Please answer all questions:

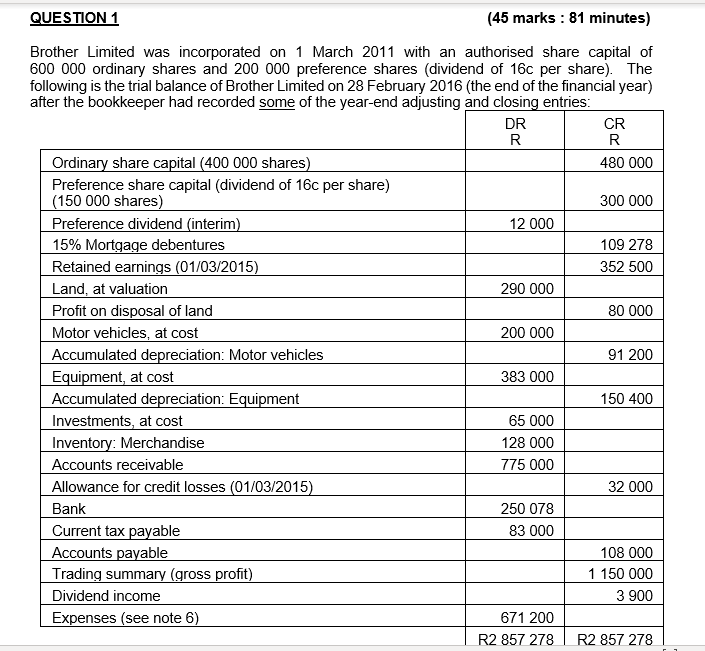

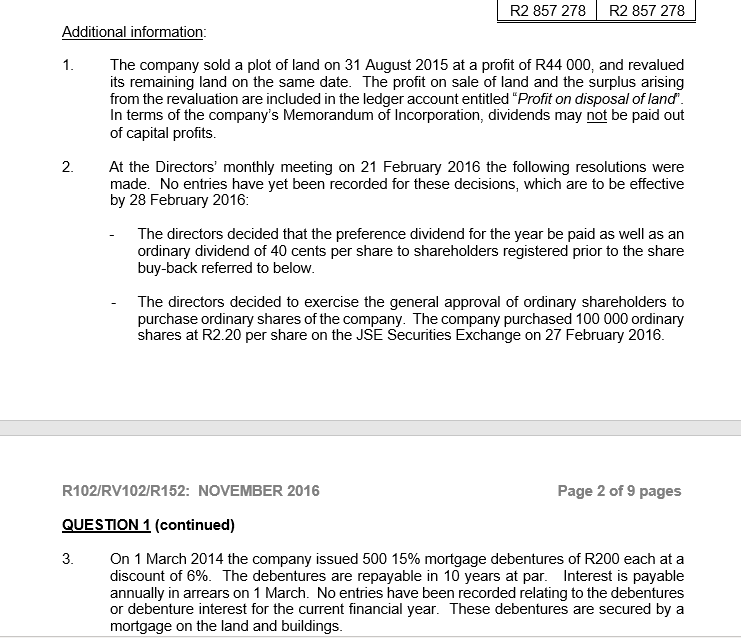

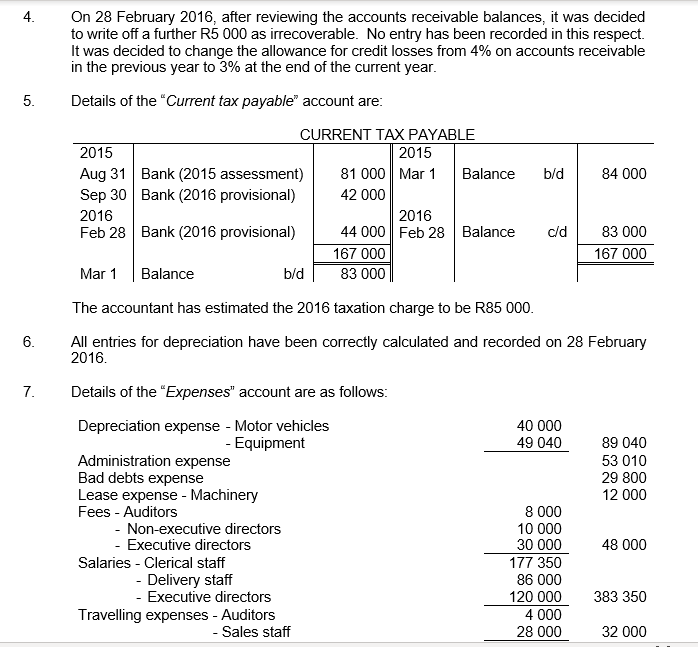

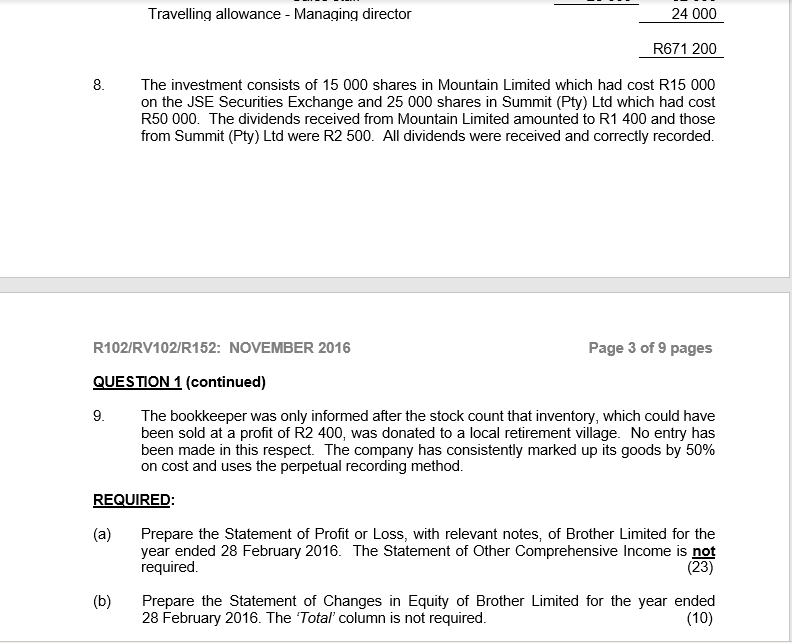

QUESTION 1 (45 marks : 81 minutes) Brother Limited was incorporated on 1 March 2011 with an authorised share capital of 600 000 ordinary shares and 200 000 preference shares (dividend of 16c per share). The following is the trial balance of Brother Limited on 28 February 2016 (the end of the financial year) after the bookkeeper had recorded some of the year-end adjusting and closing entries: DR CR R R Ordinary share capital (400 000 shares) 480 000 Preference share capital (dividend of 16c per share) (150 000 shares) 300 000 Preference dividend (interim) 12 000 15% Mortgage debentures 109 278 Retained earnings (01/03/2015) 352 500 Land, at valuation 290 000 Profit on disposal of land 80 000 Motor vehicles, at cost 200 000 Accumulated depreciation: Motor vehicles 91 200 Equipment, at cost 383 000 Accumulated depreciation: Equipment 150 400 Investments, at cost 65 000 Inventory: Merchandise 128 000 Accounts receivable 775 000 Allowance for credit losses (01/03/2015) 32 000 Bank 250 078 Current tax payable 83 000 Accounts payable 108 000 Trading summary (gross profit) 1 150 000 Dividend income 3 900 Expenses (see note 6) 671 200 R2 857 278 R2 857 278 R2 857 278 R2 857 278 Additional information: 1. The company sold a plot of land on 31 August 2015 at a profit of R44 000, and revalued its remaining land on the same date. The profit on sale of land and the surplus arising from the revaluation are included in the ledger account entitled "Profit on disposal of land". In terms of the company's Memorandum of Incorporation, dividends may not be paid out of capital profits. 2. At the Directors' monthly meeting on 21 February 2016 the following resolutions were made. No entries have yet been recorded for these decisions, which are to be effective by 28 February 2016: The directors decided that the preference dividend for the year be paid as well as an ordinary dividend of 40 cents per share to shareholders registered prior to the share buy-back referred to below. The directors decided to exercise the general approval of ordinary shareholders to purchase ordinary shares of the company. The company purchased 100 000 ordinary shares at R2.20 per share on the JSE Securities Exchange on 27 February 2016. R102/RV102/R152: NOVEMBER 2016 Page 2 of 9 pages QUESTION 1 (continued) 3. On 1 March 2014 the company issued 500 15% mortgage debentures of R200 each at a discount of 6%. The debentures are repayable in 10 years at par. Interest is payable annually in arrears on 1 March. No entries have been recorded relating to the debentures or debenture interest for the current financial year. These debentures are secured by a mortgage on the land and buildings. On 28 February 2016, after reviewing the accounts receivable balances, it was decided to write of a further R5 000 as irrecoverable. No entry has been recorded in this respect. It was decided to change the allowance for credit losses from 4% on accounts receivable in the previous year to 3% at the end of the current year. Details of the "Current tax payable" account are: 6. 