please answer both questions, thank you

This is the format presented in the chaper, thank you

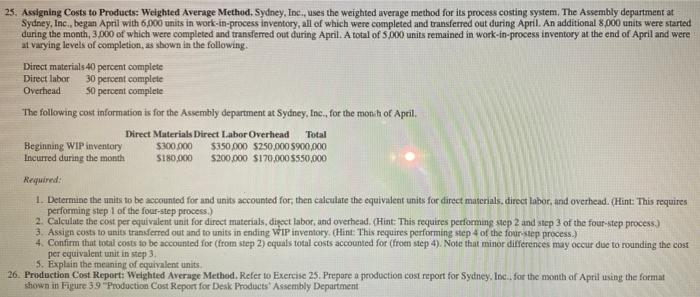

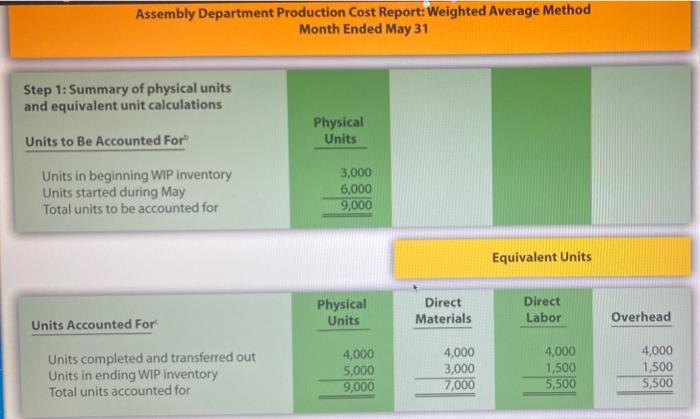

23. Assigning Costs to Products: Weighted Average Method. Sydney, Inc., uses the weighted average method for its process costing system. The Assembly department at Sydney, Inc., began April with 6,000 units in work-in-process inventory, all of which were completed and transferred out during April. An additional 8,000 units were started during the month, 3000 of which were completed and transferred out during April. A total of 5000 units remained in work-in-process inventory at the end of April and were at varying levels of completion, as shown in the following. Direct materials 40 percent complete Direct labor 30 percent complete Overhead 50 percent complete The following cost information is for the Assembly department at Sydney, Inc., for the monch of April, Direct Materials Direct Labor Overhead Total Beginning WIP inventory $300.000 $350,000 $250,000 $1,000 Incurred during the month S180.000 $200,000 $170,000 $550,000 Required: 1. Determine the units to be accounted for and units accounted for, then calculate the equivalent units for direct materials, direct labor, and overhead. (Hint: This requires performing step 1 of the four-step process.) 2. Calculate the cost per equivalent unit for direct materials, direct labor, and overhead. (Hint: This requires performing step 2 and step 3 of the four-step process.) 3. Assign costs to units transferred out and to units in ending WIP inventory. (Hint: This requires performing step 4 of the four-step process.) 4. Confirm that total costs to be accounted for (from step 2) equals total costs accounted for (from step 4). Note that minor differences may occur due to rounding the cost per equivalent unit in step 3. 5. Explain the meaning of equivalent units 26. Production Cost Report: Weighted Average Method. Refer to Exercise 25. Prepare a production cost report for Sydney, Inc., for the month of April using the format shown in Figure 39 Production Cost Report for Desk Products' Assembly Department Assembly Department Production Cost Report: Weighted Average Method Month Ended May 31 Step 1: Summary of physical units and equivalent unit calculations Physical Units Units to Be Accounted For Units in beginning WIP inventory Units started during May Total units to be accounted for 3,000 6,000 9,000 Equivalent Units Physical Units Direct Materials Direct Labor Overhead Units Accounted For Units completed and transferred out Units in ending WIP inventory Total units accounted for 4,000 5,000 9,000 4,000 3,000 7,000 4,000 1,500 5,500 4,000 1,500 5,500 Step 2: Summary of costs to be accounted for Costs to Be Accounted For Direct Materials Direct Labor Overhead Total Costs in beginning WIP inventory Costs incurred during May Total costs to be accounted for $ 95,000 115,000 $ 210,000 $ 40,000 70,000 $ 110,000 $ 26,000 40,000 $ 66,000 $ 161,000 225,000 $ 386,000 Step 3: Calculation of cost per equivalent unit Direct Materials Direct Labor Overhead Total Total costs to be accounted for Total equivalent units accounted for Cost per equivalent unit $ 210,000 +7,000 $ 30 $ 110,000 +5,500 5 20 $ 66,000 +5,500 S 12 $ 62 Step 4: Assign costs to units transferred out and units in ending WIP inventory. Step 3: Calculation of cost per equivalent unit Direct Materials Direct Labor Overhead Total Total costs to be accounted for Total equivalent units accounted for Cost per equivalent unit $ 210,000 + 7,000 5 30 $ 110,000 +5,500 5 20 $ 66,000 +5,500 12 62 Step 4: Assign costs to units transferred out and units in ending WIP inventory. Direct Materials Direct Labor Overhead Total $ 120,000 90,000 Costs assigned to units transferred out Costs assigned to ending WIP inventory Total costs accounted for $ 80,000 30,000 $ 48,000 18,000 $ 248,000 138,000 $ 386,000