Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Please answer all Questions and provide working out Using Delta-Hedging to hedge the risk in a short position in an option, the cost of hedging

Please answer all Questions and provide working out

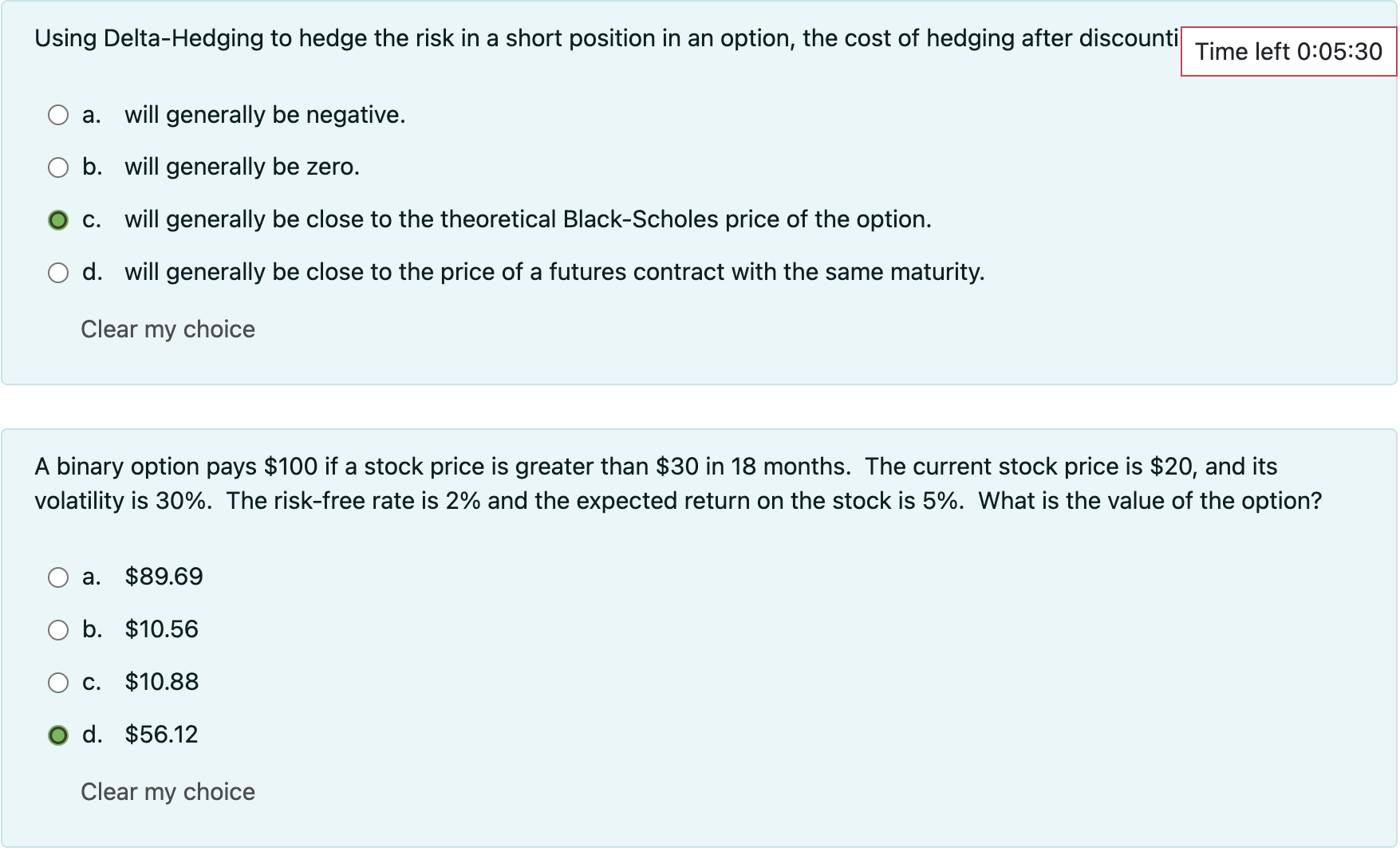

Using Delta-Hedging to hedge the risk in a short position in an option, the cost of hedging after discounti a. will generally be negative. b. will generally be zero. c. will generally be close to the theoretical Black-Scholes price of the option. d. will generally be close to the price of a futures contract with the same maturity. Clear my choice A binary option pays $100 if a stock price is greater than $30 in 18 months. The current stock price is $20, and its volatility is 30%. The risk-free rate is 2% and the expected return on the stock is 5%. What is the value of the option? a. $89.69 b. $10.56 c. $10.88 d. $56.12 Clear my choice

Using Delta-Hedging to hedge the risk in a short position in an option, the cost of hedging after discounti a. will generally be negative. b. will generally be zero. c. will generally be close to the theoretical Black-Scholes price of the option. d. will generally be close to the price of a futures contract with the same maturity. Clear my choice A binary option pays $100 if a stock price is greater than $30 in 18 months. The current stock price is $20, and its volatility is 30%. The risk-free rate is 2% and the expected return on the stock is 5%. What is the value of the option? a. $89.69 b. $10.56 c. $10.88 d. $56.12 Clear my choice Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Gender And Finance

Authors: Ylva Baeckström

1st Edition

103205557X, 978-1032055572