Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Please answer completely thanks and correct :) The future value and present value equations also help in finding the interest rate and the number of

Please answer completely thanks and correct :)

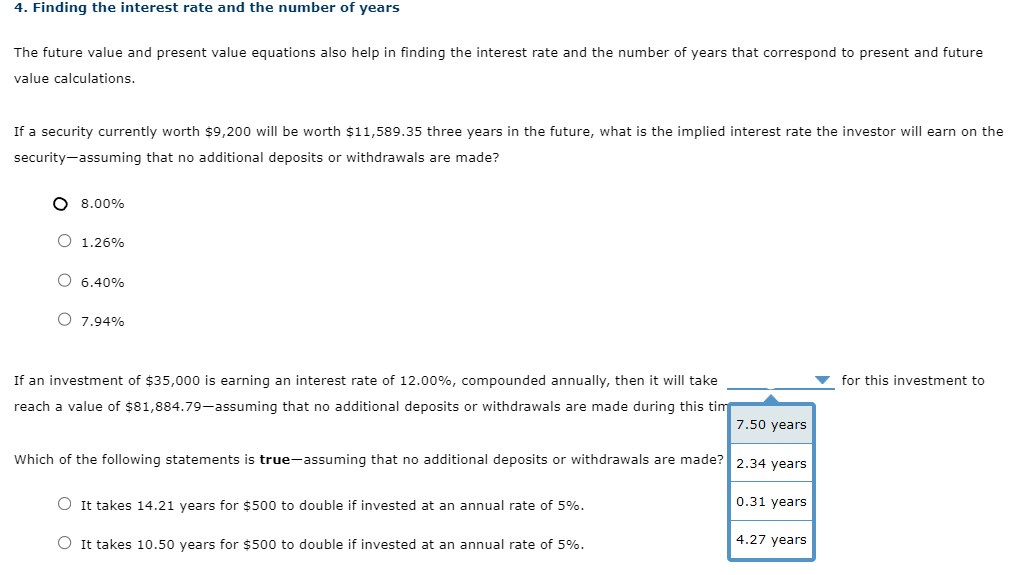

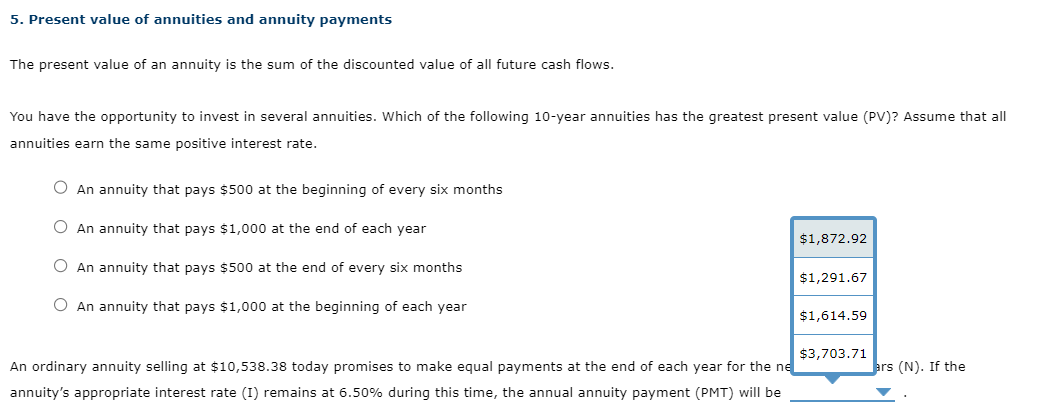

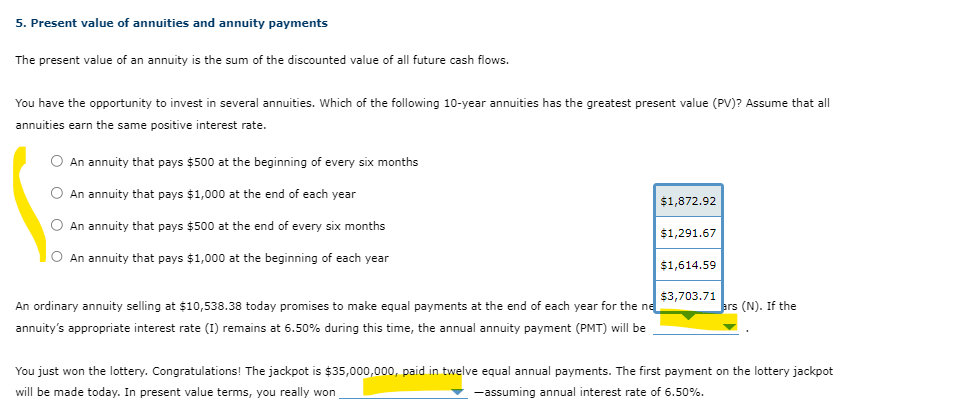

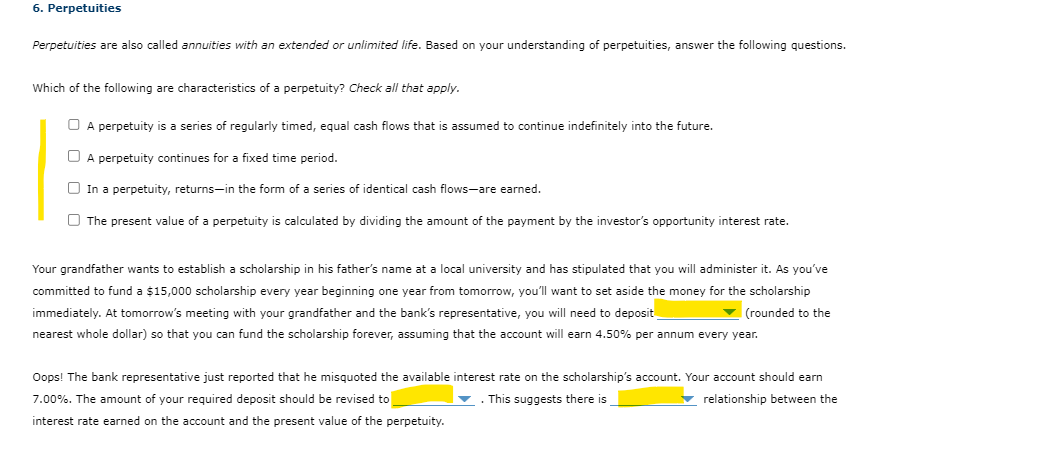

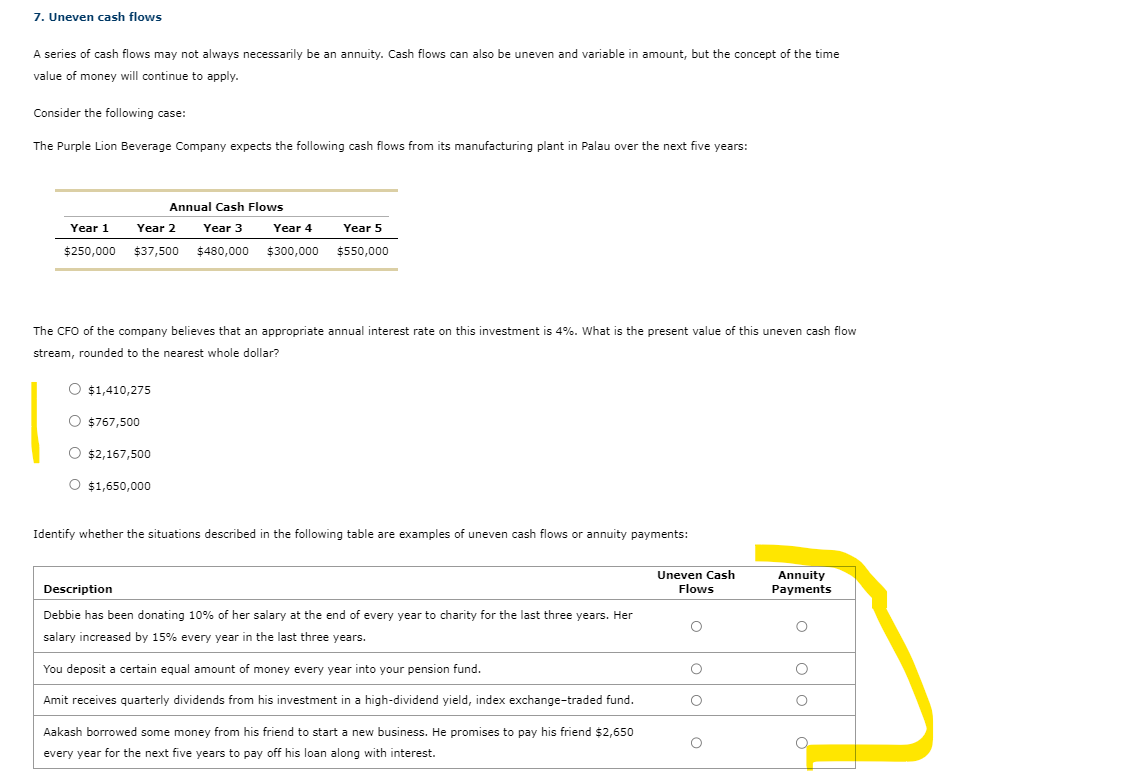

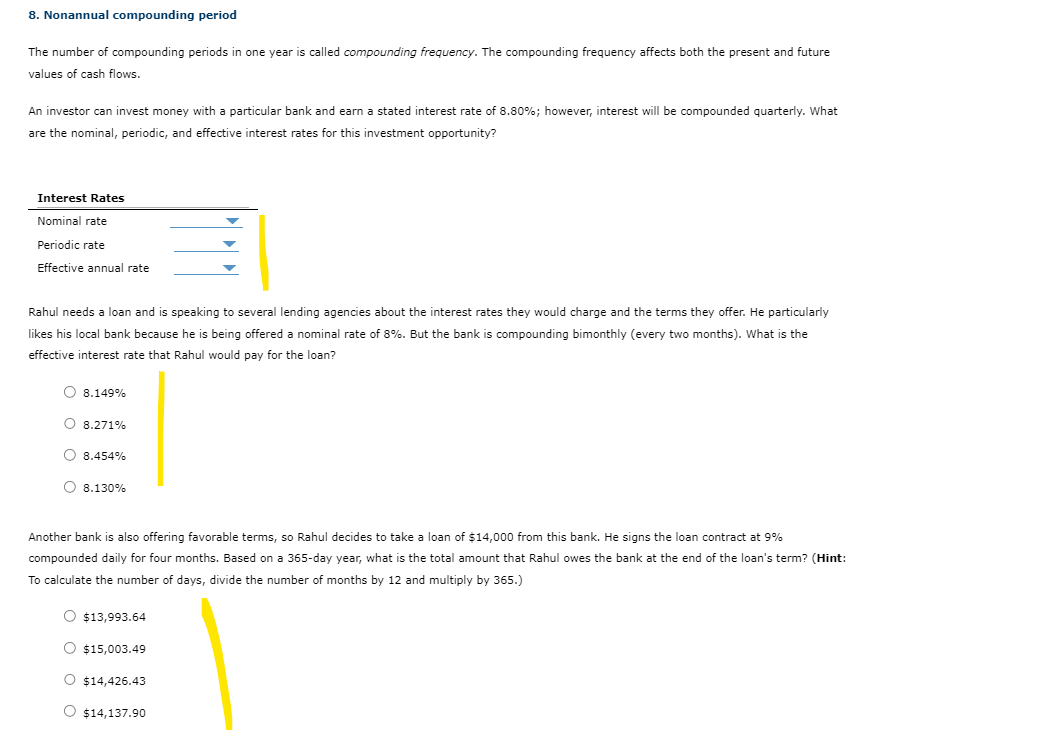

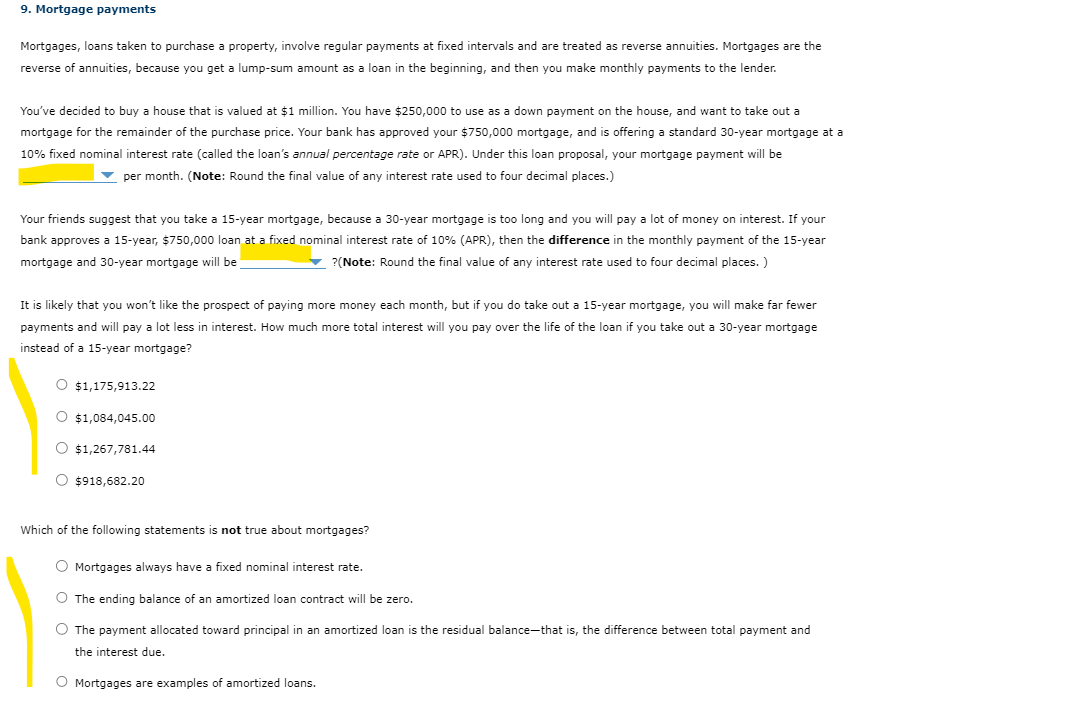

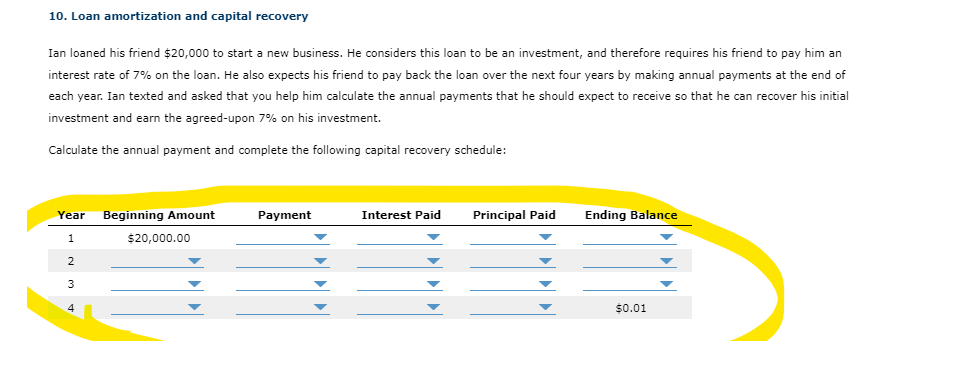

The future value and present value equations also help in finding the interest rate and the number of years that correspond to present and future value calculations. If a security currently worth $9,200 will be worth $11,589.35 three years in the future, what is the implied interest rate the investor will earn on the security-assuming that no additional deposits or withdrawals are made? 8.00% 1.26% 6.40% 7.94% If an investment of $35,000 is earning an interest rate of 12.00%, compounded annually, then it will take reach a value of $81,884.79-assuming that no additional deposits or withdrawals are made during this tin Which of the following statements is true-assuming that no additional deposits or withdrawals are made? for this investment to It takes 14.21 years for $500 to double if invested at an annual rate of 5%. It takes 10.50 years for $500 to double if invested at an annual rate of 5%. 5. Present value of annuities and annuity payments The present value of an annuity is the sum of the discounted value of all future cash flows. You have the opportunity to invest in several annuities. Which of the following 10-year annuities has the greatest present value (PV)? Assume that all annuities earn the same positive interest rate. An annuity that pays $500 at the beginning of every six months An annuity that pays $1,000 at the end of each year An annuity that pays $500 at the end of every six months An annuity that pays $1,000 at the beginning of each year An ordinary annuity selling at $10,538.38 today promises to make equal payments at the end of each year for the ne annuity's appropriate interest rate (I) remains at 6.50% during this time, the annual annuity payment (PMT) will be 5. Present value of annuities and annuity payments The present value of an annuity is the sum of the discounted value of all future cash flows. You have the opportunity to invest in several annuities. Which of the following 10-year annuities has the greatest present value (PV)? Assume that all annuities earn