Please address the case using the following case framework: Definition of the problem in strategic terms Analysis of the problem using relevant concepts and tools

Please address the case using the following case framework:

Definition of the problem in strategic terms

Analysis of the problem using relevant concepts and tools

Generation and evaluation of alternative solutions: Three alternatives with Pros and Cons

A recommendation (Based on Decision criteria)

An action plan: Follow the steps or timeline.

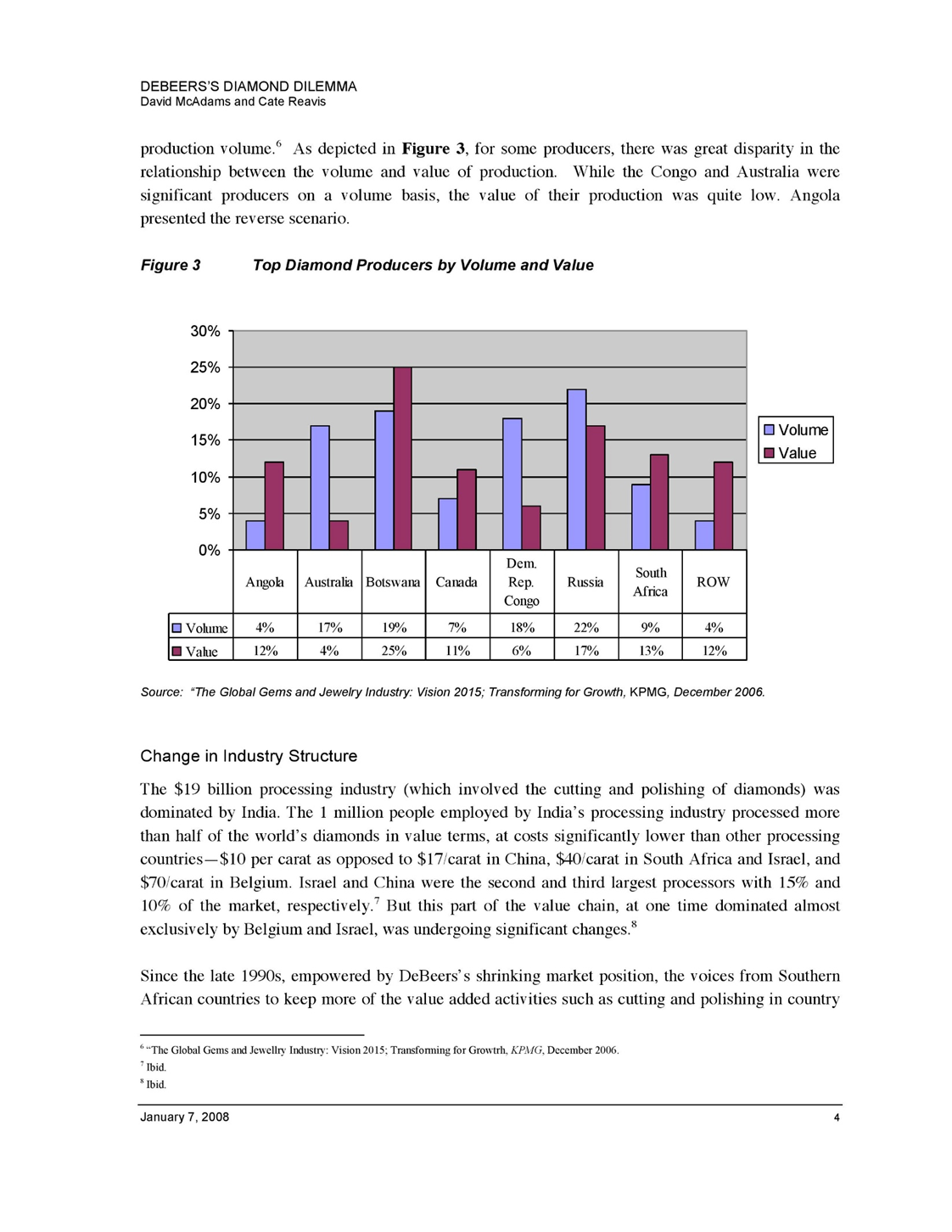

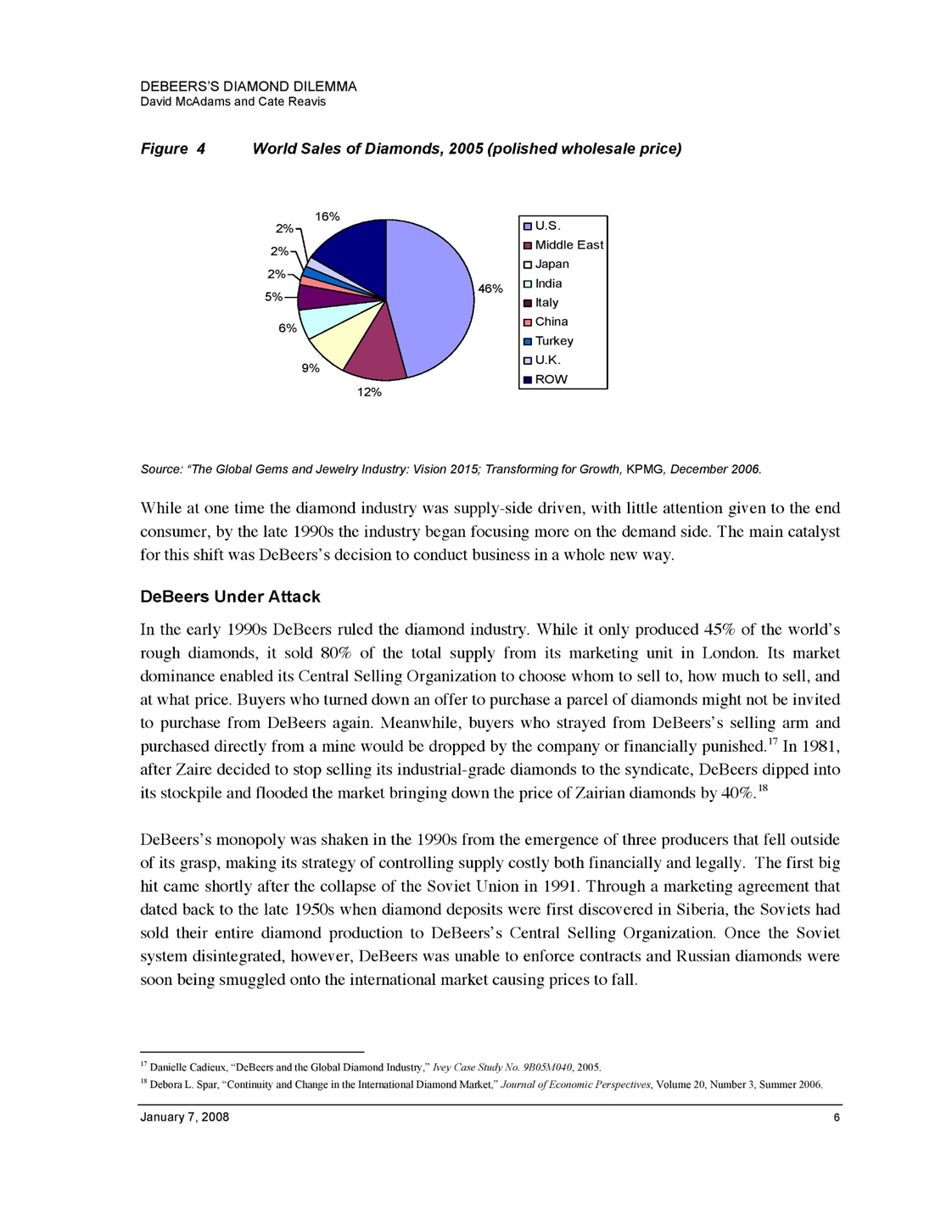

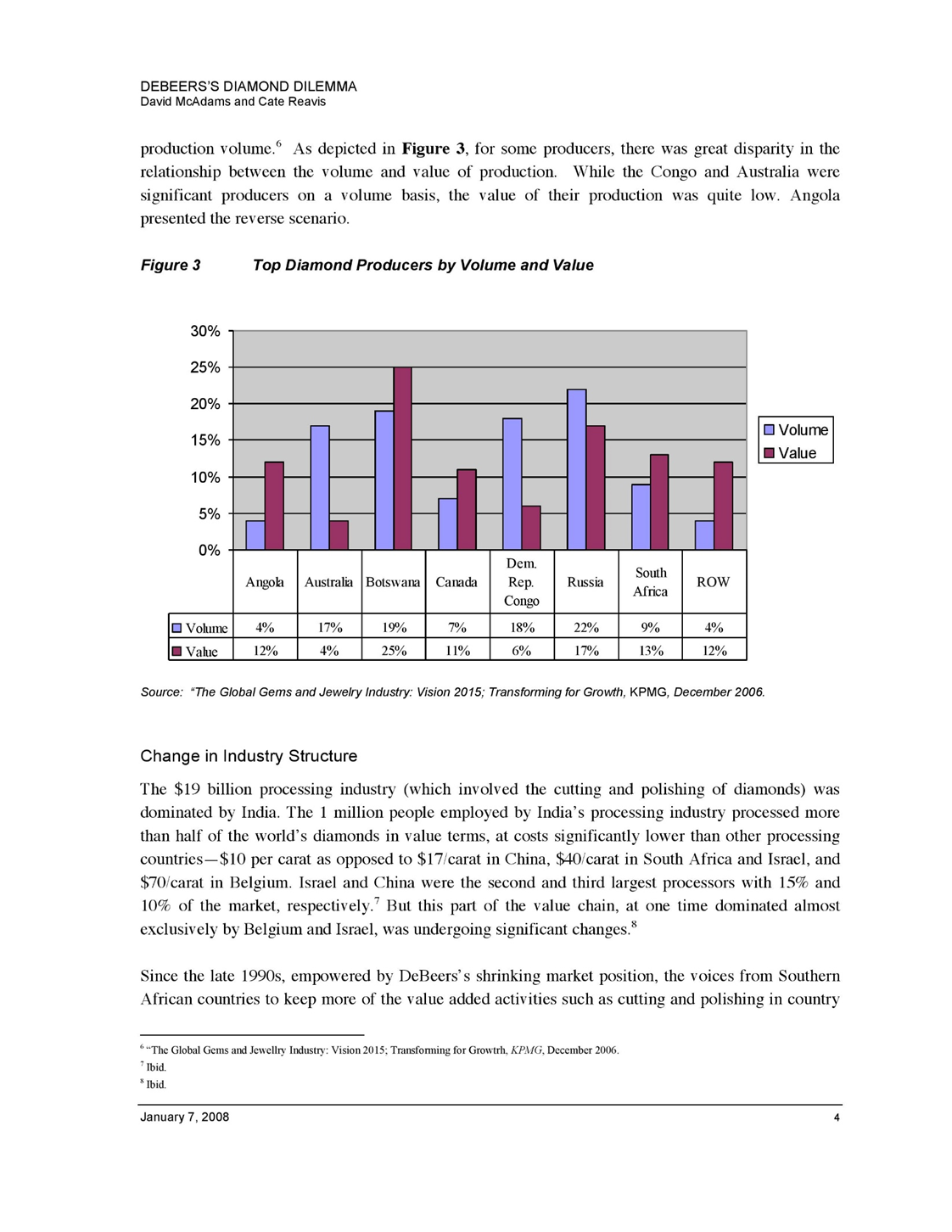

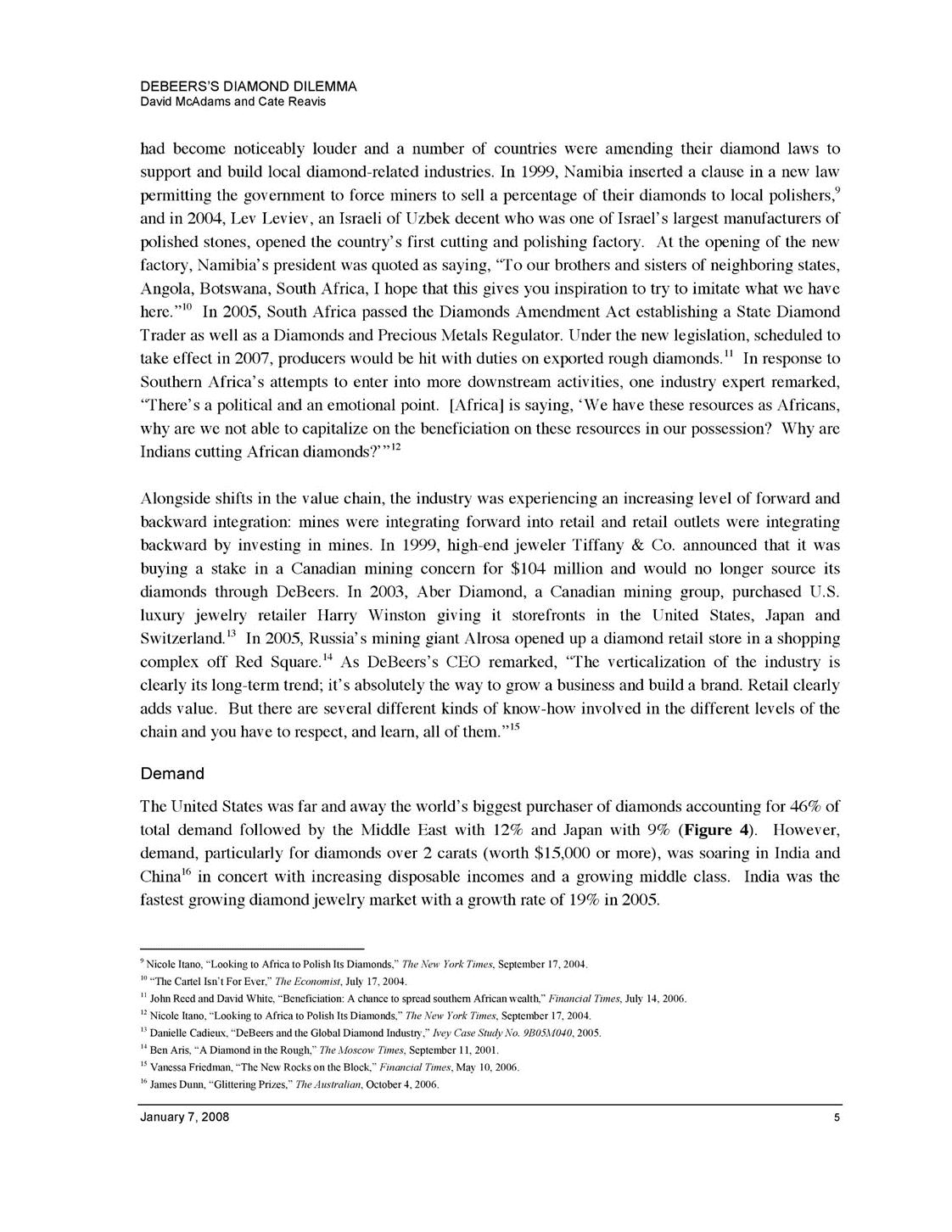

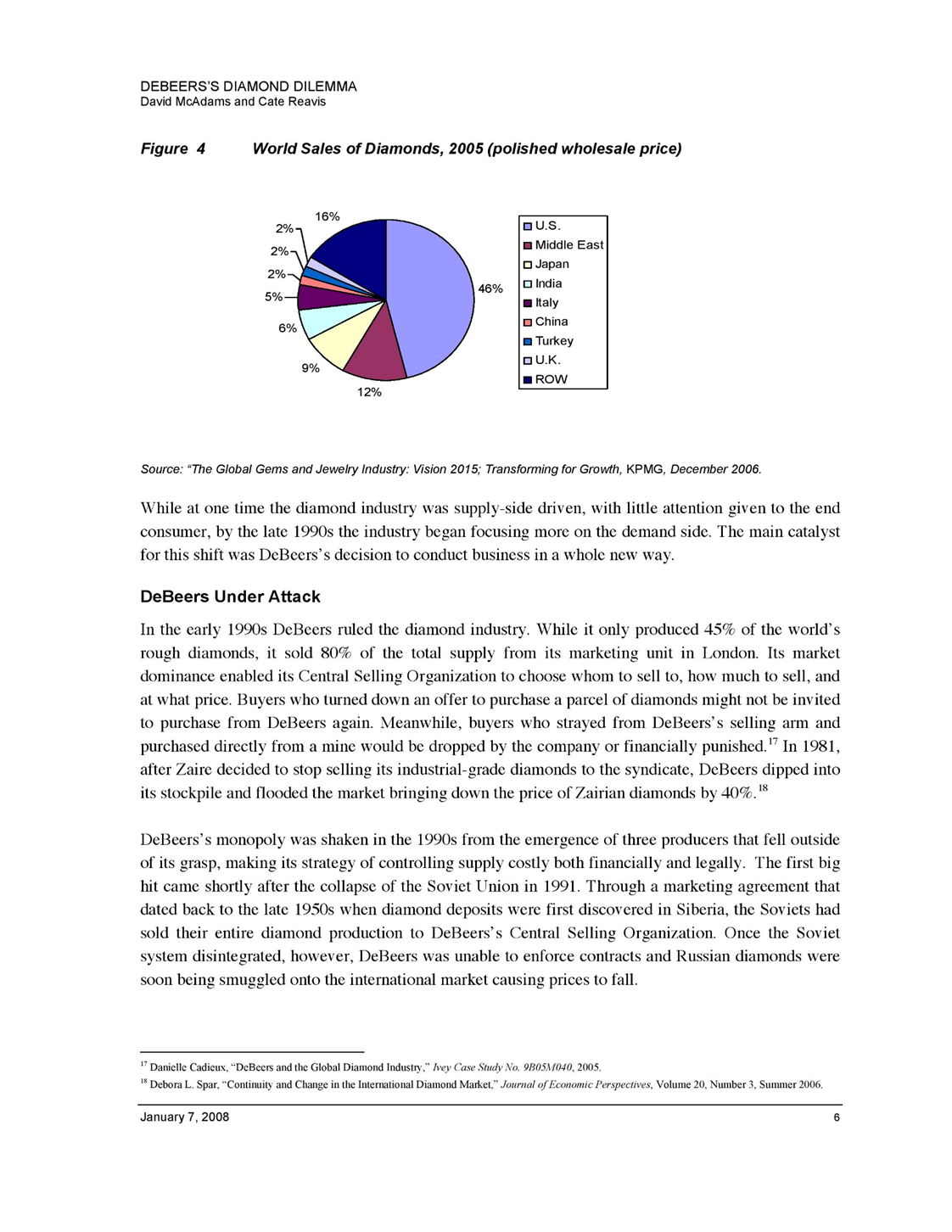

07-045 January 7, 2008 IIIIIIIIII MITSloan MANAGEMENT DeBeers's Diamond Dilemma David McAdams and Cate Reavis The mystique of natural diamonds has been built by the industry. One hundred fifty million carats of mined diamonds are produced every year, so they are really not that special if you look at those terms. -CEO of Gemesis Corporation We don't see synthetic diamonds as a threat, but you cannot ignore it completely.? -Stuart Brown, Finance Director, De Beers It was early summer 2007 and Lee Mandell decided that the time was right to propose to Diane, his girlfriend of four years. Being the romantic he was, Lee wanted to pop the question over a candle light dinner that included an exceptional bottle of Bordeaux. Logistical details of where to buy the special ring and what type of diamond, however, were less certain in his mind. Lee and Diane had recently rented the movie Blood Diamond, set in Sierra Leone in the 1990s when a civil war was raging and the rebel group, the Revolutionary United Front, relied on proceeds from smuggled diamonds to finance its military operation. The 11-year war, which ended in 2002, resulted in the deaths of tens of thousands and the displacement of more than 2 million people, nearly one- third of the country's population. Both Diane and Lee had been disturbed by the story the movie told, the hardship and violence, the