Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Please answer numbers 1-10 on page 91. CASE 1 5 DEERPARK CASH BUDGETING My instincts tell me that we could have cash flow problems sometime

Please answer numbers 1-10 on page 91.

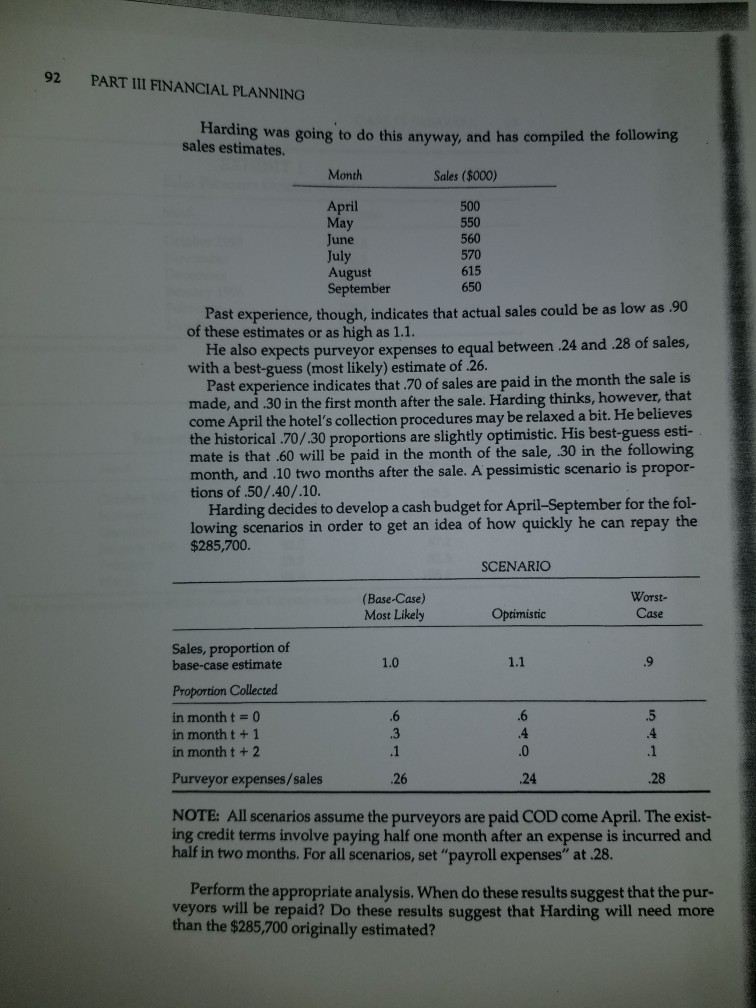

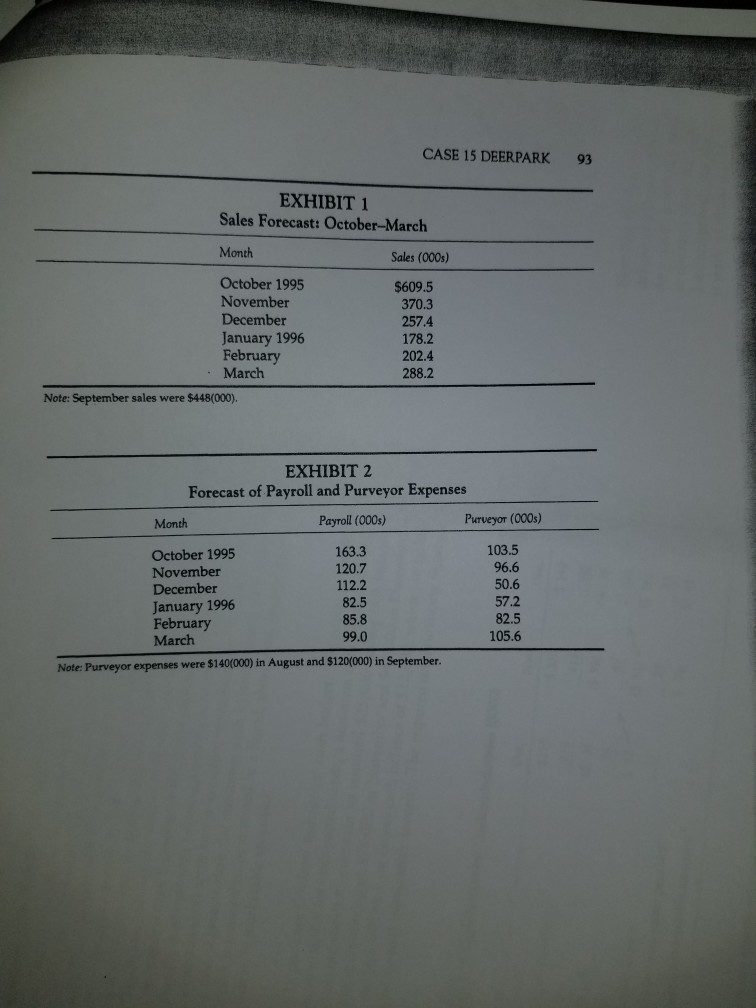

CASE 1 5 DEERPARK CASH BUDGETING "My instincts tell me that we could have cash flow problems sometime in the next six months, Patrick Harding the manager of Deerpark, a West Virginia re- sort, says to Lambert Purcell, the assistant manager. "I need to know now what we're dealing with and I think I'd better redo the cast." CASH FLOW CONCERNS fall. This is Three factors con Three months ago Harding had prepared a cash flow forecast for the period October 1995 to May 1996. November through March is generally a slow period for the resort, and it is not unusual for the lodge to run cash deficits during most, if not all of these months. However, the cash surplus generated during the peak period, from August through October, is typically sufficient to meet the short- precisely what Harding had predicted would occur when he had made the cash budget projection in July. But now, in early October, he is having second thoughts about the forecast concern Harding. First, the renovations planned for January need to be more extensive than originally thought. Harding had estimated the cost to be $420,000, but it appears $500,000 of work is necessary. Second, the re- sort's long-time sales manager left unexpectedly in August and her replacement cession has hit much of the area and Deerpark's sales are definitely sensitive the state of the regional economy All this suggests Harding's sales forecasts, which he had labeled "conservative" in July, are too high. "I can see indications of this now," he tells Purcell. "Revenue is off 10 percent for September and October, and our advance bookings for the rest of the year are also down. I'm sure we won't hit the levels we predicted." Harding has always been an advo- cate of cash budget forecasts and constantly revises an estimate in light of new information. There is no doubt a new projection is necessary. 90 PART III FINANCIAL PLANNING THE ALTERNATIVES "What will you do in the event of a cash shortfall?" Purcell asks. Harding ex- plains the options available. The resort could postpone or reduce the renova- tions, delay accounts payable, ask the owners for additional money, arrange a loan with the resort's bank, or use some combination of these options. There are problems with most of these alternatives, however. If the renova- tions are not made in January, sales will likely suffer in future months, the resort is showing signs of wear, and it is important to alter the hotel's decor periodi- cally. And, of course, the renovations are best made during an off-peak month like January. Further, the owners at a recent meeting had made it clear that it would be "extremely difficult, if not impossible" for them to raise capital at this time. Nor is the prospect of a loan an appealing option. Relations with the bank have been strained since the resort nearly went bankrupt a few years ago, before Harding's arrival as manager. The bank, assuming it would grant a loan, is likely to impose severe restrictions on the operation of the resort. That would be interference that neither Harding nor the owners would welcome. Harding's most attractive option is to delay accounts payable with the other alternatives used if needed. He intends to call a meeting of all Deerpark's purveyors and ex- plain the situation. His strategy is to be completely open with the purveyors about Deerpark's fi- nancial plight and ask for a deferment of some, if not all, payments until April. In return he will promise to pay COD when