the same positive interest rate. An annuity that pays $500 at the beginning of every six months An annuity that pays $1,000 at the end of each year An annuity that pays $500 at the end of every six months An annuity that pays $1,000 at the beginning of each year An ordinary annuity selling at $10,538.38 today promises to make equal payments at the end of each year for the ne \begin{tabular}{|} $1,872.92 \\ $1,291.67 \\ $1,614.59 \\ $3,703.71 ars (N). If the \end{tabular} annuity's appropriate interest rate (I) remains at 6.50% during this time, the annual annuity payment (PMT) will be You just won the lottery. Congratulations! The jackpot is $35,0nn nnn nair in twalve equal annual payments. The first payment on the lottery jackpot will be made today. In present value terms, you really won -assuming annual interest rate of 6.50%. Perpetuities are also called annuities with an extended or unlimited life. Based on your understanding of perpetuities, answer the following questions. Which of the following are characteristics of a perpetuity? Check all that apply. A perpetuity is a series of regularly timed, equal cash flows that is assumed to continue indefinitely into the future. A perpetuity continues for a fixed time period. In a perpetuity, returns-in the form of a series of identical cash flows-are earned. The present value of a perpetuity is calculated by dividing the amount of the payment by the investor's opportunity interest rate. Your grandfather wants to establish a scholarship in his father's name at a local university and has stipulated that you will administer it. As you've committed to fund a $15,000 scholarship every year beginning one year from tomorrow, you'll want to set aside the money for the scholarship immediately. At tomorrow's meeting with your grandfather and the bank's representative, you will need to deposit (rounded to the nearest whole dollar) so that you can fund the scholarship forever, assuming that the account will earn 4.50% per annum every year. Oops! The bank representative just reported that he misquoted the available interest rate on the scholarship's account. Your account should earn 7.00%. The amount of your required deposit should be revised to . This suggests there is relationship between the interest rate earned on the account and the present value of the perpetuity. A series of cash flows may not always necessarily be an annuity. Cash flows can also be uneven and variable in amount, but the concept of the time value of money will continue to apply. Consider the following case: The Purple Lion Beverage Company expects