children who were forcibly recruited to fight, and the lives that were destroyed all over gems that were worn by hundreds of millions of people, men and women alike, throughout the world. Karen Goldberg Goff, "Cultivated Carats," The Washington Times, February 4, 2007. Danielle Rossingh, "DeBeers Says it Can't Ignore Synthetic Diamonds," Bloomberg, May 17, 2007. This case was prepared by Cate Reavis under the supervision of Professor David McAdams. Professor McAdams is the Cecil and Ida Green Career Development Professor. Copyright @ 2008, David McAdams. This work is licensed under the Creative Commons Attribution-Noncommercial-No Derivative Works 3.0 Unported License. To view a copy of this license visit http://creativecommons.org/licenses/by-nc-nd/3.0/ or send a letter to Creative Commons, 171 Second Street, Suite 300, San Francisco, California, 94105, USADEBEERS'S DIAMOND DILEMMA David McAdams and Cate Reavis production volume." As depicted in Figure 3, for some producers, there was great disparity in the relationship between the volume and value of production. While the Congo and Australia were significant producers on a volume basis, the value of their production was quite low. Angola presented the reverse scenario. Figure 3 Top Diamond Producers by Volume and Value 30% 25% 20% O Volume 15% Value 10% 5% 0% Dem. South Angola Australia Botswana Canada Rep. Russia ROW Africa Congo Volume 4% 17% 19% 7% 18% 22% 90% 4% Value 12% 4% 25% 1 1% 6% 17% 13% 12% Source: "The Global Gems and Jewelry Industry: Vision 2015; Transforming for Growth, KPMG, December 2006. Change in Industry Structure The $19 billion processing industry (which involved the cutting and polishing of diamonds) was dominated by India. The 1 million people employed by India's processing industry processed more than half of the world's diamonds in value terms, at costs significantly lower than other processing countries-$10 per carat as opposed to $17/carat in China, $40/carat in South Africa and Israel, and $70/carat in Belgium. Israel and China were the second and third largest processors