5. b/d 84 000 CURRENT TAX PAYABLE 2015 2015 Aug 31 Bank (2015 assessment) 81 000 Mar 1 Balance Sep 30 Bank (2016 provisional) 42 000 2016 2016 Feb 28 Bank (2016 provisional) 44 000 Feb 28 Balance 167 000 Mar 1 Balance b/d 83 000 cld 83 000 167 000 The accountant has estimated the 2016 taxation charge to be R85 000. All entries for depreciation have been correctly calculated and recorded on 28 February 2016. 6. 7. 40 000 49 040 89 040 53 010 29 800 12 000 Details of the "Expenses" account are as follows: Depreciation expense - Motor vehicles Equipment Administration expense Bad debts expense Lease expense - Machinery Fees - Auditors Non-executive directors - Executive directors Salaries - Clerical staff - Delivery staff - Executive directors Travelling expenses - Auditors - Sales staff 48 000 8 000 10 000 30 000 177 350 86 000 120 000 4 000 28 000 383 350 32 000 Travelling allowance - Managing director 24 000 R671 200 8. The investment consists of 15 000 shares in Mountain Limited which had cost R15 000 on the JSE Securities Exchange and 25 000 shares in Summit (Pty) Ltd which had cost R50 000. The dividends received from Mountain Limited amounted to R1 400 and those from Summit (Pty) Ltd were R2 500. All dividends were received and correctly recorded. R102/RV102/R152: NOVEMBER 2016 Page 3 of 9 pages QUESTION 1 (continued) 9. The bookkeeper was only informed after the stock count that inventory, which could have been sold at a profit of R2 400, was donated to a local retirement village. No entry has been made in this respect. The company has consistently marked up its goods by 50% on cost and uses the perpetual recording method. REQUIRED: (a) Prepare the Statement of Profit or Loss, with relevant notes, of Brother Limited for the year ended 28 February 2016. The Statement of Other Comprehensive Income is not required. (23) (b) Prepare the Statement of Changes in Equity of Brother Limited for the year ended 28 February 2016. The 'Total column is not required. (10) (c) Prepare the 'Equity and Liabilities' section of the Statement of Financial Position of Brother Limited at 28 February 2016. (5) (d) Prepare only the 'Non-current liabilities' note to the Statement of Financial Position of Brother Limited at 28 February 2016. (7) The financial statements should be drafted in accordance with the information required in terms of International Financial Reporting Standards, insofar as the necessary detail is provided above. A worksheet is provided on page 9. Use of the worksheet is optional but should it be used it must be submitted as part of your workings. Note: Show all