the following cash flows from its manufacturing plant in Palau over the next five years: The CFO of the company believes that an appropriate annual interest rate on this investment is 4%. What is the present value of this uneven cash flow stream, rounded to the nearest whole dollar? $1,410,275$767,500$2,167,500$1,650,000 8. Nonannual compounding period The number of compounding periods in one year is called compounding frequency. The compounding frequency affects both the present and future values of cash flows. An investor can invest money with a particular bank and earn a stated interest rate of 8.80%; however, interest will be compounded quarterly. What are the nominal, periodic, and effective interest rates for this investment opportunity? Rahul needs a loan and is speaking to several lending agencies about the interest rates they would charge and the terms they offer. He particularly likes his local bank because he is being offered a nominal rate of 8%. But the bank is compounding bimonthly (every two months). What is the effective interest rate that Rahul would pay for the loan? 8.149% 8.271% 8.454% 8.130% Another bank is also offering favorable terms, so Rahul decides to take a loan of $14,000 from this bank. He signs the loan contract at 9% compounded daily for four months. Based on a 365-day year, what is the total amount that Rahul owes the bank at the end of the loan's term? (Hint: To calculate the number of days, divide the number of months by 12 and multiply by 365. ) $13,993.64$15,003.49$14,426.43$14,137.90 Mortgages, loans taken to purchase a property, involve regular payments at fixed intervals and are treated as reverse annuities. Mortgages are the reverse of annuities, because you get a lump-sum amount as a loan in the beginning, and then you make monthly payments to the lender. You've decided to buy a house that is valued at $1 million. You have $250,000 to use as a down payment on the house, and want to take out a mortgage for the remainder of the purchase price. Your bank has approved your $750,000 mortgage, and is offering a standard 30 -year mortgage at a 10% fixed nominal interest rate (called the loan's annual percentage rate or APR). Under this loan proposal, your mortgage payment will be per month. (Note: Round the final value of any interest rate used to four decimal places.) Your friends suggest that you take a 15 -year mortgage, because a 30 -year mortgage is too long and you will pay a lot of money on interest. If your bank approves a 15 -year, $750,000 loar st = fivat mnminal interest rate of 10% (APR), then the difference in the monthly payment of the 15 -year mortgage and 30 -year mortgage will be ?