with 15% and 10% of the market, respectively." But this part of the value chain, at one time dominated almost exclusively by Belgium and Israel, was undergoing significant changes. Since the late 1990s, empowered by DeBeers's shrinking market position, the voices from Southern African countries to keep more of the value added activities such as cutting and polishing in country ""The Global Gems and Jewellry Industry: Vision 2015; Transforming for Growth, KPMG, December 2006. Ibid. Ibid. January 7, 2008DEBEERS'S DIAMOND DILEMMA David McAdams and Cate Reavis had become noticeably louder and a number of countries were amending their diamond laws to support and build local diamond-related industries. In 1999, Namibia inserted a clause in a new law permitting the government to force miners to sell a percentage of their diamonds to local polishers," and in 2004, Lev Leviev, an Israeli of Uzbek decent who was one of Israel's largest manufacturers of polished stones, opened the country's first cutting and polishing factory. At the opening of the new factory, Namibia's president was quoted as saying, "To our brothers and sisters of neighboring states, Angola, Botswana, South Africa, I hope that this gives you inspiration to try to imitate what we have here." In 2005, South Africa passed the Diamonds Amendment Act establishing a State Diamond Trader as well as a Diamonds and Precious Metals Regulator. Under the new legislation, scheduled to take effect in 2007, producers would be hit with duties on exported rough diamonds." In response to Southern Africa's attempts to enter into more downstream activities, one industry expert remarked, "There's a political and an emotional point. [Africa] is saying, 'We have these resources as Africans, why are we not able to capitalize on the beneficiation on these resources in our possession? Why are Indians cutting African diamonds?'"12 Alongside shifts in the value chain, the industry was experiencing an increasing level of forward and backward integration: mines were integrating forward into retail and retail outlets were