Answered step by step

Verified Expert Solution

Question

1 Approved Answer

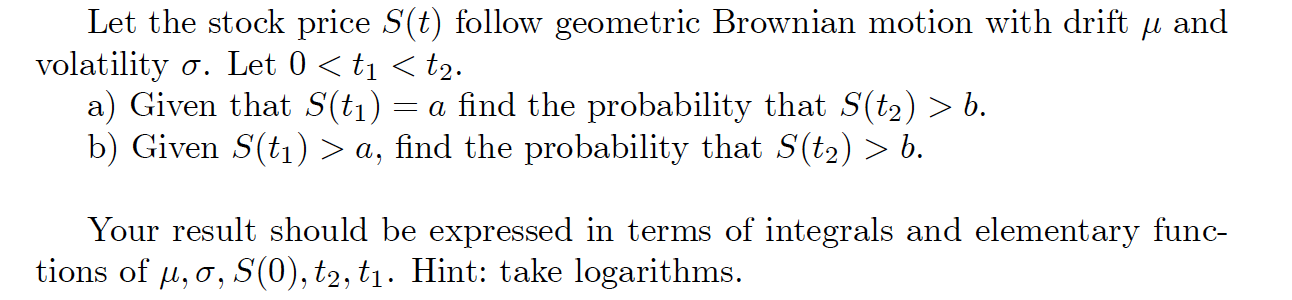

Please answer both parts, i'll give good rating Let the stock price S(t) follow geometric Brownian motion with drift u and volatility o. Let 0

Please answer both parts, i'll give good rating

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Discrete Mathematics Mathematical Reasoning And Proof With Puzzles, Patterns, And Games

Authors: Douglas E Ensley, J Winston Crawley

1st Edition

1118226534, 9781118226537