Answered step by step

Verified Expert Solution

Question

1 Approved Answer

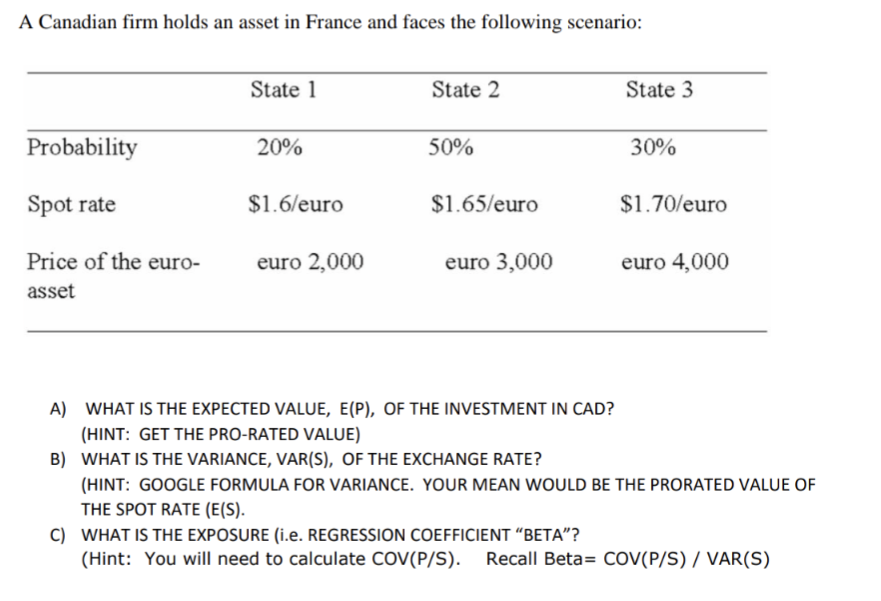

please answer all three points (a,b and c). A Canadian firm holds an asset in France and faces the following scenario: State 1 State 2

please answer all three points (a,b and c).

A Canadian firm holds an asset in France and faces the following scenario: State 1 State 2 State 3 Probability 20% 50% 30% Spot rate $1.6/euro $1.65/euro $1.70/euro euro 2,000 euro 3,000 Price of the euro- asset euro 4,000 A) WHAT IS THE EXPECTED VALUE, E(P), OF THE INVESTMENT IN CAD? (HINT: GET THE PRO-RATED VALUE) B) WHAT IS THE VARIANCE, VAR(S), OF THE EXCHANGE RATE? (HINT: GOOGLE FORMULA FOR VARIANCE. YOUR MEAN WOULD BE THE PRORATED VALUE OF THE SPOT RATE (E(S). C) WHAT IS THE EXPOSURE (i.e. REGRESSION COEFFICIENT BETA"? (Hint: You will need to calculate COV(P/S). Recall Beta= COV(P/S) / VAR(S)Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Markets And Corporate Strategy

Authors: David Hillier , Mark Grinblatt , Sheridan Titman

2nd Edition

0077129423,0077141350