(Note: Round the final value of any interest rate used to four decimal places.) It is likely that you won't like the prospect of paying more money each month, but if you do take out a 15 -year mortgage, you will make far fewer payments and will pay a lot less in interest. How much more total interest will you pay over the life of the loan if you take out a 30 -year mortgage instead of a 15 -year mortgage? $1,175,913.22$1,084,045.00$1,267,781.44$918,682.20 Which of the following statements is not true about mortgages? Mortgages always have a fixed nominal interest rate. The ending balance of an amortized loan contract will be zero. The payment allocated toward principal in an amortized loan is the residual balance-that is, the difference between total payment and the interest due. Mortgages are examples of amortized loans. 10. Loan amortization and capital recovery Ian loaned his friend $20,000 to start a new business. He considers this loan to be an investment, and therefore requires his friend to pay him an interest rate of 7% on the loan. He also expects his friend to pay back the loan over the next four years by making annual payments at the end of each year. Ian texted and asked that you help him calculate the annual payments that he should expect to receive so that he can recover his initial investment and earn the agreed-upon 7% on his investment. Calculate the annual payment and complete the following capital recovery schedule: The future value and present value equations also help in finding the interest rate and the number of years that correspond to present and future value calculations. If a security currently worth $9,200 will be worth $11,589.35 three years in the future, what is the implied interest rate the investor will earn on the security-assuming that no additional deposits or withdrawals are made? 8.00% 1.26% 6.40% 7.94% If an investment of $35,000 is earning an interest rate of 12.00%, compounded annually, then it will take reach a value of $81,884.79-assuming that no additional deposits or withdrawals are made during this tin Which of the following statements is true-assuming that no additional deposits or withdrawals are made? for this investment to It takes 14.21 years for $500 to double if invested at an annual rate of 5%. It takes 10.50 years for $500 to double if invested at an annual rate of 5%. 5. Present value of annuities and annuity payments The present value of an annuity is the sum of the discounted value of all future cash flows. You have the opportunity to invest in several annuities. Which of the following 10-year annuities has the greatest present value (PV)? Assume that all annuities earn the same positive interest rate. An annuity that pays $500 at the beginning of every six months An annuity that pays $1,000 at the end of each year An annuity that pays $500 at the end of every six months An annuity that pays $1,000 at the beginning of each year An ordinary annuity selling at $10,538.38 today promises to make equal payments at the end of each year for the ne annuity's appropriate interest rate (I) remains at 6.50% during this time, the annual annuity payment (PMT) will be 5. Present value of annuities and annuity payments The present value of an annuity is the sum of the discounted value of all future cash flows. You have the opportunity to invest in several annuities. Which of the following 10-year annuities has the greatest present value (PV)? Assume that all annuities earn the same positive interest rate. An annuity that pays $500 at the beginning of every six months An annuity that pays $1,000 at the end of each year An annuity that pays $500 at the end of every six months An annuity that pays $1,000 at the beginning of each year An ordinary annuity selling at $10,538.38 today promises to make equal payments at the end of each year for the ne \begin{tabular}{|} $1,872.92 \\ $1,291.67 \\ $1,614.59 \\ $3,703.71 ars (N). If the \end{tabular} annuity's appropriate interest rate (I) remains at 6.50% during this time, the annual annuity payment (PMT) will be You just won the lottery. Congratulations! The jackpot is $35,0nn nnn nair in twalve equal annual payments. The first payment on the lottery jackpot will be made today. In present value terms, you really won -assuming annual interest rate of 6.50%. Perpetuities are also called annuities with an extended or unlimited life. Based on your understanding of perpetuities, answer the following questions. Which of the following are characteristics of a perpetuity? Check all that apply. A perpetuity is a series of regularly timed, equal cash flows that is assumed to continue indefinitely into the future. A perpetuity continues for a fixed time period. In a perpetuity, returns-in the form of a series of identical cash flows-are earned. The present value of a perpetuity is calculated by dividing the amount of the payment by the investor's opportunity interest rate. Your grandfather wants to establish a scholarship in his father's name at a local university and has stipulated that you will administer it. As you've committed to fund a $15,000 scholarship every year