Please answer all, thank you!

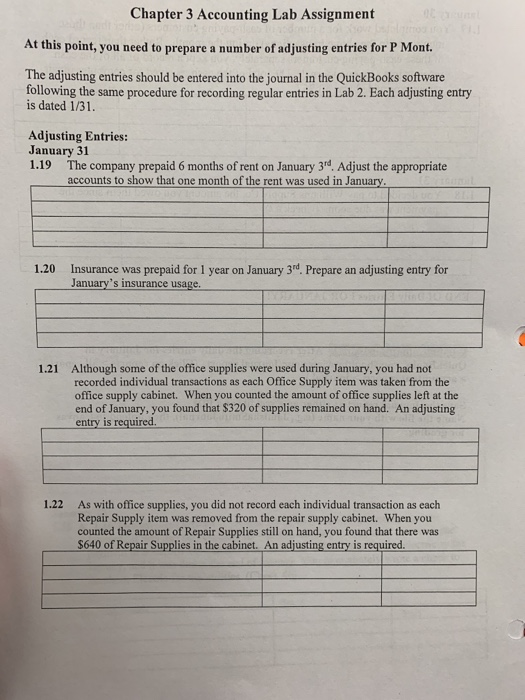

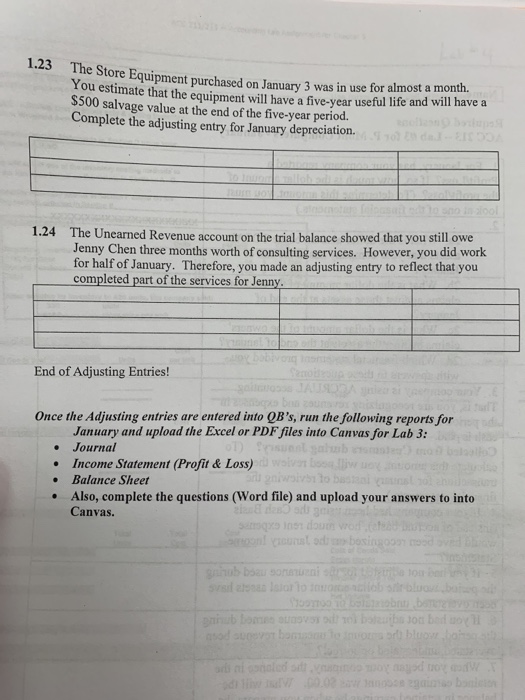

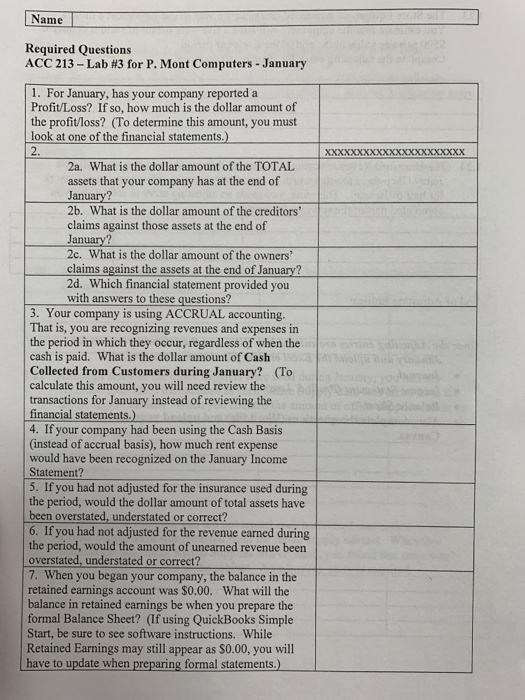

Chapter 3 Accounting Lab Assignment At this point, you need to prepare a number of adjusting entries for P Mont The adjusting entries should be entered into the journal in the QuickBooks software following the same procedure for recording regular entries in Lab 2. Each adjusting entry is dated 1/31 Adjusting Entries: January 31 1.19 The company prepaid 6 months of rent on January 3rd. Adjust the appropriate accounts to show that one month of the rent was used in January. prepaid for 1 year on January 3rd. Prepare an adjusting entry for 1.20 Insurance was January's insurance usage. Although some of the office supplies were used during January, you had not recorded individual transactions as each Office Supply item was taken from the office supply cabinet. When you counted the amount of office supplies left at the end of January, you found that $320 of supplies remained on hand. An adjusting entry is required. 1.21 1.22 As with office supplies, you did not record each individual transaction as each Repair Supply item was removed from the repair supply cabinet. When you counted the amount of Repair Supplies still on hand, you found that there was $640 of Repair Supplies in the cabinet. An adjusting entry is required. 1.23 The Store Equipment purchased on January 3 was in use for almost a montn. You estimate that the equipment will have a five-year useful life and will have a $500 salvage value at the end of the five-year period. Complete the adjusting entry for January depreciation. bedups to tgom 1.24 The Unearned Revenue account on the trial balance showed that you still owe Jenny Chen three months worth of consulting services. However, you did work for half of January. Therefore, you made an adjusting entry to reflect that you completed part of the services for Jenny. bvong End of Adjusting Entries! o ba zau run the following reports for Once the Adjusting entries are entered into QB's, January and upload the Excel or PDF files into Canvas for Lab 3: Journal Income Statement (Profit & Loss) Balance Sheet Also, complete the questions (Word file) and upload your answers to into zianl desO sdi goie 9qs In dou n unt od bosingoo Canvas. gahub bsau sonanueni Yd a laarlo ouo 10 rblua STOo obru bene prnub Lomes suaovso e bateih Jon bed o bamsorn o invors o bluo o asod ourev w gaino bneo Name Required Questions ACC 213 Lab #3 for P. Mont Computers - January 1. For January, has your company reported Profit/Loss? If so, how much is the dollar amount of the profit/loss? (To determine this amount, you must look at one of the financial statements.) 2. 2a. What is the dollar amount of the TOTAL assets that your company has at the end of January? 2b. What is the dollar amount of the creditors claims against those assets at the end of January? 2c. What is the dollar amount of the owners' claims against the assets at the end of January? 2d. Which financial statement provided you with answers to these questions? 3. Your company is using ACCRUAL accounting. That is, you are recognizing revenues and expenses in the period in which they occur, regardless of when the cash is paid. What is the dollar amount of Cash Collected from Customers during January? (To calculate this amount, you will need review the transactions for January instead of reviewing the financial statements.) 4. If your company had been using the Cash Basis (instead of accrual basis), how much rent expense would have been recognized on the January Income Statement? olbn wk Jary 5. If you had not adjusted for the insurance used during the period, would the dollar amount of total assets have been overstated, understated or correct? 6. If you had not adjusted for the revenue earned during the period, would the amount of unearned revenue been overstated, understated or correct? 