Answered step by step

Verified Expert Solution

Question

1 Approved Answer

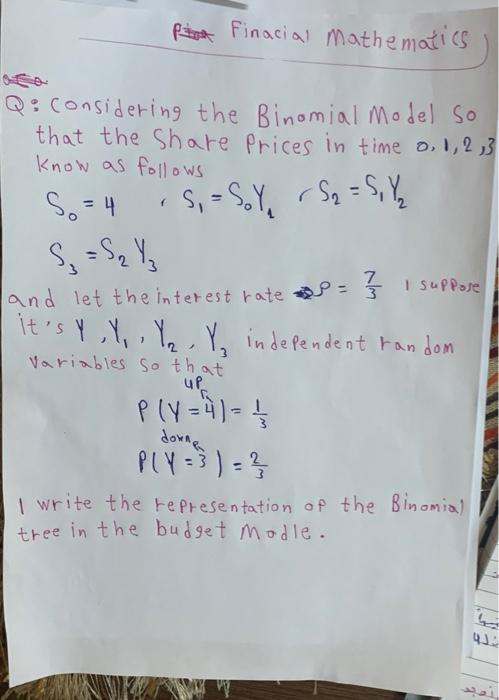

Pitzt finacial Mathematics 7 I suppose Q: considering the Binomial model so that the Share Prices in time o. 1,2,3 know as follows So=4 .SoSoy

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Professional Risk Managers Guide To Financial Market Bond Markets

Authors: Professional Risk Managers' International Association (PRMIA)

1st Edition

0071738932