Please answer only if you can answer all the questions correctly!!! Please Skip and leave for other experts if you cannot. I need proper explained answers for each question.

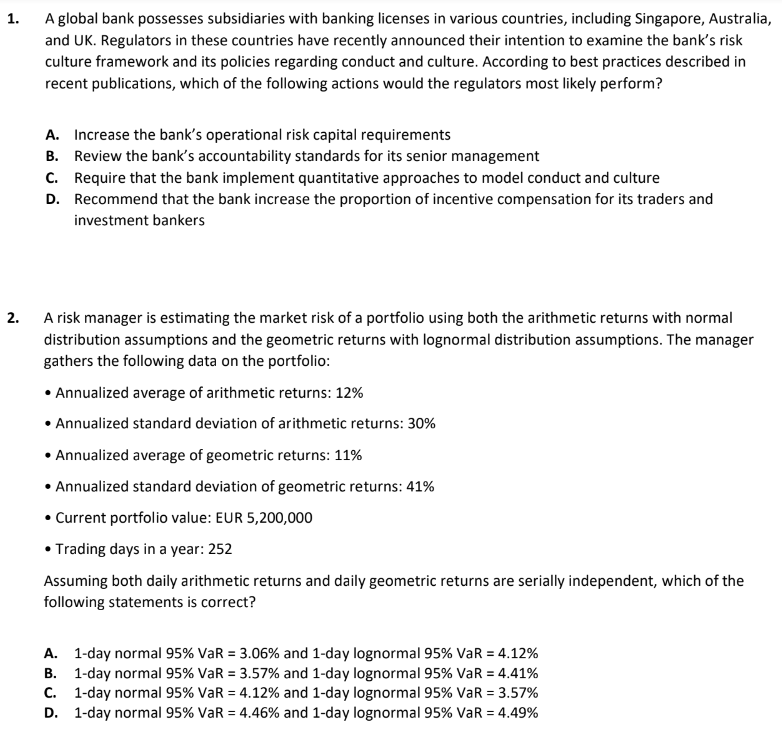

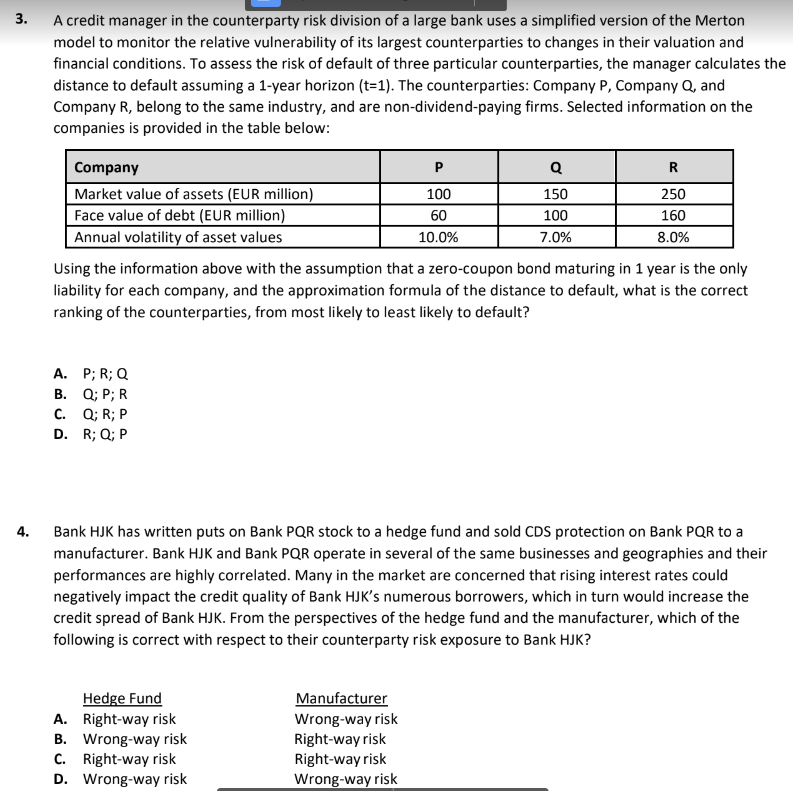

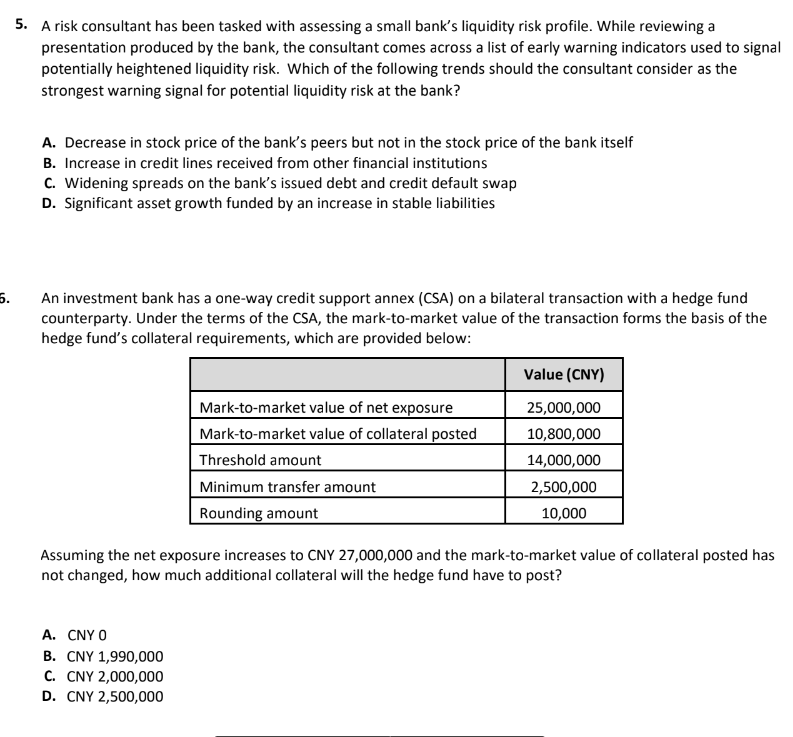

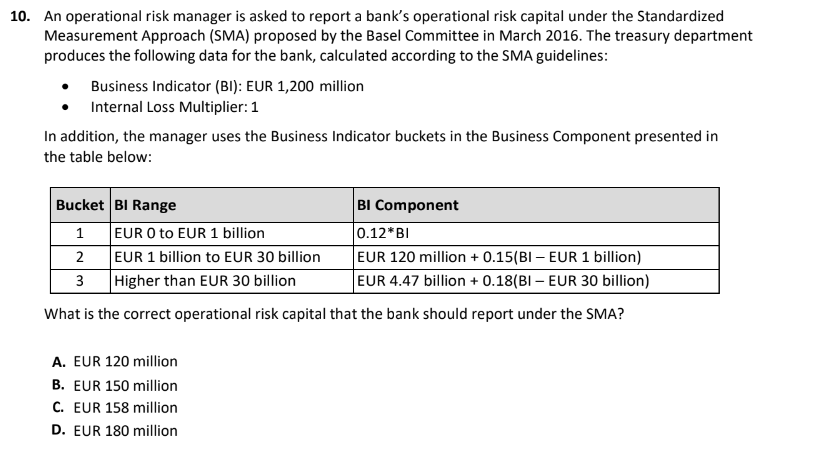

1. A global bank possesses subsidiaries with banking licenses in various countries, including Singapore, Australia and UK. Regulators in these countries have recently announced their intention to examine the bank's risk culture framework and its policies regarding conduct and culture. According to best practices described in recent publications, which of the following actions would the regulators most likely perform? A. Increase the bank's operational risk capital requirements B. Review the bank's accountability standards for its senior management C. Require that the bank implement quantitative approaches to model conduct and culture D. Recommend that the bank increase the proportion of incentive compensation for its traders and investment bankers 2. A risk manager is estimating the market risk of a portfolio using both the arithmetic returns with normal distribution assumptions and the geometric returns with lognormal distribution assumptions. The manager gathers the following data on the portfolio: - Annualized average of arithmetic returns: 12% - Annualized standard deviation of arithmetic returns: 30% - Annualized average of geometric returns: 11% - Annualized standard deviation of geometric returns: 41% - Current portfolio value: EUR 5,200,000 - Trading days in a year: 252 Assuming both daily arithmetic returns and daily geometric returns are serially independent, which of the following statements is correct? A. 1-day normal 95%VaR=3.06% and 1-day lognormal 95%VaR=4.12% B. 1-day normal 95%VaR=3.57% and 1-day lognormal 95%VaR=4.41% C. 1-day normal 95%VaR=4.12% and 1-day lognormal 95%VaR=3.57% D. 1-day normal 95%VaR=4.46% and 1-day lognormal 95%VaR=4.49% A credit manager in the counterparty risk division of a large bank uses a simplified version of the Merton model to monitor the relative vulnerability of its largest counterparties to changes in their valuation and financial conditions. To assess the risk of default of three particular counterparties, the manager calculates th distance to default assuming a 1-year horizon ( t=1 ). The counterparties: Company P, Company Q, and Company R, belong to the same industry, and are non-dividend-paying firms. Selected information on the companies is provided in the table below: Using the information above with the assumption that