Answered step by step

Verified Expert Solution

Question

1 Approved Answer

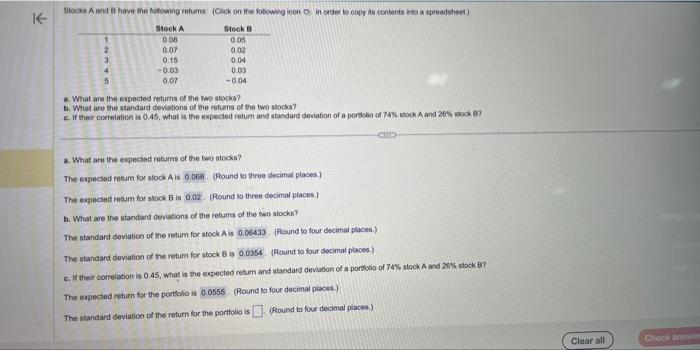

Please answer last part, make sure I can see the answer. Will only upvote if correct a. What are the expected returns of the fwo

Please answer last part, make sure I can see the answer.

a. What are the expected returns of the fwo stocka? b. What are the standard deviations of the ceburns of the two socks? c. If their correlation is 0.45, what is the expected return and atandard deviation of a porbilio of 74N mack A and 265 , asck B? a. What are the expected reburns of the two stocks? The expected retum for stock. A is (Found so theee dedimal places.) The expected resum for stock B is (Round to three decimai places.) b. What are the atandard deviations of the retums of the two stocks? The standard deviation of the return for stock A is (Found to four decimal places.) The standard deviation of the return for atock 8 is (Round to four decimal places.) c. if their comelation is 0.45, what is the expected rehum and atandard deviafion of a portolio of 74% stock A and 26% stock B? The expected return for the portlolio is (Round to four decimal plabes) The standard deviation of the return for the portfoio is (Round to four decinial places.) Will only upvote if correct

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Quantitative Corporate Finance

Authors: John B. Guerard Jr. Anureet Saxena, Mustafa Gultekin

2nd Edition

3030435466, 978-3030435462