integrating backward by investing in mines. In 1999, high-end jeweler Tiffany & Co. announced that it was buying a stake in a Canadian mining concern for $104 million and would no longer source its diamonds through DeBeers. In 2003, Aber Diamond, a Canadian mining group, purchased U.S. luxury jewelry retailer Harry Winston giving it storefronts in the United States, Japan and Switzerland." In 2005, Russia's mining giant Alrosa opened up a diamond retail store in a shopping complex off Red Square." As DeBeers's CEO remarked, "The verticalization of the industry is clearly its long-term trend; it's absolutely the way to grow a business and build a brand. Retail clearly adds value. But there are several different kinds of know-how involved in the different levels of the chain and you have to respect, and learn, all of them."15 Demand The United States was far and away the world's biggest purchaser of diamonds accounting for 46% of total demand followed by the Middle East with 12% and Japan with 9% (Figure 4). However, demand, particularly for diamonds over 2 carats (worth $15,000 or more), was soaring in India and China" in concert with increasing disposable incomes and a growing middle class. India was the fastest growing diamond jewelry market with a growth rate of 19% in 2005. Nicole Itano, "Looking to Africa to Polish Its Diamonds," The New York Times, September 17, 2004. 10 "The Cartel Isn't For Ever." The Economist, July 17, 2004 " John Reed and David White, "Beneficiation: A chance to spread southern African wealth," Financial Times, July 14, 2006. 12 Nicole Itano, "Looking to Africa to Polish Its Diamonds," The New York Times, September 17, 2004. " Danielle Cadieux. "DeBeers and the Global Diamond Industry." Ivey Case Study No. 9805M1040, 2005. " Ben Aris, "A Diamond in the Rough," The Moscow Times, September 11, 2001. 