business picks up. "They just might agree to this," he tells Purcell. "We've been a good customer, and it is in their in- terest to help us out. After all, it's not like we're in danger of bankruptcy. Reservations for next April through September are extremely strong, and we should be rolling in cash by early summer. In any event, we've got to do another forecast. I must know how bad the situation is. Do I ask them to postpone 50 per- cent of what we purchase, 75 percent, 100 percent? I'm not even sure a complete deferment will be enough." Harding then asks Purcell to prepare a cash budget for October through March. He hands Purcell a revised estimate of sales (see Exhibit 1) and reminds Purcell that sales in September were $448,000. Typically, 70 percent of the resort's sales are paid in cash and 30 percent are paid using the resort's Deerpark Charge and collected in the month following the sale. Deerpark also incurs the following monthly expenses: mortgage, $50,000; utilities and maintenance, $70,000; and lease, rental, and miscellaneous expenses, $25,000. Property taxes of $107,000 are due in February, income taxes of $5,000 are due in December and March, and the renovations will be paid for in January. Exhibit 2 shows the resort's estimated payroll and purveyor ex- penses. Half of the purveyor expenses are paid one month after they are in- curred and half in two months. Deerpark's required minimum cash balance at its bank is $100,000, and the current balance is $550,000. CASE 15 DEERPARK 91 QUESTIONS 1. Should the resort's depreciation expense of $30,000 per month be consid- ered in your cash budget? Explain. 2. Prepare a cash budget for the period October through March. 3. Is there any advantage to extending the forecast through April and May? Explain. 4. Let's assume Deerpark's cash flow would not be sufficient to cover any shortfall occurring during the October-through-March period. What amount of payables must be deferred to get the resort through this period? 5. Harding in essence will be asking the firm's vendors for a loan. From Deerpark's point of view, the size of the loan is your answer to question 4. From the suppliers' point of view, however, the size of their investment in the loan is actually less than that amount. Explain why. (Hint: The price charged will reflect the suppliers' costs plus profit, and costs are the sum of fixed and variable costs). 6. Do Deerpark's purveyors have an incentive to cooperate? Explain. 7. If the purveyors are unable or unwilling to cooperate, how do you think Harding should proceed? 8. Which do you think is more likely to revise a cash budget: a firm like Deerpark or an electric utility? Explain. 9. What do you think is the most important variable in a cash budget forecast? Why? 10. Do you think that a cash budget is a more important financial tool for a small firm like Deerpark or a large firm like Exxon? Explain. SOFTWARE QUESTION 11. Patrick Harding, the resort's manager, is convinced that the estimates used to develop the October-March cash budget are as accurate as he can make them. Thus, he intends to ask the resort's purveyors for an extension of $285,700. He intends to pay COD (cash on delivery) effective April and will use any surplus monthly cash to repay the purveyors. The purveyors have indicated in preliminary conversations that they are willing to cooperate. In order to help their planning, however, they would like Harding to estimate how much of the $285,700 will be paid in April, how much in May, etc. 92 PART III FINANCIAL PLANNING Harding was going to do this anyway, and has compiled the following sales estimates. Month Sales ($000) April 500 May 550 June 560 July 570 August 615 September 650 Past experience, though, indicates that actual sales could be as low as 90 of