a zero-coupon bond maturing in 1 year is the only liability for each company, and the approximation formula of the distance to default, what is the correct ranking of the counterparties, from most likely to least likely to default? A. P; R; Q B. Q; P; R C. Q; R; P D. R; Q; P Bank HJK has written puts on Bank PQR stock to a hedge fund and sold CDS protection on Bank PQR to a manufacturer. Bank HJK and Bank PQR operate in several of the same businesses and geographies and their performances are highly correlated. Many in the market are concerned that rising interest rates could negatively impact the credit quality of Bank HJK's numerous borrowers, which in turn would increase the credit spread of Bank HJK. From the perspectives of the hedge fund and the manufacturer, which of the following is correct with respect to their counterparty risk exposure to Bank HJK? 5. A risk consultant has been tasked with assessing a small bank's liquidity risk profile. While reviewing a presentation produced by the bank, the consultant comes across a list of early warning indicators used to signal potentially heightened liquidity risk. Which of the following trends should the consultant consider as the strongest warning signal for potential liquidity risk at the bank? A. Decrease in stock price of the bank's peers but not in the stock price of the bank itself B. Increase in credit lines received from other financial institutions C. Widening spreads on the bank's issued debt and credit default swap D. Significant asset growth funded by an increase in stable liabilities An investment bank has a one-way credit support annex (CSA) on a bilateral transaction with a hedge fund counterparty. Under the terms of the CSA, the mark-to-market value of the transaction forms the basis of the hedge fund's collateral requirements, which are provided below: Assuming the net exposure increases to CNY 27,000,000 and the mark-to-market value of collateral posted has not changed, how much additional collateral will the hedge fund have to post? A. CNY 0 B. CNY 1,990,000 C. CNY 2,000,000 D. CNY 2,500,000 The board of directors of an insurance company has identified a number of potential growth opportunities for the company to consider. To help assess these opportunities and determine an optimal risk structure to use across the organization, the risk committee has recommended that the company implement an ERM program. Which of the following would best represent an appropriate goal for the firm to state as part of the ERM program? A. Determine a risk-return trade-off that reflects the company's target credit rating and ensure that business unit managers evaluate new projects with this firm-wide target in mind. B. Attempt to eliminate the company's probability of financial distress to maximize company value. c. Maximize the firm's leverage ratio within its risk tolerance to ensure the highest expected return on equity. D. Establish a target minimum level of annual earnings and guarantee to shareholders that it will maintain this level. 