Answered step by step

Verified Expert Solution

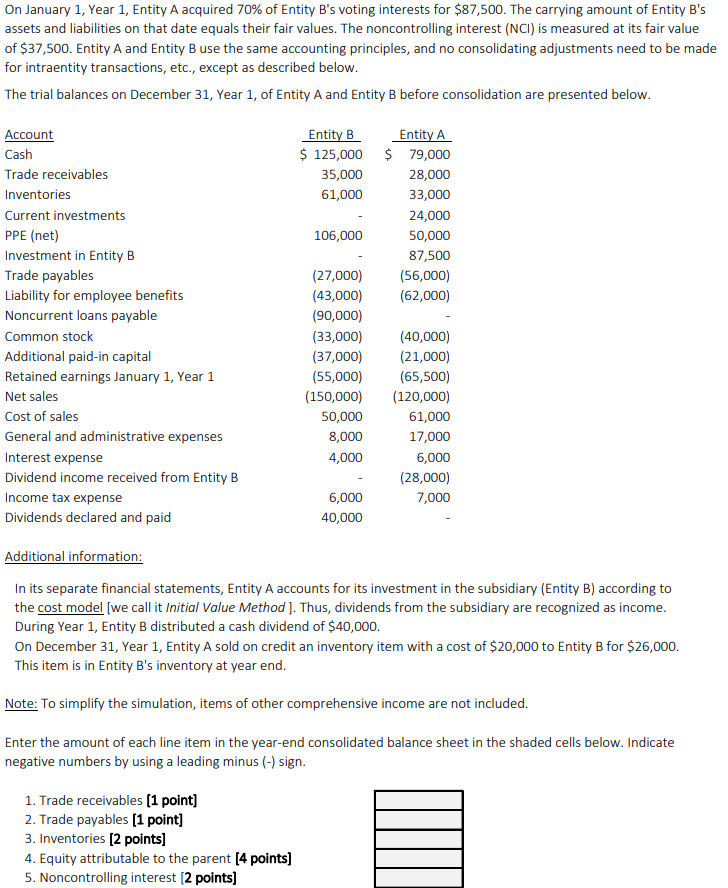

Question

1 Approved Answer

Please answer all blanks below. On January 1, Year 1, Ent'rty A acquired 70% of Entity B's voting interests for $31500. The carrying amount of

Please answer all blanks below.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Interpreting And Analyzing Financial Statements

Authors: Karen P Schoenebeck, Mark P Holtzman

5th Edition

0136121985, 9780136121985