these estimates or as high as 1.1. He also expects purveyor expenses to equal between 24 and 28 of sales, with a best-guess (most likely) estimate of 26. Past experience indicates that.70 of sales are paid in the month the sale is made, and .30 in the first month after the sale. Harding thinks, however, that come April the hotel's collection procedures may be relaxed a bit. He believes the historical.70/.30 proportions are slightly optimistic. His best-guess esti- mate is that .60 will be paid in the month of the sale, 30 in the following month, and .10 two months after the sale. A pessimistic scenario is propor- tions of .50/.40/.10. Harding decides to develop a cash budget for April-September for the fol- lowing scenarios in order to get an idea of how quickly he can repay the $285,700. SCENARIO (Base-Case) Most Likely Worst- Case Optimistic 1.0 1.1 9 Sales, proportion of base-case estimate Proportion Collected in month t = 0 in month t + 1 in month t + 2 Purveyor expenses/sales .6 3 .1 .6 .4 .0 .5 .4 .1 .26 .24 .28 NOTE: All scenarios assume the purveyors are paid COD come April . The exist- ing credit terms involve paying half one month after an expense is incurred and half in two months. For all scenarios, set "payroll expenses" at.28. Perform the appropriate analysis. When do these results suggest that the pur- veyors will be repaid? Do these results suggest that Harding will need more than the $285,700 originally estimated? CASE 15 DEERPARK 93 EXHIBIT 1 Sales Forecast: October-March Month Sales (000s) $609.5 370.3 October 1995 November December January 1996 February March 257.4 178.2 202.4 288.2 Note: September sales were $448(000). EXHIBIT 2 Forecast of Payroll and Purveyor Expenses Month Payroll (000s) Purveyor (000s) 103,5 October 1995 163.3 November 120.7 December 112.2 January 1996 82.5 February 85.8 March 99.0 Note: Purveyor expenses were $140(000) in August and $120(000) in September. 96.6 50.6 57.2 82.5 105.6 CASE 1 5 DEERPARK CASH BUDGETING "My instincts tell me that we could have cash flow problems sometime in the next six months, Patrick Harding the manager of Deerpark, a West Virginia re- sort, says to Lambert Purcell, the assistant manager. "I need to know now what we're dealing with and I think I'd better redo the cast." CASH FLOW CONCERNS fall. This is Three factors con Three months ago Harding had prepared a cash flow forecast for the period October 1995 to May 1996. November through March is generally a slow period for the resort, and it is not unusual for the lodge to run cash deficits during most, if not all of these months. However, the cash surplus generated during the peak period, from August through October, is typically sufficient to meet the short- precisely what Harding had predicted would occur when he had made the cash budget projection in July. But now, in early October, he is having second thoughts about the forecast concern Harding. First, the renovations planned for January need to be more extensive than originally thought. Harding had estimated the cost to be $420,000, but it appears $500,000 of work is necessary. Second, the re- sort's long-time sales manager left unexpectedly in August and her replacement cession has hit much of the area and Deerpark's sales are definitely sensitive the state of the regional economy All this suggests Harding's sales forecasts, which he had labeled "conservative" in July, are too high. "I can see indications of this now," he tells Purcell. "Revenue is off 10 percent for September and October, and our advance bookings for the rest of the year are also down. I'm sure we won't hit the levels we predicted." Harding has always been an advo- cate of cash budget forecasts and constantly revises an estimate in light of new information. There is no doubt a new projection is necessary. 