15 Vanessa Friedman, "The New Rocks on the Block," Financial Times, May 10, 2006. James Dunn, "Glittering Prizes." The Australian, October 4, 2006. January 7, 2008DEBEERS'S DIAMOND DILEMMA David McAdams and Cate Reavis Figure 4 World Sales of Diamonds, 2005 (polished wholesale price) 16% 2% O U.S. 2%- Middle East Japan 2%~ 46% India 5% Italy 6% China Turkey O U.K. 9% ROW 12% Source: "The Global Gems and Jewelry Industry: Vision 2015; Transforming for Growth, KPMG, December 2006. While at one time the diamond industry was supply-side driven, with little attention given to the end consumer, by the late 1990s the industry began focusing more on the demand side. The main catalyst for this shift was DeBeers's decision to conduct business in a whole new way. DeBeers Under Attack In the early 1990s DeBeers ruled the diamond industry. While it only produced 45% of the world's rough diamonds, it sold 80% of the total supply from its marketing unit in London. Its market dominance enabled its Central Selling Organization to choose whom to sell to, how much to sell, and at what price. Buyers who turned down an offer to purchase a parcel of diamonds might not be invited to purchase from DeBeers again. Meanwhile, buyers who strayed from DeBeers's selling arm and purchased directly from a mine would be dropped by the company or financially punished." In 1981, after Zaire decided to stop selling its industrial-grade diamonds to the syndicate, DeBeers dipped into its stockpile and flooded the market bringing down the price of Zairian diamonds by 40%. 18 DeBeers's monopoly was shaken in the 1990s from the emergence of three producers that fell outside of its grasp, making its strategy of controlling supply costly both financially and legally. The first big hit came shortly after the collapse of the Soviet Union in 1991. Through a marketing agreement that dated back to the late 1950s when diamond deposits were first discovered in Siberia, the Soviets had sold their entire diamond production to DeBeers's Central Selling Organization. Once the Soviet system disintegrated, however, DeBeers was unable to enforce contracts and Russian diamonds were soon being smuggled onto the international market causing prices to fall. " Danielle Cadieux, "DeBeers and the Global Diamond Industry," Ivey Case Study No. 9805M040, 