Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Please answer just 2 and 3 using ASC 810-10-15. Thank you Case 05-3 Cherry Banana Inc. (Banana) is a publicly traded company that manufactures fruity

Please answer just 2 and 3 using ASC 810-10-15. Thank you

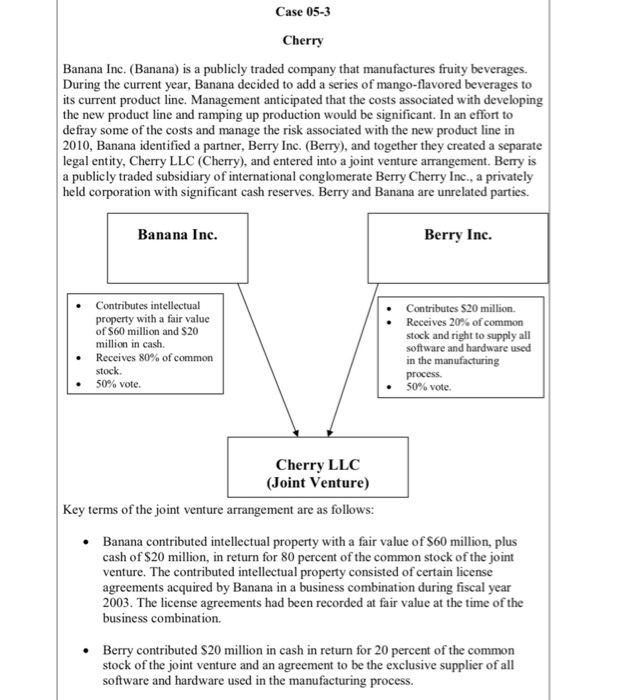

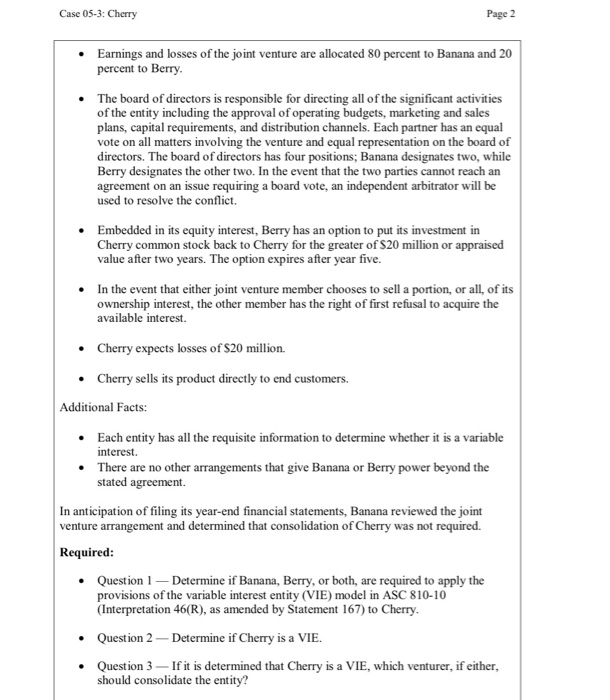

Case 05-3 Cherry Banana Inc. (Banana) is a publicly traded company that manufactures fruity beverages. During the current year, Banana decided to add a series of mango-flavored beverages to its current product line. Management anticipated that the costs associated with developing the new product line and ramping up production would be significant. In an effort to defray some of the costs and manage the risk associated with the new product line in 2010, Banana identified a partner, Berry Inc. (Berry), and together they created a separate legal entity, Cherry LLC (Cherry), and entered into a joint venture arrangement. Berry is a publicly traded subsidiary of international conglomerate Berry Cherry Inc., a privately held corporation with significant cash reserves. Berry and Banana are unrelated parties. Banana Inc. Berry Inc. Contributes intellectual property with a fair value of $60 million and $20 million in cash. Receives 80% of common stock. 50% vote. Contributes $20 million Receives 20% of common stock and right to supply all software and hardware used in the manufacturing process. 50% vote. Cherry LLC (Joint Venture) Key terms of the joint venture arrangement are as follows: Banana contributed intellectual property with a fair value of $60 million, plus cash of $20 million, in return for 80 percent of the common stock of the joint venture. The contributed intellectual property consisted of certain license agreements acquired by Banana in a business combination during fiscal year 2003. The license agreements had been recorded at fair value at the time of the business combination Berry contributed $20 million in cash in return for 20 percent of the common stock of the joint venture and an agreement to be the exclusive supplier of all software and hardware used in the manufacturing process. Case 05-3: Cherry Page 2 Earnings and losses of the joint venture are allocated 80 percent to Banana and 20 percent to Berry The board of directors is responsible for directing all of the significant activities of the entity including the approval of operating budgets, marketing and sales plans, capital requirements, and distribution channels. Each partner has an equal vote on all matters involving the venture and equal representation on the board of directors. The board of directors has four positions, Banana designates two, while Berry designates the other two. In the event that the two parties cannot reach an agreement on an issue requiring a board vote, an independent arbitrator will be used to resolve the conflict. Embedded in its equity interest, Berry has an option to put its investment in Cherry common stock back to Cherry for the greater of $20 million or appraised value after two years. The option expires after year five. In the event that either joint venture member chooses to sell a portion, or all of its ownership interest, the other member has the right of first refusal to acquire the available interest Cherry expects losses of $20 million. Cherry sells its product directly to end customers. Additional Facts: Each entity has all the requisite information to determine whether it is a variable interest There are no other arrangements that give Banana or Berry power beyond the stated agreement. In anticipation of filing its year-end financial statements, Banana reviewed the joint venture arrangement and determined that consolidation of Cherry was not required. Required: Question 1 Determine if Banana, Berry, or both, are required to apply the provisions of the variable interest entity (VIE) model in ASC 810-10 (Interpretation 46(R), as amended by Statement 167) to Cherry. Question 2 - Determine if Cherry is a VIE. Question 3 - If it is determined