Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Please answer all Questions and provide working out A stock price has an expected return of 5% and a volatility of 30% per year. The

Please answer all Questions and provide working out

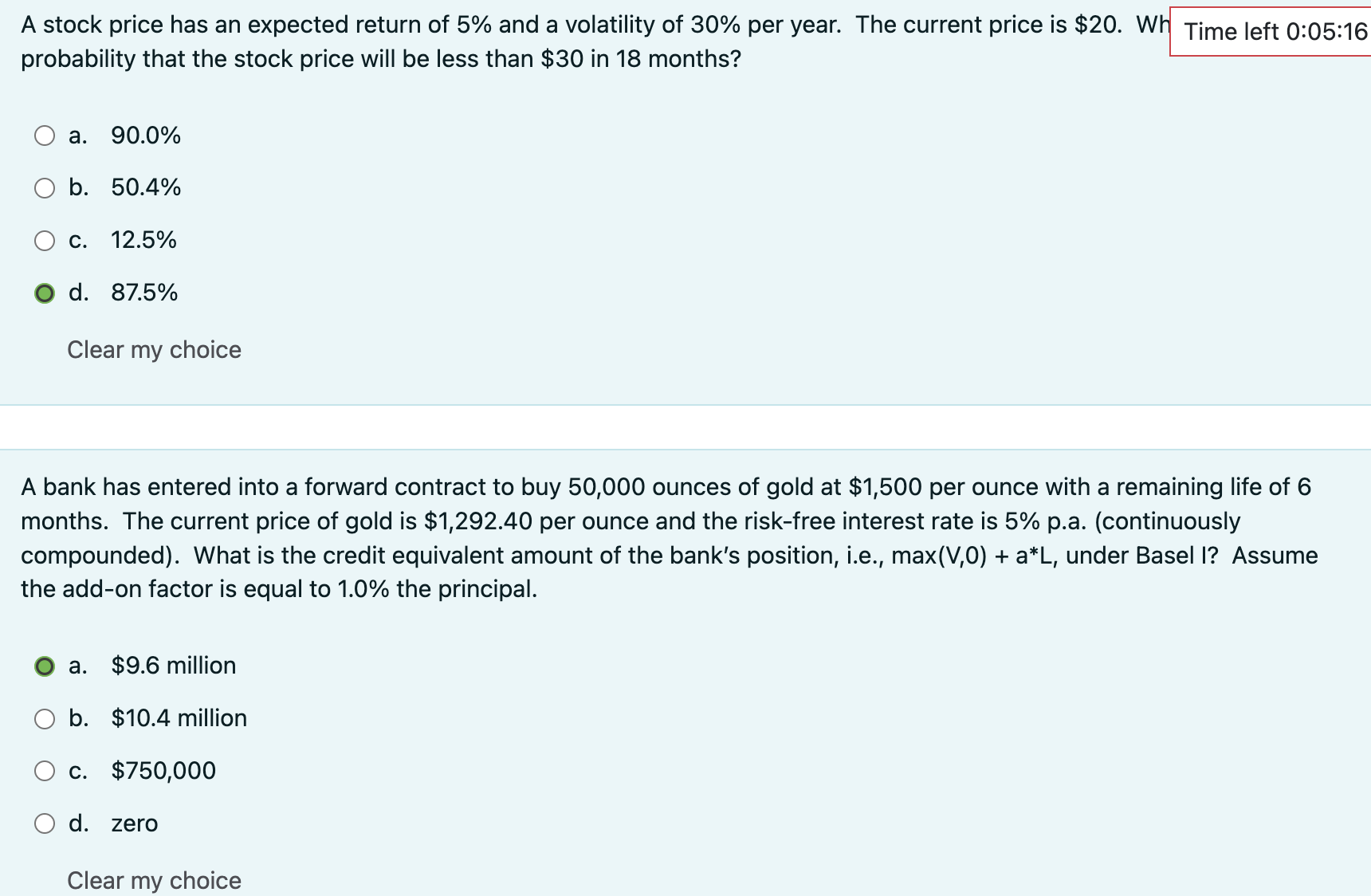

A stock price has an expected return of 5% and a volatility of 30% per year. The current price is $20. Wr probability that the stock price will be less than $30 in 18 months? a. 90.0% b. 50.4% c. 12.5% d. 87.5% Clear my choice A bank has entered into a forward contract to buy 50,000 ounces of gold at $1,500 per ounce with a remaining life of 6 months. The current price of gold is $1,292.40 per ounce and the risk-free interest rate is 5% p.a. (continuously compounded). What is the credit equivalent amount of the bank's position, i.e., max(V,0)+aL, under Basel I? Assume the add-on factor is equal to 1.0% the principal. a. \$9.6 million b. $10.4 million C. $750,000 d. zero Clear my choice

A stock price has an expected return of 5% and a volatility of 30% per year. The current price is $20. Wr probability that the stock price will be less than $30 in 18 months? a. 90.0% b. 50.4% c. 12.5% d. 87.5% Clear my choice A bank has entered into a forward contract to buy 50,000 ounces of gold at $1,500 per ounce with a remaining life of 6 months. The current price of gold is $1,292.40 per ounce and the risk-free interest rate is 5% p.a. (continuously compounded). What is the credit equivalent amount of the bank's position, i.e., max(V,0)+aL, under Basel I? Assume the add-on factor is equal to 1.0% the principal. a. \$9.6 million b. $10.4 million C. $750,000 d. zero Clear my choice Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Green And Sustainable Finance

Authors: Simon Thompson

2nd Edition

1398609242, 978-1398609242