beginning one year from tomorrow, you'll want to set aside the money for the scholarship immediately. At tomorrow's meeting with your grandfather and the bank's representative, you will need to deposit (rounded to the nearest whole dollar) so that you can fund the scholarship forever, assuming that the account will earn 4.50% per annum every year. Oops! The bank representative just reported that he misquoted the available interest rate on the scholarship's account. Your account should earn 7.00%. The amount of your required deposit should be revised to . This suggests there is relationship between the interest rate earned on the account and the present value of the perpetuity. A series of cash flows may not always necessarily be an annuity. Cash flows can also be uneven and variable in amount, but the concept of the time value of money will continue to apply. Consider the following case: The Purple Lion Beverage Company expects the following cash flows from its manufacturing plant in Palau over the next five years: The CFO of the company believes that an appropriate annual interest rate on this investment is 4%. What is the present value of this uneven cash flow stream, rounded to the nearest whole dollar? $1,410,275$767,500$2,167,500$1,650,000 8. Nonannual compounding period The number of compounding periods in one year is called compounding frequency. The compounding frequency affects both the present and future values of cash flows. An investor can invest money with a particular bank and earn a stated interest rate of 8.80%; however, interest will be compounded quarterly. What are the nominal, periodic, and effective interest rates for this investment opportunity? Rahul needs a loan and is speaking to several lending agencies about the interest rates they would charge and the terms they offer. He particularly likes his local bank because he is being offered a nominal rate of 8%. But the bank is compounding bimonthly (every two months). What is the effective interest rate that Rahul would pay for the loan? 8.149% 8.271% 8.454% 8.130% Another bank is also offering favorable terms, so Rahul decides to take a loan of $14,000 from this bank. He signs the loan contract at 9% compounded daily for four months. Based on a 365-day year, what is the total amount that Rahul owes the bank at the end of the loan's term? (Hint: To calculate the number of days, divide the number of months by 12 and multiply by 365. ) $13,993.64$15,003.49$14,426.43$14,137.90 Mortgages, loans taken to purchase a property, involve regular payments at fixed intervals and are treated as reverse