90 PART III FINANCIAL PLANNING THE ALTERNATIVES "What will you do in the event of a cash shortfall?" Purcell asks. Harding ex- plains the options available. The resort could postpone or reduce the renova- tions, delay accounts payable, ask the owners for additional money, arrange a loan with the resort's bank, or use some combination of these options. There are problems with most of these alternatives, however. If the renova- tions are not made in January, sales will likely suffer in future months, the resort is showing signs of wear, and it is important to alter the hotel's decor periodi- cally. And, of course, the renovations are best made during an off-peak month like January. Further, the owners at a recent meeting had made it clear that it would be "extremely difficult, if not impossible" for them to raise capital at this time. Nor is the prospect of a loan an appealing option. Relations with the bank have been strained since the resort nearly went bankrupt a few years ago, before Harding's arrival as manager. The bank, assuming it would grant a loan, is likely to impose severe restrictions on the operation of the resort. That would be interference that neither Harding nor the owners would welcome. Harding's most attractive option is to delay accounts payable with the other alternatives used if needed. He intends to call a meeting of all Deerpark's purveyors and ex- plain the situation. His strategy is to be completely open with the purveyors about Deerpark's fi- nancial plight and ask for a deferment of some, if not all, payments until April. In return he will promise to pay COD when business picks up. "They just might agree to this," he tells Purcell. "We've been a good customer, and it is in their in- terest to help us out. After all, it's not like we're in danger of bankruptcy. Reservations for next April through September are extremely strong, and we should be rolling in cash by early summer. In any event, we've got to do another forecast. I must know how bad the situation is. Do I ask them to postpone 50 per- cent of what we purchase, 75 percent, 100 percent? I'm not even sure a complete deferment will be enough." Harding then asks Purcell to prepare a cash budget for October through March. He hands Purcell a revised estimate of sales (see Exhibit 1) and reminds Purcell that sales in September were $448,000. Typically, 70 percent of the resort's sales are paid in cash and 30 percent are paid using the resort's Deerpark Charge and collected in the month following the sale. Deerpark also incurs the following monthly expenses: mortgage, $50,000; utilities and maintenance, $70,000; and lease, rental, and miscellaneous expenses, $25,000. Property taxes of $107,000 are due in February, income taxes of $5,000 are due in December and March, and the renovations will be paid for in January. Exhibit 2 shows the resort's estimated payroll and purveyor ex- penses. Half of the purveyor expenses are paid one month after they are in- curred and half in two months. Deerpark's required minimum cash balance at its bank is $100,000, and the current balance is $550,000. CASE 15 DEERPARK 91 QUESTIONS 1. Should the resort's depreciation expense of $30,000 per month be consid- ered in your cash budget? Explain. 2. Prepare a cash budget for the period October through March. 3. Is there any advantage to extending the forecast through April and May? Explain. 4. Let's assume Deerpark's cash flow would not be sufficient to cover any shortfall occurring during the October-through-March period. What amount of payables must be deferred to get the resort through this period? 