2005. " Debora L. Spar, "Continuity and Change in the International Diamond Market," Journal of Economic Perspectives, Volume 20, Number 3, Summer 2006. January 7, 2008DEBEERS'S DIAMOND DILEMMA David McAdams and Cate Reavis But DeBeers's challenges in Russia could not be blamed solely on the country's economic and political upheaval. Lev Leviev, one of Israel's largest manufacturers of polished stones, was making his move in Russia where he was well connected politically. In 1989, two years after Leviev became a sightholder for DeBeers, Russia's state-run diamond mining and trading group, now known as Alrosa, entered into a joint venture with Leviev to establish the country's first cutting factory, the stones of which would be supplied directly by Russian mines, not through DeBeers." The partnership marked the first time in which rough diamonds were cut in their country of origin. Over the next five years, Leviev's position in the Russian diamond industry grew to the point where, in 1995, DeBeers terminated his sightholder status. 20 The second jolt to DeBeers's position came in 1996 with the decision by Australia's Argyle diamond mine, which produced low quality diamonds suitable for inexpensive jewelry, to terminate its contract with DeBeers and begin marketing its own diamonds. It sold 42 million carats directly to polishers in Antwerp that year."' Finally, the emergence of Canada in the early 1990s as a diamond producer served as a further threat to DeBeers's position. While the company was successful in acquiring stakes in a couple of Canadian mines, the majority of the country's production fell outside of its control. In order to keep prices high, therefore safeguard its market dominance, DeBeers was forced to both hold back a large portion of its diamonds from the market and purchase much of the excess supply from these producing countries often at inflated prices. By the end of the 1990s, DeBeers's market share had fallen from 85% to 65% while its diamond stockpile had grown from $2.5 billion to $5 billion. Between December 1989 and 1998 DeBeers's