Answered step by step

Verified Expert Solution

Question

1 Approved Answer

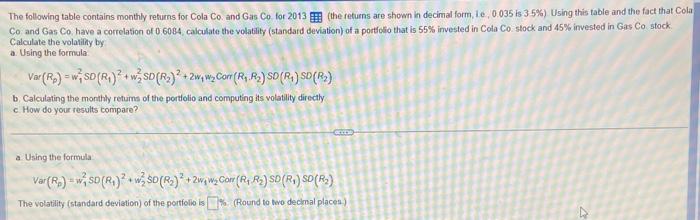

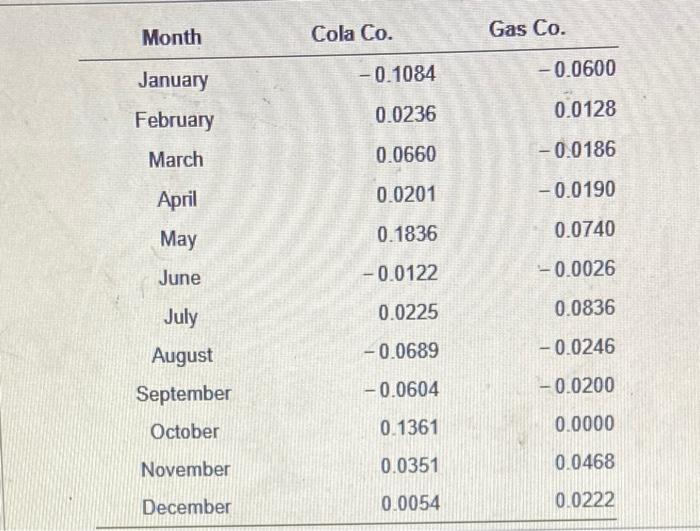

please answer all steps thank you! The following table contains monthly returns for Cola Co. and Gas Co for 2013 (the returns are shown in

please answer all steps thank you!

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Trade And Development Report 2020 From Global Pandemic To Prosperity For All Avoiding Another Lost Decade

Authors: United Nations Publications

1st Edition

9211129923,9210052692