Please answer case #1

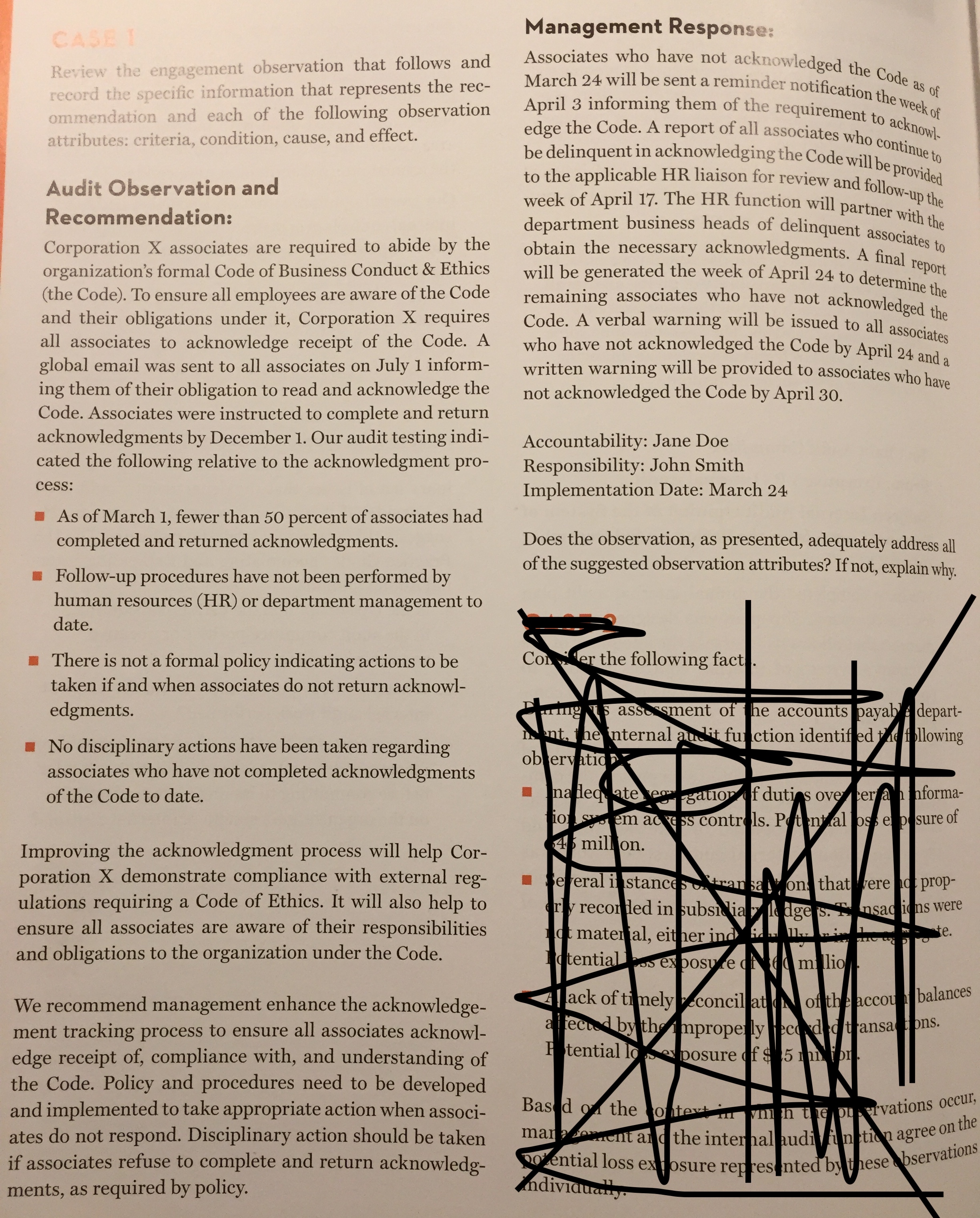

CASE I Management Response: Review the engagement observation that follows and record the specific information that represents the rec- Associates who have not acknowledged the Code as of ommendation and each of the following observation March 24 will be sent a reminder notification the week of April 3 informing them of the requirement to acknowl attributes: criteria, condition, cause, and effect. edge the Code. A report of all associates who continue to be delinquent in acknowledging the Code will be provided Audit Observation and to the applicable HR liaison for r ison for review and follow-up the Recommendation: week of April 17. The HR function will partner with the Corporation X associates are required to abide by the department business heads of delinquent associates to organization's formal Code of Business Conduct & Ethics obtain the necessary acknowledgments. A final report (the Code). To ensure all employees are aware of the Code will be generated the week of April 24 to determine the and their obligations under it, Corporation X requires remaining associates who have not acknowledged the all associates to acknowledge receipt of the Code. A Code. A verbal warning will be issued to all associates global email was sent to all associates on July 1 inform- who have not acknowledged the Code by April 24 and a ing them of their obligation to read and acknowledge the written warning will be provided to associates who have Code. Associates were instructed to complete and return not acknowledged the Code by April 30. acknowledgments by December 1. Our audit testing indi- Accountability: Jane Doe cated the following relative to the acknowledgment pro- Responsibility: John Smith cess: Implementation Date: March 24 As of March 1, fewer than 50 percent of associates had completed and returned acknowledgments. Does the observation, as presented, adequately address all Follow-up procedures have not been performed by of the suggested observation attributes? If not, explain why. human resources (HR) or department management to date. There is not a formal policy indicating actions to be Col der the following fact taken if and when associates do not return acknowl edgments. s assessment of the accounts payable depart- No disciplinary actions have been taken regarding ent, he internal audit function identified following associates who have not completed acknowledgments blervation of the Code to date. madeq. te ec gation f duties over per a Informa- em access controls. Potential loss exposure of Improving the acknowledgment process will help Cor- 4% mill on. poration X demonstrate compliance with external reg- eral instances tran said on that were not prop- ulations requiring a Code of Ethics. It will also help to Ins were ensure all associates are aware of their responsibilities recorded in subsidial ledgers. Mansaq t material, either ind te and obligations to the organization under the Code. Fos exposure millio We recommend management enhance the acknowledge- of the account balances ment tracking process to ensure all associates acknowl ons. edge receipt of, compliance with, and understanding of the Code. Policy and procedures need to be developed and implemented to take appropriate action when associ- ates do not respond. Disciplinary action should be taken if associates refuse to complete and return acknowledg- ments, as required by policy