share price fell from $17 to $12, a nearly 30% drop. 22 In addition to the financial sting DeBeers was feeling resulting from its supply-side strategy, antitrust regulators in the United States and the European Union were becoming increasingly aggressive in their attempts to formally end the company's price control practices. In a 1994 indictment, the United States accused DeBeers of violating the Sherman Antitrust Act by fixing the price of industrial diamonds. The government contended that a subsidiary of DeBeers conspired with General Electric, another producer of industrial diamond products, to fix the world prices of industrial diamonds in 1991 and 1992. While the United States Justice Department was unable to prosecute DeBeers because its operations were overseas and it refused to subject itself to the jurisdiction of an American court, the company was prohibited from conducting business in the United States. 19 "The Cartel Isn't Forever." The Economist, July 17, 2004. 20 Phyllis Berman and Lea Goldman, "Cracked DeBeers," Forbes.com, September 15, 2003. 21 Ibid. 2Nicholas Stein, "The DeBeers Story: A New Cut On An Old Monopoly." Fortune, February 19, 2001. January 7, 2008DEBEERS'S DIAMOND DILEMMA David Mandamus and Gate Reavis On a completely different front. DeBeers faced yet another threat, which was quickly turning into a public relations nightmare for the entire diamond industry. In the mid1990s, Angola, the world's third largest producer of rough diamonds, was overrun by rebel forces opposed to President Dos Santos. Gaining control of the country's diamond supplies, the rebels flooded the market with up to $l.2 billion worth of rough diamonds. To maintain control over supply, therefore prices, DeBeers had little choice hilt to buy what were becoming known as \"blood diamonds,\" the proceeds of which went toward financing the armed eoniet. Angola was not a lone participant in the blood diamond trade. Rebel forces in Sierra Leone, Liberia, and the Democratic Republic of the Congo were also using the illicit diamond trade to finance their