Answered step by step

Verified Expert Solution

Question

1 Approved Answer

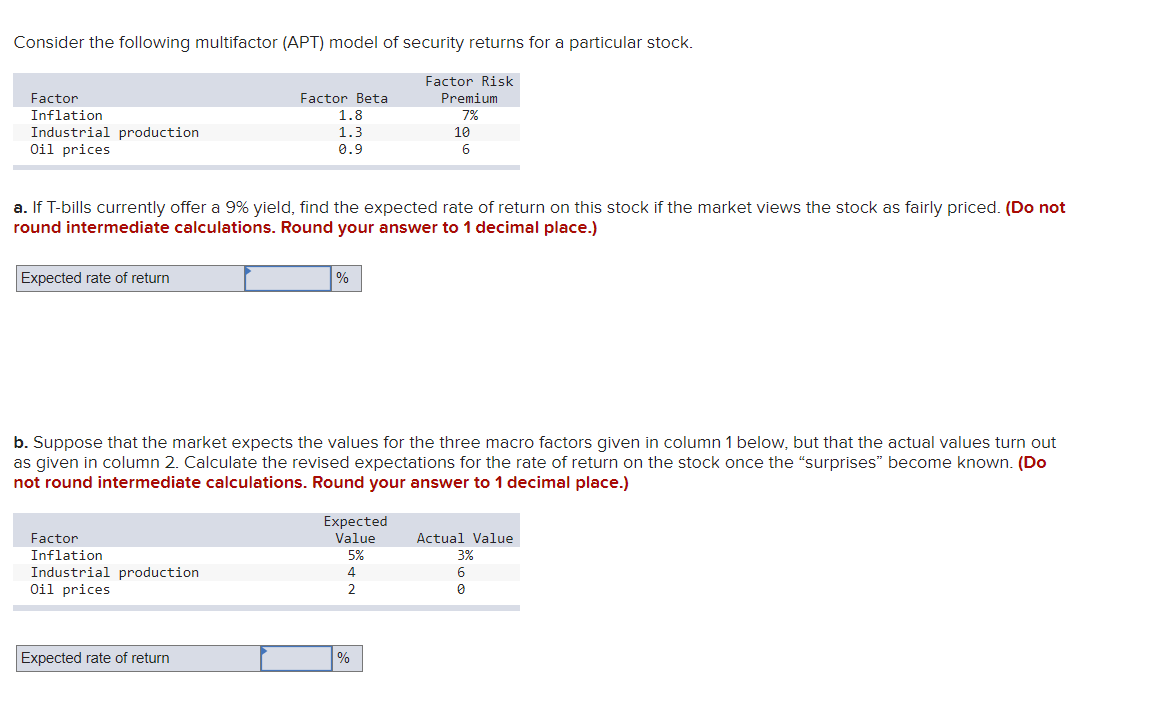

Please answer question 5 with parts A and B . Show work please. Consider the following multifactor (APT) model of security returns for a particular

Please answer question with parts A and B Show work please.

Consider the following multifactor (APT) model of security returns for a particular stock 1.8 1.3 Factor Inflation Industrial production Oil prices Factor Beta Factor Risk Premium 10 6 a. If T-bills currently offer a 9% yield, find the expected rate of return on this stock if the market views the stock as fairly priced. (Do not round intermediate calculations. Round your answer to 1 decimal place.) Expected rate of return 0/0 b. Suppose that the market expects the values for the three macro factors given in column 1 below, but that the actual values turn out as given in column 2_ Calculate the revised expectations for the rate of return on the stock once the "surprises" become known. (Do not round intermediate calculations. Round your answer to 1 decimal place.) Factor Inflation Industrial production Oil prices Expected rate of return Expected Value 4 2 0/0 Actual Value 6

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Reporting And Statement Analysis A Strategic Approach

Authors: Clyde P. Stickney, Paul Brown, James M. Wahlen

5th Edition

032418638X, 978-0324186383