workings clearly. Work to the nearest R1. Work debenture interest rate to the nearest 4 decimal places. QUESTION 1 (45 marks : 81 minutes) Brother Limited was incorporated on 1 March 2011 with an authorised share capital of 600 000 ordinary shares and 200 000 preference shares (dividend of 16c per share). The following is the trial balance of Brother Limited on 28 February 2016 (the end of the financial year) after the bookkeeper had recorded some of the year-end adjusting and closing entries: DR CR R R Ordinary share capital (400 000 shares) 480 000 Preference share capital (dividend of 16c per share) (150 000 shares) 300 000 Preference dividend (interim) 12 000 15% Mortgage debentures 109 278 Retained earnings (01/03/2015) 352 500 Land, at valuation 290 000 Profit on disposal of land 80 000 Motor vehicles, at cost 200 000 Accumulated depreciation: Motor vehicles 91 200 Equipment, at cost 383 000 Accumulated depreciation: Equipment 150 400 Investments, at cost 65 000 Inventory: Merchandise 128 000 Accounts receivable 775 000 Allowance for credit losses (01/03/2015) 32 000 Bank 250 078 Current tax payable 83 000 Accounts payable 108 000 Trading summary (gross profit) 1 150 000 Dividend income 3 900 Expenses (see note 6) 671 200 R2 857 278 R2 857 278 R2 857 278 R2 857 278 Additional information: 1. The company sold a plot of land on 31 August 2015 at a profit of R44 000, and revalued its remaining land on the same date. The profit on sale of land and the surplus arising from the revaluation are included in the ledger account entitled "Profit on disposal of land". In terms of the company's Memorandum of Incorporation, dividends may not be paid out of capital profits. 2. At the Directors' monthly meeting on 21 February 2016 the following resolutions were made. No entries have yet been recorded for these decisions, which are to be effective by 28 February 2016: The directors decided that the preference dividend for the year be paid as well as an ordinary dividend of 40 cents per share to shareholders registered prior to the share buy-back referred to below. The directors decided to exercise the general approval of ordinary shareholders to purchase ordinary shares of the company. The company purchased 100 000 ordinary shares at R2.20 per share on the JSE Securities Exchange on 27 February 2016. R102/RV102/R152: NOVEMBER 2016 Page 2 of 9 pages QUESTION 1 (continued) 3. On 1 March 2014 the company issued 500 15% mortgage debentures of R200 each at a discount of 6%. The debentures are repayable in 10 years at par. Interest is payable annually in arrears on 1 March. No entries have been recorded relating to the debentures or debenture interest for the current financial year. These debentures are secured by a mortgage on the land and buildings. On 28 February 2016, after reviewing the accounts receivable balances, it was decided to write of a further R5 000 as irrecoverable. No entry has been recorded in this respect. It was decided to change the allowance for credit losses from 4% on accounts receivable in the previous year to 3% at the end of the current year. Details of the "Current tax payable" account are: 6. 