respective armed conflicts. Delleers's involvement in the \"blood diamond" trade was exposed in a 1998 report by Global \\\\-"itness which accused the company of \"operatlingl with an extraordinary lack of z-iceounlabilily."23 As Martin Rapaport, publisher of the diamond industry pricing guide, asked rhetorically, \"How can it be that tens of millions of dollars are exported from diamond areas and yet there is no electricity, no plumbing, no wells, no improvement in the lives of the people?" Rapaport went on to ask the more complicated question of, \"Do we owe anything to the people of .-\\ frica just because we buy their diamonds? Are we responsible for what we buy?"24 For DcBecrs, these challenges and threats in aggregate were creating a \"perfect storm\" of sorts. Significant changes to the company's strategy that had served it well for decades had to be made. A New Direction In 1998, on the advice of US. consulting firm Rain and Company, DeBecrs decided to \"ditch its role of buyer of last resort" and develop a strategy that was demand~driven and brand focused whereby profits were more important than market share.25 When explaining its strategic shift, Deliecrs's Managing Director stated, \"'tVe don't have to go rushing about the world trying to buy every diamond. What is the point of us buying diamonds close to or over our selling prices? It's silly. I'm perfectly happy to market 60%. What I want to do is differentiate the portion that does come to us and create value on those goods. .. in order to sell them first, more advantageously, and at 5'2!) better prices. As a part of its strategy. DeBeers ended its practice of stockpiling diamonds, stopped buying diamonds on the open market. and began only selling diamonds from its own operations which enabled it to guarantee that its supply was \"conict free." The company promised the European I'nion it would stop buying diamonds from Alrosa, the statenowned Russian firm that accounted for 3" WI} Ills Bermau and Lea Goldman. \"(ticked DeBeers_" .f'iirhr'x

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance