Answered step by step

Verified Expert Solution

Question

1 Approved Answer

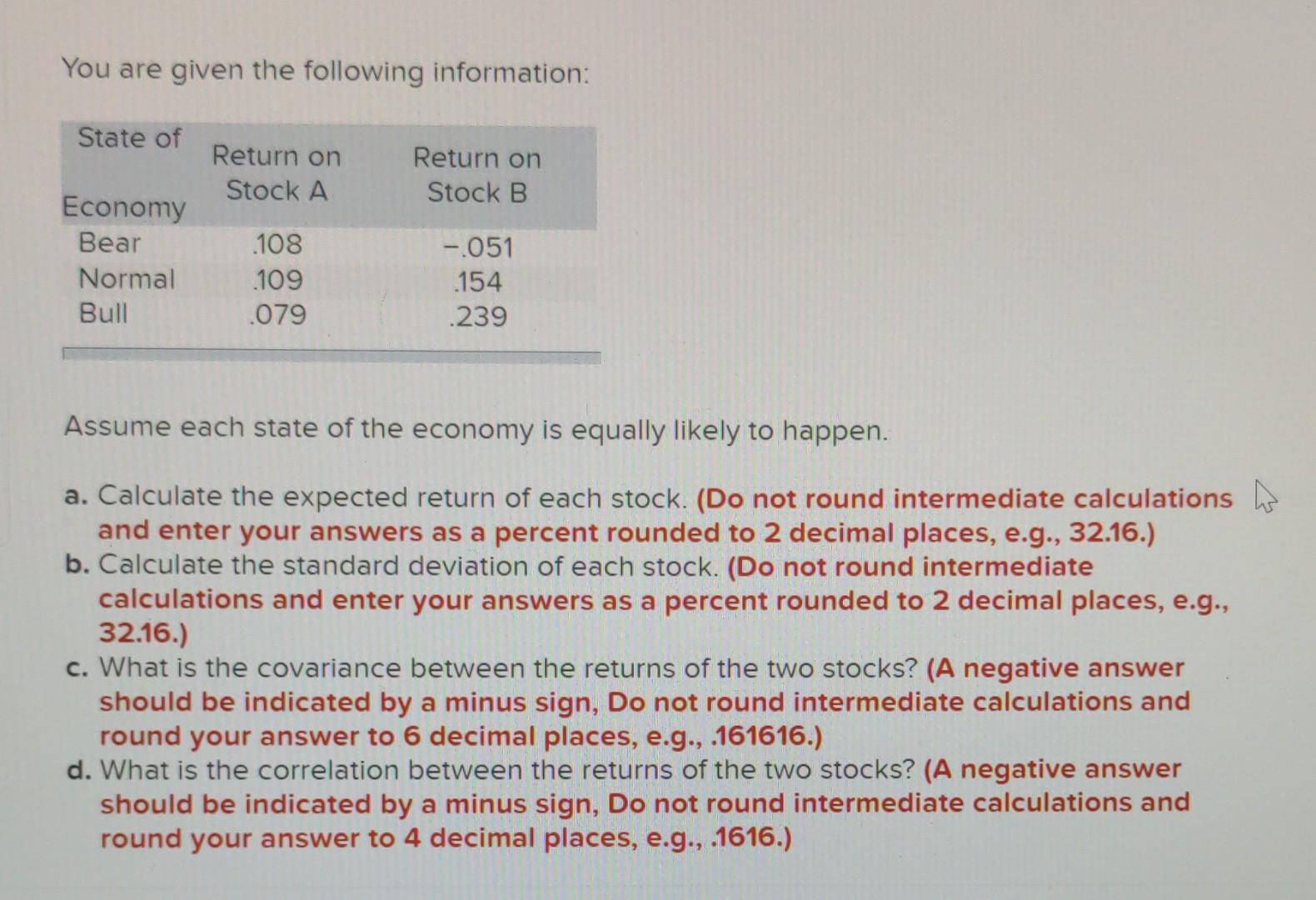

Please answer part A-D. You are given the following information: State of Return on Stock A Return on Stock B Economy Bear Normal Bull 108

Please answer part A-D.

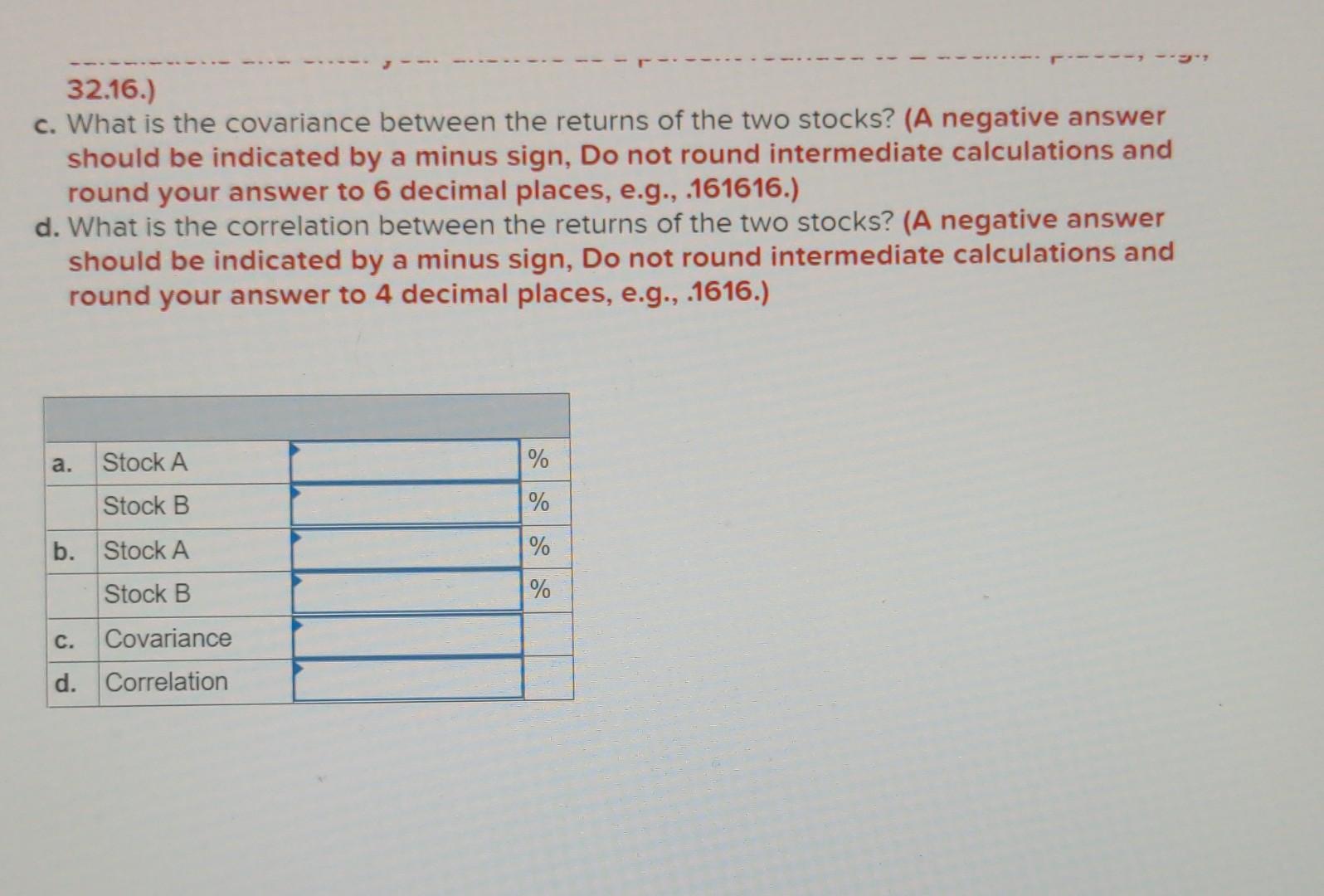

You are given the following information: State of Return on Stock A Return on Stock B Economy Bear Normal Bull 108 109 079 -.051 .154 .239 Assume each state of the economy is equally likely to happen. a. Calculate the expected return of each stock. (Do not round intermediate calculations as and enter your answers as a percent rounded to 2 decimal places, e.g., 32.16.) b. Calculate the standard deviation of each stock. (Do not round intermediate calculations and enter your answers as a percent rounded to 2 decimal places, e.g., 32.16.) c. What is the covariance between the returns of the two stocks? (A negative answer should be indicated by a minus sign, Do not round intermediate calculations and round your answer to 6 decimal places, e.g., .161616.) d. What is the correlation between the returns of the two stocks? (A negative answer should be indicated by a minus sign, Do not round intermediate calculations and round your answer to 4 decimal places, e.g., 1616.) 32.16.) c. What is the covariance between the returns of the two stocks? (A negative answer should be indicated by a minus sign, Do not round intermediate calculations and round your answer to 6 decimal places, e.g., 161616.) d. What is the correlation between the returns of the two stocks? (A negative answer should be indicated by a minus sign, Do not round intermediate calculations and round your answer to 4 decimal places, e.g., 1616.) a. Stock A % Stock B % b. Stock A % Stock B % C. Covariance d. CorrelationStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Everything Improve Your Credit Book

Authors: Justin Pritchard

1st Edition

1598691554, 978-1598691559