Answered step by step

Verified Expert Solution

Question

1 Approved Answer

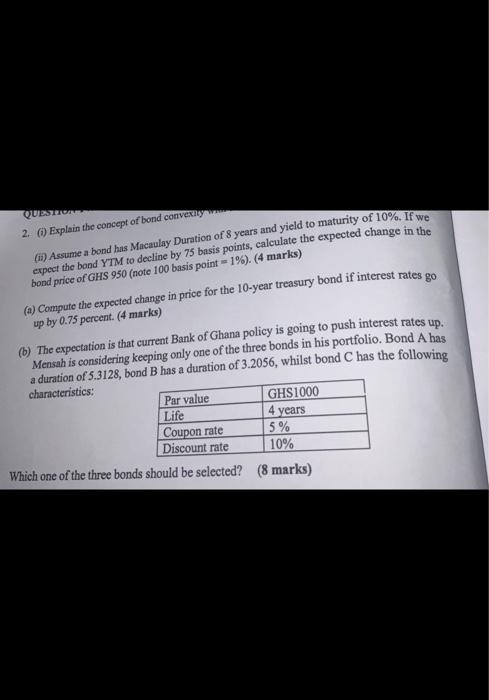

please answer a question ii 2. (i) Explain the concept of bond convextly (ii) Assume a bond has Macaulay Duration of 8 years and yield

please answer a question ii

2. (i) Explain the concept of bond convextly (ii) Assume a bond has Macaulay Duration of 8 years and yield to maturity of 10%. If we expect the bond YTM to decline by 75 basis points, calculate the expected change in the bond price of GHS 950 (note 100 basis point =1% ). ( 4 marks) (a) Compute the expected change in price for the 10-year treasury bond if interest rates go up by 0.75 percent. ( 4 marks) (b) The expectation is that current Bank of Ghana policy is going to push interest rates up. Mensah is considering keeping only one of the three bonds in his portfolio. Bond A has a duration of 5.3128 , bond B has a duration of 3.2056 , whilst bond C has the following characteristics: Which one of the three bonds should be selected? (8 marks) Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Management Core Concepts

Authors: Ray Brooks, Raymond Brooks

1st Edition

0321155173, 9780321155177