please amswer these questions

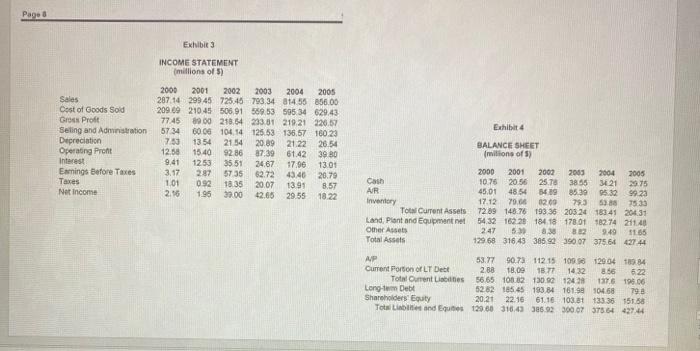

Case Study Instructions . . . . Assuming the role of the accounting firm hired to complete the second review, prepare a two page memorandum that analyses the financial condition of California Choppers and makes suggestions for improvement. The memo should be divided into sections describing a) Liquidity, b) Asset Management, c) Long term debt paying ability d) Profitability e) Recommendations Prepare the following exhibits for 2000-2005 Ratio tables incorporating only the ratios for which the industry averages are provided vertical analysis of income statements and balance sheets horizontal analysis (index numbers) of income statements and balance sheets a five-part analysis of return on investment (ROE) and . a cash flow statement Also in your write-up, comment on the performance of the CEO, Jane Heathcliff and her working relationship with Arlen Doakes. . . . Page 3 Exhibit 3 INCOME STATEMENT millions of 5) Exhibit Sales Cost of Goods Sold Gross Profit Seling and Administration Depreciation Operating Pront Interest Emmings Before Taxes Taxes Net Income 2000 2001 2002 2003 2004 2005 287 14 299 45 725.45 793.34 314 58 856.00 209.09 210 45 506.91 569.53 595 34 629.43 77.45 89.00 218.54 233.81 21921 920,67 5734 6006 104 14 125 53 136.57 160.23 733 1354 2154 20.89 21.22 2654 12.50 15.40 87:39 6142 39 BO 9.41 1253 24.67 17.96 13.01 3.17 287 62.72 4340 26.79 101 092 18:35 13.91 8.57 2.16 195 42.65 29.55 18.22 BALANCE SHEET milions of 5) 9286 3551 5735 2007 30.00 Cash AJR Inventory Tot Current Assets Land, Plant and Equipment Omer Assets Total Assets 2000 2001 2002 2003 2004 2005 10.76 20:56 25. Te 38.55 34.21 29.75 45.01 4854 5489 85.39 $5.32 99.23 17.12 79,64 02.00 79.3 5388 7535 7289 148.76 193.36 20324 18341 20431 543216220 184.18 17801 18274 211.40 247 5.30 8.30 9:49 1165 129 68 31643 385 92 390 0737566 427 44 AP 53.77 90.73 112 15 109.56 129 04 183 84 Current Portion of LT Debt 2.88 18.00 18.77 1432 856 622 Total Current Lines 56 65 100 2 130.92 12428 136196.00 Long tum Debt 5282 185.45 193,84 161.99 10468 79 e Shareholders' Equity 20 21 22.10 61.16 103.8t 1333615158 Total Liband Equit 120.60 31643 306 92 300.07 375 64 427.44 CASE SUMMARY With a dramatic downturn in profitability in 2005, the advisory board for California Choppers (CC), with the concurrence of the owner, Arlen Doakes, agreed to hire another consulting group to review operations and make suggestions for getting the company "back on track." Secretly, Doakes hoped this review would give him the ammunition he needed to terminate the current chief executive officer (CEO), Jane Heathcliff, whose cautious manner, Doakes felt had been a drag on company expansion. . CC was a manufacturer of large, high-end motorcycles that catered primarily to older, wealthier motorcycle enthusiasts who were trying to regain some of the excitement of their youth. The custom choppers produced were sold through an online auction service, and the proceeds were denoted to motorcycle safety programs in a number of western states. The company also generated modest revenues by licensing its logo for t-shirts and posters. Up to 2000, CC's sales were largely in the states of California, Arizona, Nevada, New Mexico, Oregon and Washington. In 2001, the company undertook a major expansion in order to develop the remainder of the U.S. market with hopes of possibly growing overseas. The decision to expand was based on a review the company had had done of its operations, which resulted in a scathing evaluation of its performance. Not only was the company not effectively developing its markets, its production processes were found to be inefficient, its operating costs were excessive, and its use of financial leverage was far too high. Doakes had strong technical knowledge of motorcycles, but he did not have the business sense and discipline needed to operate what had become a major corporation. He