Answered step by step

Verified Expert Solution

Question

1 Approved Answer

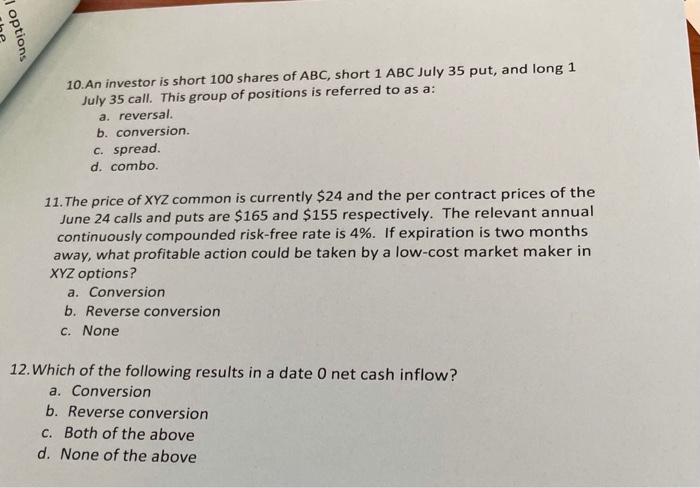

please answer 10,11,12 options 10. An investor is short 100 shares of ABC, short 1 ABC July 35 put, and long 1 July 35 call.

please answer 10,11,12

options 10. An investor is short 100 shares of ABC, short 1 ABC July 35 put, and long 1 July 35 call. This group of positions is referred to as a: a. reversal. b. conversion. c. spread. d. combo. 11. The price of XYZ common is currently $24 and the per contract prices of the June 24 calls and puts are $165 and $155 respectively. The relevant annual continuously compounded risk-free rate is 4%. If expiration is two months away, what profitable action could be taken by a low-cost market maker in XYZ options? a. Conversion b. Reverse conversion c. None 12. Which of the following results in a date 0 net cash inflow? a. Conversion b. Reverse conversion c. Both of the above d. None of the above Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Currency Wars Offense And Defense Through Systemic Thinking

Authors: Jeffrey Yi-Lin Forrest , Yirong Ying , Zaiwu Gong

1st Edition

3319677640,3319677659