5. Harding in essence will be asking the firm's vendors for a loan. From Deerpark's point of view, the size of the loan is your answer to question 4. From the suppliers' point of view, however, the size of their investment in the loan is actually less than that amount. Explain why. (Hint: The price charged will reflect the suppliers' costs plus profit, and costs are the sum of fixed and variable costs). 6. Do Deerpark's purveyors have an incentive to cooperate? Explain. 7. If the purveyors are unable or unwilling to cooperate, how do you think Harding should proceed? 8. Which do you think is more likely to revise a cash budget: a firm like Deerpark or an electric utility? Explain. 9. What do you think is the most important variable in a cash budget forecast? Why? 10. Do you think that a cash budget is a more important financial tool for a small firm like Deerpark or a large firm like Exxon? Explain. SOFTWARE QUESTION 11. Patrick Harding, the resort's manager, is convinced that the estimates used to develop the October-March cash budget are as accurate as he can make them. Thus, he intends to ask the resort's purveyors for an extension of $285,700. He intends to pay COD (cash on delivery) effective April and will use any surplus monthly cash to repay the purveyors. The purveyors have indicated in preliminary conversations that they are willing to cooperate. In order to help their planning, however, they would like Harding to estimate how much of the $285,700 will be paid in April, how much in May, etc. 92 PART III FINANCIAL PLANNING Harding was going to do this anyway, and has compiled the following sales estimates. Month Sales ($000) April 500 May 550 June 560 July 570 August 615 September 650 Past experience, though, indicates that actual sales could be as low as 90 of these estimates or as high as 1.1. He also expects purveyor expenses to equal between 24 and 28 of sales, with a best-guess (most likely) estimate of 26. Past experience indicates that.70 of sales are paid in the month the sale is made, and .30 in the first month after the sale. Harding thinks, however, that come April the hotel's collection procedures may be relaxed a bit. He believes the historical.70/.30 proportions are slightly optimistic. His best-guess esti- mate is that .60 will be paid in the month of the sale, 30 in the following month, and .10 two months after the sale. A pessimistic scenario is propor- tions of .50/.40/.10. Harding decides to develop a cash budget for April-September for the fol- lowing scenarios in order to get an idea of how quickly he can repay the $285,700. SCENARIO (Base-Case) Most Likely Worst- Case Optimistic 1.0 1.1 9 Sales, proportion of base-case estimate Proportion Collected in month t = 0 in month t + 1 in month t + 2 Purveyor expenses/sales .6 3 .1 .6 .4 .0 .5 .4 .1 .26 .24 .28 NOTE: All scenarios assume the purveyors are paid COD come April . The exist- ing credit terms involve paying half one month after an expense is incurred and half in two months. For all scenarios, set "payroll expenses" at.28. Perform the appropriate analysis. When do these results suggest that the pur- veyors will be repaid? Do these results suggest that Harding will need more than the $285,700 originally estimated? CASE 15 DEERPARK 93 EXHIBIT 1 Sales Forecast: October-March Month Sales (000s) $609.5 370.3 October 1995 November December January 1996 February March 257.4 178.2 202.4 288.2 Note: September sales were $448(000). EXHIBIT 2 Forecast of Payroll and Purveyor Expenses Month Payroll (000s) Purveyor (000s) 103,5 October 1995 163.3 November 120.7 December 112.2 January 1996 82.5 February 85.8 March 99.0 Note: Purveyor expenses were $140(000) in August and $120(000) in September. 96.6 50.6 57.2 82.5 105.6Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Health Care Finance Basic Tools For Nonfinancial Managers

Authors: Judith J. Baker, R.W. Baker, Neil R. Dworkin

5th Edition

1284118215, 978-1284118216