Answered step by step

Verified Expert Solution

Question

1 Approved Answer

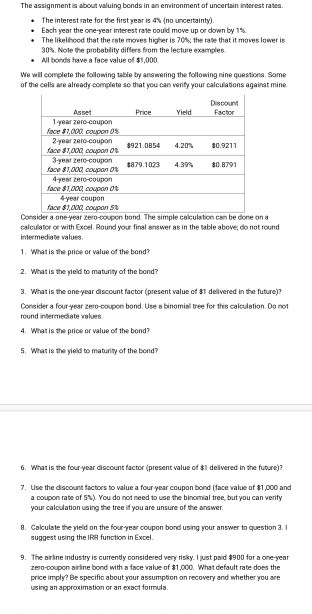

please answer all questions The assignment is about valuing bonds in an environment of uncertain interest rates. The interest rate for the first year is

please answer all questions

The assignment is about valuing bonds in an environment of uncertain interest rates. The interest rate for the first year is 4 (no uncertainty). Each year the one-year interest rate could move up or down by 1% The likelihood that the rate moves higher is 70% the rate that it moves lower is 30% Note the probability differs from the lecture examples All bonds have a face value of $1,000 We wil complete the following table by answering the following nine questions. Some of the calls are already complete so that you can verify your calculations against mine Discount Asset Price Yield Factor 1-year Zero-coupon face $1.000 euron 0% 2-year zero-coupon 8921.0854 4.2013 30.9211 face $100 con 08 3-year Zero-coupon $879. 1023 4.39% $0.8791 face $1.000 coupon 4-year Zero-coupon face $1,80 coupon 4-year coupon face $1,0 con 58 Consider a one-year Zero-coupon bond. The simple calculation can be done on a calculator or with ExcelRound your finalaswer as in the table above, do not round intermediate values 1. What is the price or value of the bond? 2. What is the yield to maturity of the bond? 3. What is the one year discount factor (present value of $1 delivered in the future)? Consider a four year Zero-coupon bond Use a binomial tree for this calculation. Do not round intermediate values 4. What is the price or value of the bond? 5. What is the yield to maturity of the bond? 6. What is the four year discount factor (present value of $1 delivered in the future)? 7. Use the discount factors to value a four year coupon bond (ace value of 31.000 and a coupon rate of 5). You do not need to use the binomial tree, but you can verify your calculation using the tree if you are unsure of the answer 8. Calculate the yield on the four year coupon bond using your answer to question 3.1 suggest using their function in Excel. 9. The arine industry is currently considered very risky. I just paid $900 for a one-year zero-coupon arine bond with a face value of $1,000. What default rate does the price imply? Be specific about your assumption on recovery and whether you are using an approximation or an exact formula The assignment is about valuing bonds in an environment of uncertain interest rates. The interest rate for the first year is 4 (no uncertainty). Each year the one-year interest rate could move up or down by 1% The likelihood that the rate moves higher is 70% the rate that it moves lower is 30% Note the probability differs from the lecture examples All bonds have a face value of $1,000 We wil complete the following table by answering the following nine questions. Some of the calls are already complete so that you can verify your calculations against mine Discount Asset Price Yield Factor 1-year Zero-coupon face $1.000 euron 0% 2-year zero-coupon 8921.0854 4.2013 30.9211 face $100 con 08 3-year Zero-coupon $879. 1023 4.39% $0.8791 face $1.000 coupon 4-year Zero-coupon face $1,80 coupon 4-year coupon face $1,0 con 58 Consider a one-year Zero-coupon bond. The simple calculation can be done on a calculator or with ExcelRound your finalaswer as in the table above, do not round intermediate values 1. What is the price or value of the bond? 2. What is the yield to maturity of the bond? 3. What is the one year discount factor (present value of $1 delivered in the future)? Consider a four year Zero-coupon bond Use a binomial tree for this calculation. Do not round intermediate values 4. What is the price or value of the bond? 5. What is the yield to maturity of the bond? 6. What is the four year discount factor (present value of $1 delivered in the future)? 7. Use the discount factors to value a four year coupon bond (ace value of 31.000 and a coupon rate of 5). You do not need to use the binomial tree, but you can verify your calculation using the tree if you are unsure of the answer 8. Calculate the yield on the four year coupon bond using your answer to question 3.1 suggest using their function in Excel. 9. The arine industry is currently considered very risky. I just paid $900 for a one-year zero-coupon arine bond with a face value of $1,000. What default rate does the price imply? Be specific about your assumption on recovery and whether you are using an approximation or an exact formulaStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Principles Of Macroeconomics

Authors: Frank, Bernanke, Antonovics, Heffetz

3rd Edition

1259117162, 9781259117169