8. A US pension fund had assets and liabilities valued at USD 840 million and USD 450 million, respectively, at the end of 2017. The fund's assets were fully invested in equities and commodities while its liabilities consisted entirely of fixed-income obligations. The fund reported that by the end of 2018 the value of assets decreased by 14.0% and the value of liabilities increased by 3.5%. Assuming no changes were made to the composition of the assets and liabilities during the year, what was the change in the pension fund's surplus over the 1-year period? A. USD -133.4 million B. USD - 117.6 million C. USD 256.7 million D. USD 390.0 million A wealth management firm has a portfolio consisting of USD 37 million invested in US equities and USD 48 million invested in emerging markets equities. The US equities and emerging markets equities both have a 1-day 95% VaR of USD 1.3 million. The correlation between the returns of the US equities and emerging markets equities is 0.25. While rebalancing the portfolio, the manager in charge decides to sell USD 7 million of the US equities to buy USD 7 million of the emerging markets equities. At the same time, the CRO of the firm advises the portfolio manager to change the risk measure from 1-day 95% VaR to 10-day 99% VaR. Assuming that returns are normally distributed and that the rebalancing does not affect the volatility of the individual equity positions, by how much will the portfolio VaR increase due to the combined effect of portfolio rebalancing and change in risk measure? A. USD 4.373 million B. USD 6.428 million C. USD 7.034 million D. USD 9.089 million An operational risk manager is asked to report a bank's operational risk capital under the Standardized Measurement Approach (SMA) proposed by the Basel Committee in March 2016. The treasury department produces the following data for the bank, calculated according to the SMA guidelines: - Business Indicator (BI): EUR 1,200 million - Internal Loss Multiplier: 1 In addition, the manager uses the Business Indicator buckets in the Business Component presented in the table below: What is the correct operational risk capital that the bank should report under the SMA? A. EUR 120 million B. EUR 150 million C. EUR 158 million D. EUR 180 million