also enjoyed a very luxurious lifestyle, recycling little of his profits back into the company prior to 2000. In 2001, Doakes agreed to step down as CEO and hired Jane Heathcliff, P. Eng., as his replacement. Heathcliff had over 20 years of engineering and management experience at another major domestic motorcycle manufacturer, and she was highly respected by her colleagues. Also, based on advice from the consultants, Doakes organized a corporate advisory board made up of experienced industry professionals with whom he had strong personal relationships. . Prior to 2000, CC's performance was poor, but its non-unionized workforce continued to receive above-average wage rates. Also, he had refused repeated requests by his production staff to outsource the production of parts to lower-wages factories in Mexico and Asia. Arlen Doakes was truly a "flag waving" American, and he felt strongly that a California Chopper should be "Made in the U.S.A." In late 2003, CC gave its workforce a large increase in wages and benefits, and Arlen Doakes made a public announcement that the company must share its new-found success with its workforce. CC offered its customers industry-average credit terms of net 30, but varied from that regularly in order to provide encouragement to new dealers to carry CC's products. CC also received credit terms of net 60 on average for its purchases of parts and supplies. It the past, the company had regularly stretched its payables in order to generate needed cash flows, but Heathcliff was committed to stopping this practice, after receiving complaints and some threats from suppliers. Purchases of land, plant and equipment were financed through a combination of mortgages and term loans. These loans had, as requirements, that the company maintain a current ratio of 1.25 and a times interest earned of 2.0, although CC's bank had been very lenient on these conditions in the past due to a strong personal relationship between Arlen Doakes and his lending officer and her superiors. Case Study Instructions . . . . Assuming the role of the accounting firm hired to complete the second review, prepare a two page memorandum that analyses the financial condition of California Choppers and makes suggestions for improvement. The memo should be divided into sections describing a) Liquidity, b) Asset Management, c) Long term debt paying ability d) Profitability e) Recommendations Prepare the following exhibits for 2000-2005 Ratio tables incorporating only the ratios for which the industry averages are provided vertical analysis of income statements and balance sheets horizontal analysis (index numbers) of income statements and balance sheets a five-part analysis of return on investment (ROE) and . a cash flow statement Also in your write-up, comment on the performance of the CEO, Jane Heathcliff and her working relationship with Arlen Doakes. . . . Page 3 Exhibit 3 INCOME STATEMENT millions of 5) Exhibit Sales Cost of Goods Sold Gross Profit Seling and Administration Depreciation Operating Pront Interest Emmings Before Taxes Taxes Net Income 2000 2001 2002 2003 2004 2005 287 14 299 45 725.45 793.34 314 58 856.00 209.09 210 45 506.91 569.53 595 34 629.43 77.45 89.00 218.54 233.81 21921 920,67 5734 6006 104 14 125 53 136.57 160.23 733 1354 2154 20.89 21.22 2654 12.50 15.40 87:39 6142 39 BO 9.41 1253 24.67 17.96 13.01 3.17 287 62.72 4340 26.79 101 092 18:35 13.91 8.57 2.16 195 42.65 29.55 18.22 BALANCE SHEET milions of 5) 9286 3551 5735 2007 30.00 Cash AJR Inventory Tot Current Assets Land, Plant and Equipment Omer Assets Total Assets 2000 2001 2002 2003 2004 2005 10.76 20:56 25. Te 38.55 34.21 29.75 45.01 4854 5489 85.39 $5.32 99.23 17.12 79,64 02.00 79.3 5388 7535 7289 148.76 193.36 20324 18341 20431 543216220 184.18 17801 18274 211.40 247 5.30 8.30 9:49 1165 129 68 31643 385 92 390 0737566 427 44 AP 53.77 90.73 112 15 109.56 129 04 183 84 Current Portion of LT Debt 2.88 18.00 18.77 1432 856 622 Total