Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Please answer all for a good rating and like!! Thanks :) begin{tabular}{|r|r|r|r|} hline 42 & 2003 & 31.77 & 1.02 hline 43 & 2004

Please answer all for a good rating and like!! Thanks :)

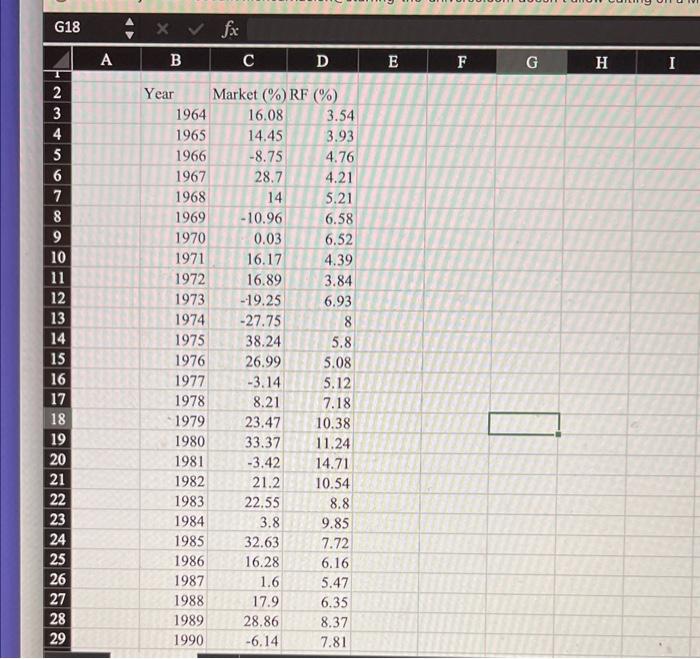

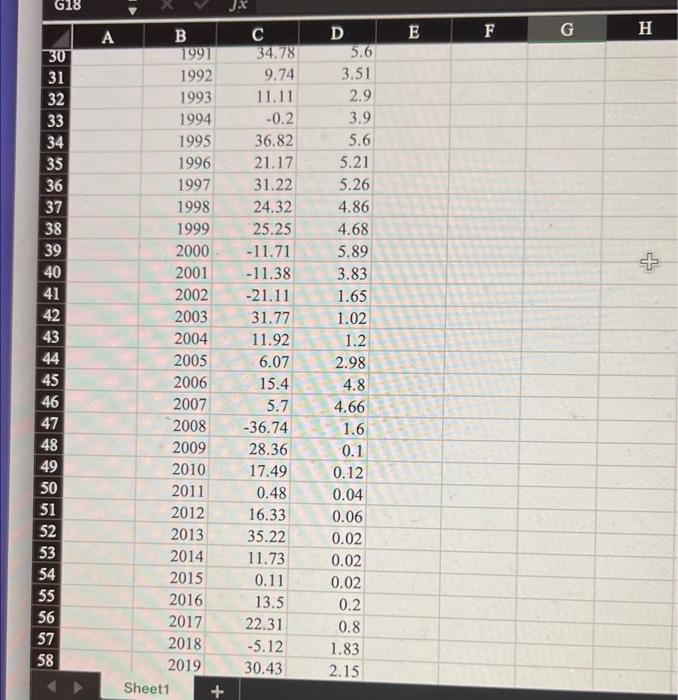

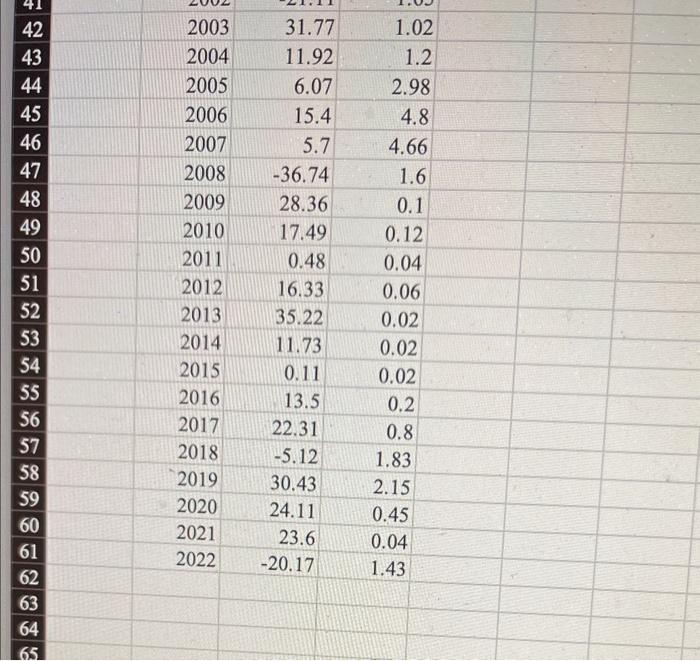

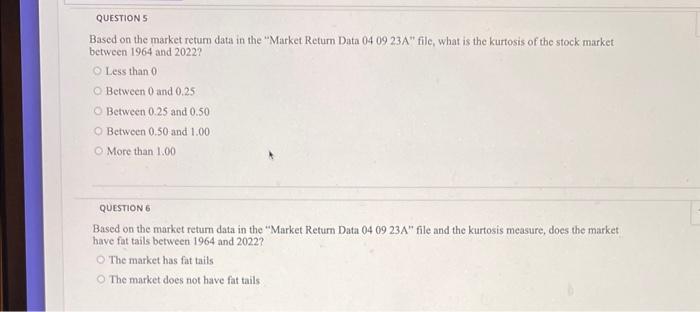

\begin{tabular}{|r|r|r|r|} \hline 42 & 2003 & 31.77 & 1.02 \\ \hline 43 & 2004 & 11.92 & 1.2 \\ \hline 44 & 2005 & 6.07 & 2.98 \\ \hline 45 & 2006 & 15.4 & 4.8 \\ \hline 46 & 2007 & 5.7 & 4.66 \\ \hline 47 & 2008 & -36.74 & 1.6 \\ \hline 48 & 2009 & 28.36 & 0.1 \\ \hline 49 & 2010 & 17.49 & 0.12 \\ \hline 50 & 2011 & 0.48 & 0.04 \\ \hline 51 & 2012 & 16.33 & 0.06 \\ \hline 52 & 2013 & 35.22 & 0.02 \\ \hline 53 & 2014 & 11.73 & 0.02 \\ \hline 54 & 2015 & 0.11 & 0.02 \\ \hline 55 & 2016 & 13.5 & 0.2 \\ \hline 56 & 2017 & 22.31 & 0.8 \\ \hline 57 & 2018 & -5.12 & 1.83 \\ \hline 58 & 2019 & 30.43 & 2.15 \\ \hline 59 & 2020 & 24.11 & 0.45 \\ \hline 60 & 2021 & 23.6 & 0.04 \\ \hline 61 & 2022 & -20.17 & 1.43 \\ \hline 62 & & & \\ \hline \end{tabular} Based on the market return data in the "Market Return Data 040923A " filc, what is the kurtosis of the stock market between 1964 and 2022 ? Less than Between 0 and 0.25 Between 0.25 and 0.50 Between 0.50 and 1.00 More than 1.00 QUESTION 6 Based on the market return data in the "Market Retum Data 040923A file and the kurtosis measure, does the market have fat tails between 1964 and 2022 ? The market has fat tails The market does not have fat tails Based on the market retum and risk free rate data in the "Market Return Data 040923A" file what was the average (arithmetic) market risk premium between 1964 and 2022 ? Less than 7.00% Between 7.00% and 7.50% Between 7.50% and 8.00% Between 8.00% and 8.50% More than 8.50% QUESTION 8 Based on the market return data in the "Market Return Data 040923A" file, what is the standard deviation of the stock market's retum between 1964 and 2022 ? Less than 15\% Between 15% and 16% Between 16% and 17% Between 17% and 18% More than 18\% Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Risk Adjusted Performance And Bank Governance Structures

Authors: Christoph Böhm

1st Edition

3631639163, 3653027306, 9783631639160, 9783653027303