that Cherry is a VIE, which venturer, if either, should consolidate the entity? Case 05-3 Cherry Banana Inc. (Banana) is a publicly traded company that manufactures fruity beverages. During the current year, Banana decided to add a series of mango-flavored beverages to its current product line. Management anticipated that the costs associated with developing the new product line and ramping up production would be significant. In an effort to defray some of the costs and manage the risk associated with the new product line in 2010, Banana identified a partner, Berry Inc. (Berry), and together they created a separate legal entity, Cherry LLC (Cherry), and entered into a joint venture arrangement. Berry is a publicly traded subsidiary of international conglomerate Berry Cherry Inc., a privately held corporation with significant cash reserves. Berry and Banana are unrelated parties. Banana Inc. Berry Inc. Contributes intellectual property with a fair value of $60 million and $20 million in cash. Receives 80% of common stock. 50% vote. Contributes $20 million Receives 20% of common stock and right to supply all software and hardware used in the manufacturing process. 50% vote. Cherry LLC (Joint Venture) Key terms of the joint venture arrangement are as follows: Banana contributed intellectual property with a fair value of $60 million, plus cash of $20 million, in return for 80 percent of the common stock of the joint venture. The contributed intellectual property consisted of certain license agreements acquired by Banana in a business combination during fiscal year 2003. The license agreements had been recorded at fair value at the time of the business combination Berry contributed $20 million in cash in return for 20 percent of the common stock of the joint venture and an agreement to be the exclusive supplier of all software and hardware used in the manufacturing process. Case 05-3: Cherry Page 2 Earnings and losses of the joint venture are allocated 80 percent to Banana and 20 percent to Berry The board of directors is responsible for directing all of the significant activities of the entity including the approval of operating budgets, marketing and sales plans, capital requirements, and distribution channels. Each partner has an equal vote on all matters involving the venture and equal representation on the board of directors. The board of directors has four positions, Banana designates two, while Berry designates the other two. In the event that the two parties cannot reach an agreement on an issue requiring a board vote, an independent arbitrator will be used to resolve the conflict. Embedded in its equity interest, Berry has an option to put its investment in Cherry common stock back to Cherry for the greater of $20 million or appraised value after two years. The option expires after year five. In the event that either joint venture member chooses to sell a portion, or all of its ownership interest, the other member has the right of first refusal to acquire the available interest Cherry expects losses of $20 million. Cherry sells its product directly to end customers. Additional Facts: Each entity has all the requisite information to determine whether it is a variable interest There are no other arrangements that give Banana or Berry power beyond the stated agreement. In anticipation of filing its year-end financial statements, Banana reviewed the joint venture arrangement and determined that consolidation of Cherry was not required. Required: Question 1 Determine if Banana, Berry, or both, are required to apply the provisions of the variable interest entity (VIE) model in ASC 810-10 (Interpretation 46(R), as amended by Statement 167) to Cherry. Question 2 - Determine if Cherry is a VIE. Question 3 - If it is determined that Cherry is a VIE, which venturer, if either, should consolidate the entityStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Essential Knowledge For A First Year Audit Staff Intern In Big 4 Accounting

Authors: Kevin Hsu

1st Edition

1481097040, 978-1481097048