Current Lines 56 65 100 2 130.92 12428 136196.00 Long tum Debt 5282 185.45 193,84 161.99 10468 79 e Shareholders' Equity 20 21 22.10 61.16 103.8t 1333615158 Total Liband Equit 120.60 31643 306 92 300.07 375 64 427.44 CASE SUMMARY With a dramatic downturn in profitability in 2005, the advisory board for California Choppers (CC), with the concurrence of the owner, Arlen Doakes, agreed to hire another consulting group to review operations and make suggestions for getting the company "back on track." Secretly, Doakes hoped this review would give him the ammunition he needed to terminate the current chief executive officer (CEO), Jane Heathcliff, whose cautious manner, Doakes felt had been a drag on company expansion. . CC was a manufacturer of large, high-end motorcycles that catered primarily to older, wealthier motorcycle enthusiasts who were trying to regain some of the excitement of their youth. The custom choppers produced were sold through an online auction service, and the proceeds were denoted to motorcycle safety programs in a number of western states. The company also generated modest revenues by licensing its logo for t-shirts and posters. Up to 2000, CC's sales were largely in the states of California, Arizona, Nevada, New Mexico, Oregon and Washington. In 2001, the company undertook a major expansion in order to develop the remainder of the U.S. market with hopes of possibly growing overseas. The decision to expand was based on a review the company had had done of its operations, which resulted in a scathing evaluation of its performance. Not only was the company not effectively developing its markets, its production processes were found to be inefficient, its operating costs were excessive, and its use of financial leverage was far too high. Doakes had strong technical knowledge of motorcycles, but he did not have the business sense and discipline needed to operate what had become a major corporation. He also enjoyed a very luxurious lifestyle, recycling little of his profits back into the company prior to 2000. In 2001, Doakes agreed to step down as CEO and hired Jane Heathcliff, P. Eng., as his replacement. Heathcliff had over 20 years of engineering and management experience at another major domestic motorcycle manufacturer, and she was highly respected by her colleagues. Also, based on advice from the consultants, Doakes organized a corporate advisory board made up of experienced industry professionals with whom he had strong personal relationships. . Prior to 2000, CC's performance was poor, but its non-unionized workforce continued to receive above-average wage rates. Also, he had refused repeated requests by his production staff to outsource the production of parts to lower-wages factories in Mexico and Asia. Arlen Doakes was truly a "flag waving" American, and he felt strongly that a California Chopper should be "Made in the U.S.A." In late 2003, CC gave its workforce a large increase in wages and benefits, and Arlen Doakes made a public announcement that the company must share its new-found success with its workforce. CC offered its customers industry-average credit terms of net 30, but varied from that regularly in order to provide encouragement to new dealers to carry CC's products. CC also received credit terms of net 60 on average for its purchases of parts and supplies. It the past, the company had regularly stretched its payables in order to generate needed cash flows, but Heathcliff was committed to stopping this practice, after receiving complaints and some threats from suppliers. Purchases of land, plant and equipment were financed through a combination of mortgages and term loans. These loans had, as requirements, that the company maintain a current ratio of 1.25 and a times interest earned of 2.0, although CC's bank had been very lenient on these conditions in the past due to a strong personal relationship between Arlen Doakes and his lending officer and her superiors