7. When you began your company, the balance in the retained earnings account was $0.00. What will the balance in retained earnings be when you prepare the formal Balance Sheet? (If using QuickBooks Simple Start, be sure to see software instructions. While Retained Earnings may still appear as $0.00, you will have to update when preparing formal statements.) Chapter 3 Accounting Lab Assignment At this point, you need to prepare a number of adjusting entries for P Mont The adjusting entries should be entered into the journal in the QuickBooks software following the same procedure for recording regular entries in Lab 2. Each adjusting entry is dated 1/31 Adjusting Entries: January 31 1.19 The company prepaid 6 months of rent on January 3rd. Adjust the appropriate accounts to show that one month of the rent was used in January. prepaid for 1 year on January 3rd. Prepare an adjusting entry for 1.20 Insurance was January's insurance usage. Although some of the office supplies were used during January, you had not recorded individual transactions as each Office Supply item was taken from the office supply cabinet. When you counted the amount of office supplies left at the end of January, you found that $320 of supplies remained on hand. An adjusting entry is required. 1.21 1.22 As with office supplies, you did not record each individual transaction as each Repair Supply item was removed from the repair supply cabinet. When you counted the amount of Repair Supplies still on hand, you found that there was $640 of Repair Supplies in the cabinet. An adjusting entry is required. 1.23 The Store Equipment purchased on January 3 was in use for almost a montn. You estimate that the equipment will have a five-year useful life and will have a $500 salvage value at the end of the five-year period. Complete the adjusting entry for January depreciation. bedups to tgom 1.24 The Unearned Revenue account on the trial balance showed that you still owe Jenny Chen three months worth of consulting services. However, you did work for half of January. Therefore, you made an adjusting entry to reflect that you completed part of the services for Jenny. bvong End of Adjusting Entries! o ba zau run the following reports for Once the Adjusting entries are entered into QB's, January and upload the Excel or PDF files into Canvas for Lab 3: Journal Income Statement (Profit & Loss) Balance Sheet Also, complete the questions (Word file) and upload your answers to into zianl desO sdi goie 9qs In dou n unt od bosingoo Canvas. gahub bsau sonanueni Yd a laarlo ouo 10 rblua STOo obru bene prnub Lomes suaovso e bateih Jon bed o bamsorn o invors o bluo o asod ourev w gaino bneo Name Required Questions ACC 213 Lab #3 for P. Mont Computers - January 1. For January, has your company reported Profit/Loss? If so, how much is the dollar amount of the profit/loss? (To determine this amount, you must look at one of the financial statements.) 2. 2a. What is the dollar amount of the TOTAL assets that your company has at the end of January? 2b. What is the dollar amount of the creditors claims against those assets at the end of January? 2c. What is the dollar amount of the owners' claims against the assets at the end of January? 2d. Which financial statement provided you with answers to these questions? 3. Your company is using ACCRUAL accounting. That is, you are recognizing revenues and expenses in the period in which they occur, regardless of when the cash is paid. What is the dollar amount of Cash Collected from Customers during January? (To calculate this amount, you will need review the transactions for January instead of reviewing the financial statements.) 4. If your company had been using the Cash Basis (instead of accrual basis), how much rent expense would have been recognized on the January Income Statement? olbn wk Jary 5. If you had not adjusted for the insurance used during the period, would the dollar amount of total assets have been overstated, understated or correct? 6. If you had not adjusted for the revenue earned during the period, would the amount of unearned revenue been overstated, understated or correct? 7. When you began your company, the balance in the retained earnings account was $0.00. What will the balance in retained earnings be when you prepare the formal Balance Sheet? (If using QuickBooks Simple Start, be sure to see software instructions. While Retained Earnings may still appear as $0.00, you will have to update when preparing formal statements.)