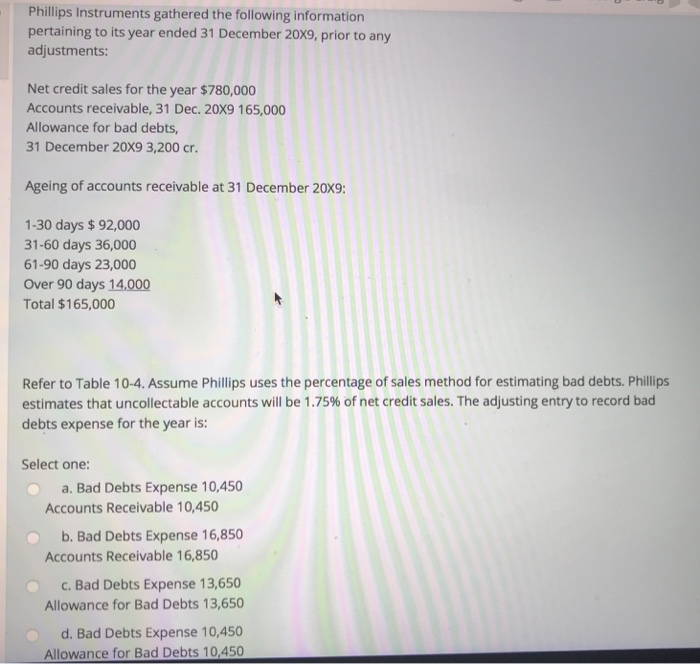

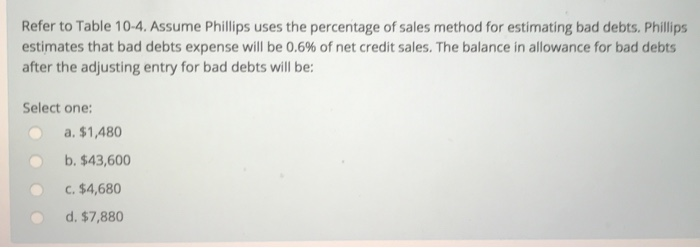

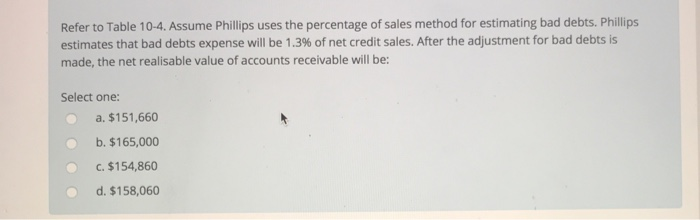

Phillips Instruments gathered the following information pertaining to its year ended 31 December 20X9, prior to any adjustments: Net credit sales for the year $780,000 Accounts receivable, 31 Dec. 20X9 165,000 Allowance for bad debts, 31 December 20X9 3,200 cr. Ageing of accounts receivable at 31 December 20x9: 1-30 days $ 92,000 31-60 days 36,000 61-90 days 23,000 Over 90 days 14,000 Total $165,000 Refer to Table 10-4. Assume Phillips uses the percentage of sales method for estimating bad debts. Phillips estimates that uncollectable accounts will be 1.75% of net credit sales. The adjusting entry to record bad debts expense for the year is: Select one: a. Bad Debts Expense 10,450 Accounts Receivable 10,450 b. Bad Debts Expense 16,850 Accounts Receivable 16,850 c. Bad Debts Expense 13,650 Allowance for Bad Debts 13,650 d. Bad Debts Expense 10,450 Allowance for Bad Debts 10.450 Refer to Table 10-4. Assume Phillips uses the percentage of sales method for estimating bad debts. Phillips estimates that bad debts expense will be 0.6% of net credit sales. The balance in allowance for bad debts after the adjusting entry for bad debts will be: Select one: a. $1,480 b. $43,600 .$4,680 d. $7,880 Refer to Table 10-4. Assume Phillips uses the percentage of sales method for estimating bad debts. Phillips estimates that bad debts expense will be 1.3% of net credit sales. After the adjustment for bad debts is made, the net realisable value of accounts receivable will be: Select one: a. $151,660 b. $165,000 C.$154,860 d. $158,060 Phillips Instruments gathered the following information pertaining to its year ended 31 December 20X9, prior to any adjustments: Net credit sales for the year $780,000 Accounts receivable, 31 Dec. 20X9 165,000 Allowance for bad debts, 31 December 20X9 3,200 cr. Ageing of accounts receivable at 31 December 20x9: 1-30 days $ 92,000 31-60 days 36,000 61-90 days 23,000 Over 90 days 14,000 Total $165,000 Refer to Table 10-4. Assume Phillips uses the percentage of sales method for estimating bad debts. Phillips estimates that uncollectable accounts will be 1.75% of net credit sales. The adjusting entry to record bad debts expense for the year is: Select one: a. Bad Debts Expense 10,450 Accounts Receivable 10,450 b. Bad Debts Expense 16,850 Accounts Receivable 16,850 c. Bad Debts Expense 13,650 Allowance for Bad Debts 13,650 d. Bad Debts Expense 10,450 Allowance for Bad Debts 10.450 Refer to Table 10-4. Assume Phillips uses the percentage of sales method for estimating bad debts. Phillips estimates that bad debts expense will be 0.6% of net credit sales. The balance in allowance for bad debts after the adjusting entry for bad debts will be: Select one: a. $1,480 b. $43,600 .$4,680 d. $7,880 Refer to Table 10-4. Assume Phillips uses the percentage of sales method for estimating bad debts. Phillips estimates that bad debts expense will be 1.3% of net credit sales. After the adjustment for bad debts is made, the net realisable value of accounts receivable will be: Select one: a. $151,660 b. $165,000 C.$154,860 d. $158,060