5. b/d 84 000 CURRENT TAX PAYABLE 2015 2015 Aug 31 Bank (2015 assessment) 81 000 Mar 1 Balance Sep 30 Bank (2016 provisional) 42 000 2016 2016 Feb 28 Bank (2016 provisional) 44 000 Feb 28 Balance 167 000 Mar 1 Balance b/d 83 000 cld 83 000 167 000 The accountant has estimated the 2016 taxation charge to be R85 000. All entries for depreciation have been correctly calculated and recorded on 28 February 2016. 6. 7. 40 000 49 040 89 040 53 010 29 800 12 000 Details of the "Expenses" account are as follows: Depreciation expense - Motor vehicles Equipment Administration expense Bad debts expense Lease expense - Machinery Fees - Auditors Non-executive directors - Executive directors Salaries - Clerical staff - Delivery staff - Executive directors Travelling expenses - Auditors - Sales staff 48 000 8 000 10 000 30 000 177 350 86 000 120 000 4 000 28 000 383 350 32 000 Travelling allowance - Managing director 24 000 R671 200 8. The investment consists of 15 000 shares in Mountain Limited which had cost R15 000 on the JSE Securities Exchange and 25 000 shares in Summit (Pty) Ltd which had cost R50 000. The dividends received from Mountain Limited amounted to R1 400 and those from Summit (Pty) Ltd were R2 500. All dividends were received and correctly recorded. R102/RV102/R152: NOVEMBER 2016 Page 3 of 9 pages QUESTION 1 (continued) 9. The bookkeeper was only informed after the stock count that inventory, which could have been sold at a profit of R2 400, was donated to a local retirement village. No entry has been made in this respect. The company has consistently marked up its goods by 50% on cost and uses the perpetual recording method. REQUIRED: (a) Prepare the Statement of Profit or Loss, with relevant notes, of Brother Limited for the year ended 28 February 2016. The Statement of Other Comprehensive Income is not required. (23) (b) Prepare the Statement of Changes in Equity of Brother Limited for the year ended 28 February 2016. The 'Total column is not required. (10) (c) Prepare the 'Equity and Liabilities' section of the Statement of Financial Position of Brother Limited at 28 February 2016. (5) (d) Prepare only the 'Non-current liabilities' note to the Statement of Financial Position of Brother Limited at 28 February 2016. (7) The financial statements should be drafted in accordance with the information required in terms of International Financial Reporting Standards, insofar as the necessary detail is provided above. A worksheet is provided on page 9. Use of the worksheet is optional but should it be used it must be submitted as part of your workings. Note: Show all workings clearly. Work to the nearest R1. Work debenture interest rate to the nearest 4 decimal places