived sustainably with their environ- ment for centuries (Mercer et al. 2007). While the climate crisis poses new challenges. 45 @ orrrrau traditional knowledge from Indigenous peoples can provide key insights Into dealing with the threat of climate change. Thus accounting research needs to draw from this rich. con- textualised Indigenous knowledge in developing solutions that are not only relevant to the Pacic but may also be relevant to countries around the world. Indigenous peoples must not be treated as mere objects of research but as co-creators of the knowledge through