annuities. Mortgages are the reverse of annuities, because you get a lump-sum amount as a loan in the beginning, and then you make monthly payments to the lender. You've decided to buy a house that is valued at $1 million. You have $250,000 to use as a down payment on the house, and want to take out a mortgage for the remainder of the purchase price. Your bank has approved your $750,000 mortgage, and is offering a standard 30 -year mortgage at a 10% fixed nominal interest rate (called the loan's annual percentage rate or APR). Under this loan proposal, your mortgage payment will be per month. (Note: Round the final value of any interest rate used to four decimal places.) Your friends suggest that you take a 15 -year mortgage, because a 30 -year mortgage is too long and you will pay a lot of money on interest. If your bank approves a 15 -year, $750,000 loar st = fivat mnminal interest rate of 10% (APR), then the difference in the monthly payment of the 15 -year mortgage and 30 -year mortgage will be ?(Note: Round the final value of any interest rate used to four decimal places.) It is likely that you won't like the prospect of paying more money each month, but if you do take out a 15 -year mortgage, you will make far fewer payments and will pay a lot less in interest. How much more total interest will you pay over the life of the loan if you take out a 30 -year mortgage instead of a 15 -year mortgage? $1,175,913.22$1,084,045.00$1,267,781.44$918,682.20 Which of the following statements is not true about mortgages? Mortgages always have a fixed nominal interest rate. The ending balance of an amortized loan contract will be zero. The payment allocated toward principal in an amortized loan is the residual balance-that is, the difference between total payment and the interest due. Mortgages are examples of amortized loans. 10. Loan amortization and capital recovery Ian loaned his friend $20,000 to start a new business. He considers this loan to be an investment, and therefore requires his friend to pay him an interest rate of 7% on the loan. He also expects his friend to pay back the loan over the next four years by making annual payments at the end of each year. Ian texted and asked that you help him calculate the annual payments that he should expect to receive so that he can recover his initial investment and earn the agreed-upon 7% on his investment. Calculate the annual payment and complete the following capital recovery schedule

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Public Finance

Authors: H L Bhatia

30th Edition

9390080258, 978-9390080250