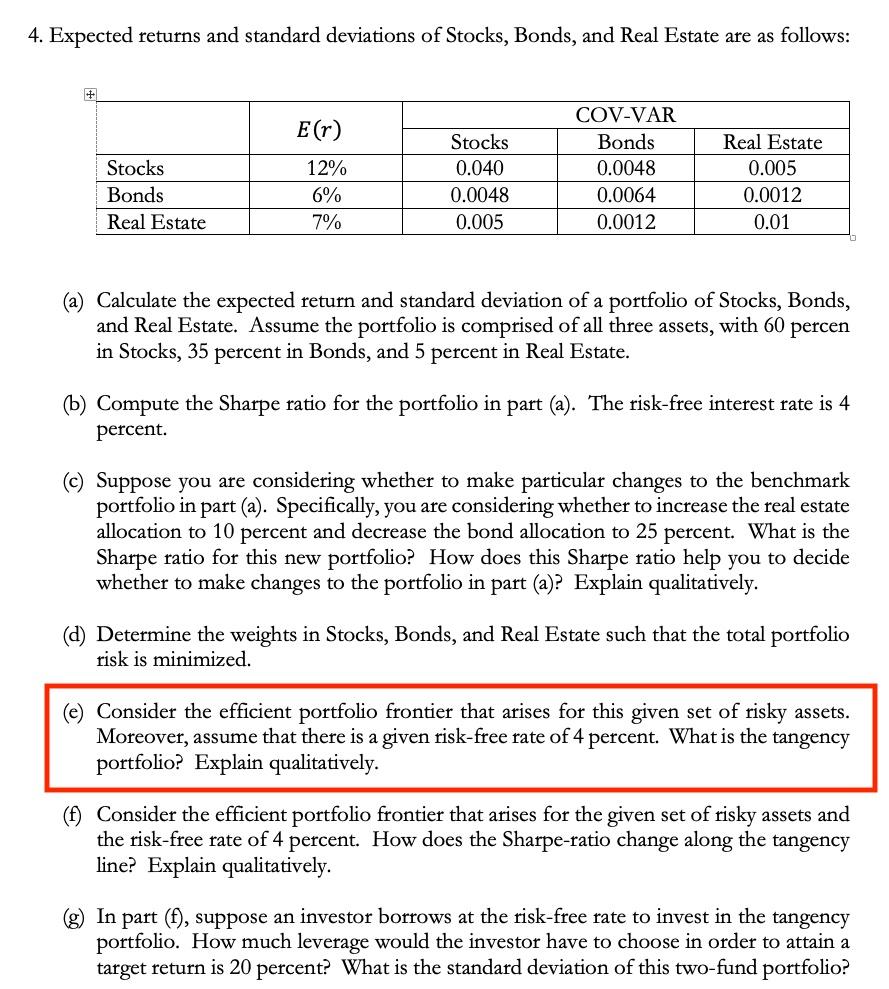

Question

Please answer E (outlined in Redbox / written directly below this sentence). (e) Consider the efficient portfolio frontier that arises for this given set of

Please answer E (outlined in Redbox / written directly below this sentence).

(e) Consider the efficient portfolio frontier that arises for this given set of risky assets. Moreover, assume that there is a given risk-free rate of 4 percent. What is the tangency portfolio? Explain qualitatively.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Lifestyle Investor

Authors: Justin Donald, Ryan Levesque, Mike Koenigs

1st Edition

1636800130, 978-1636800134