Please answer question 6 only. The rest of the content is only there to provide context.

"Note that the sum of the variances computed in parts 1-4 does NOT add up to the total over/under applied cost. Briefly explain why not (2-3 sentences should be sufficient). It is sufficient to point out which variances should be included or excluded in order to arrive at the total over/under applied cost."

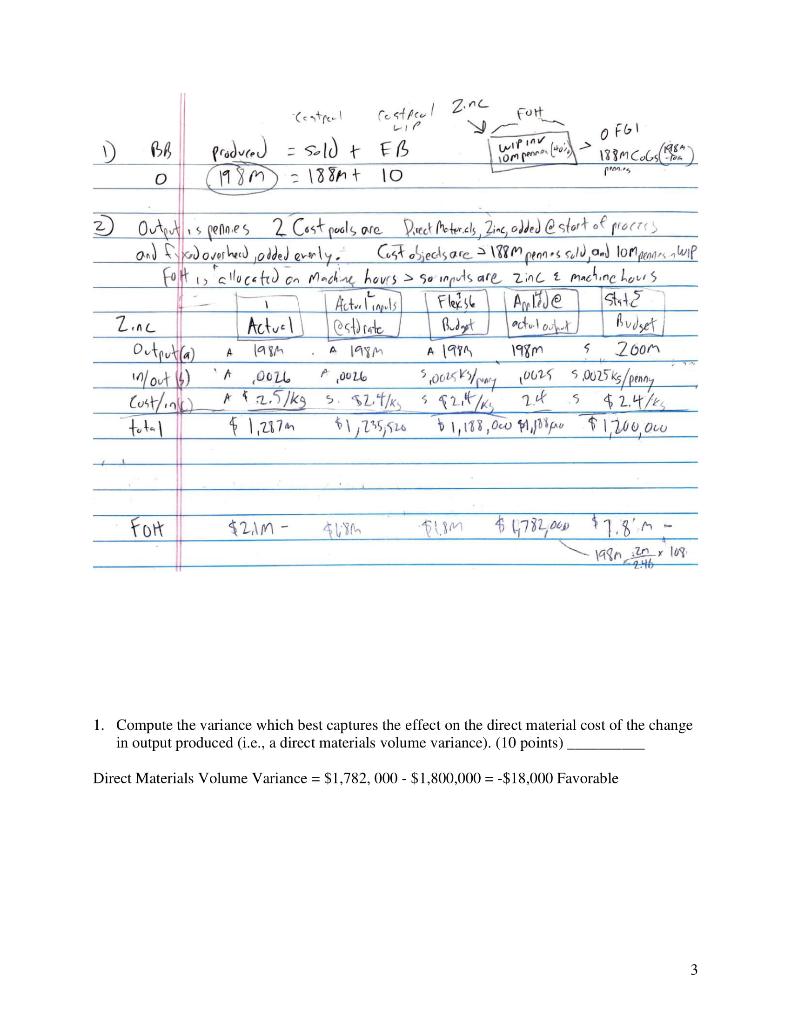

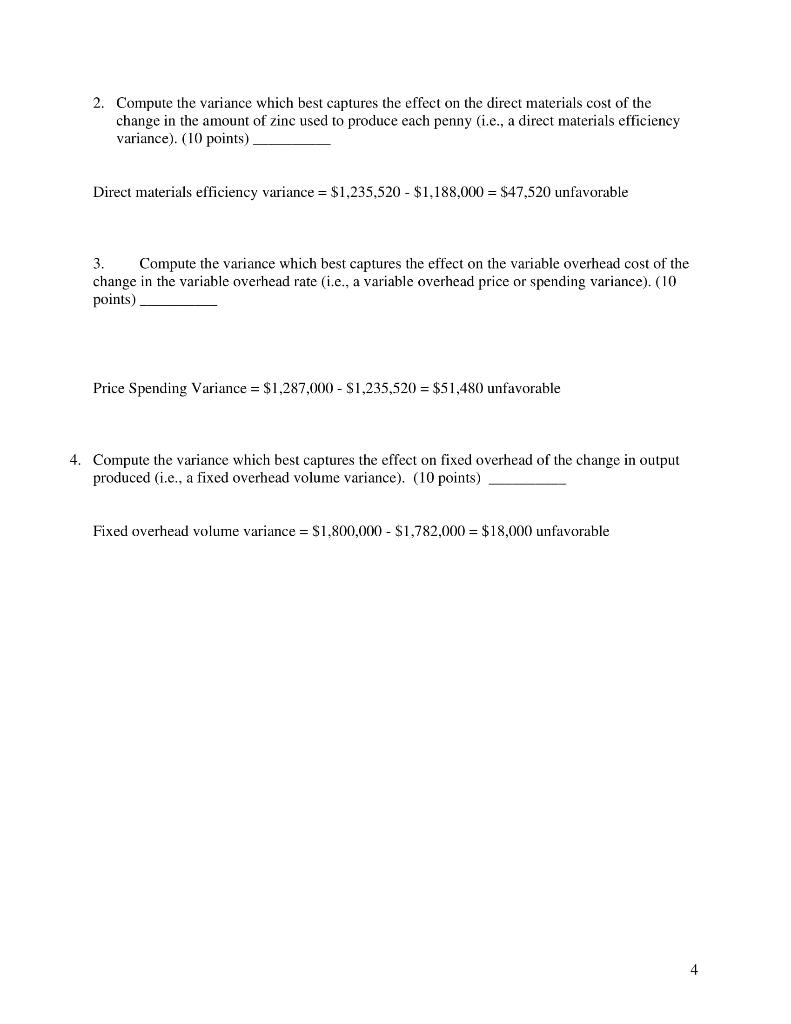

I. U.S. Mint (75 points) One department of the U.S. Mint in Denver produces about half of all U.S. pennies (and nothing else). All questions in this problem relate only to the department which produces pennies. The U.S. Mint has a standard absorption costing system, and uses weighted average for all inventories. This system has two cost pools. Direct material (zinc) is added at the beginning of the production process, and overhead costs (which includes the copper coating) are added evenly during the production process. All overhead costs are allocated based on machine hours. The department's annual static budget called for producing 2.4 billion pennies at a cost of $43.2m, as follows: $14.4m Direct Materials (6 million kilograms of zinc) Overhead Cost (based on 200.000 machine hours) Variable Cost Fixed Cost Total Overhead Cost Total Cost $ 7.2m $21.6m $28.8m $43.2m Note that the static budget assumes that there is no inventory of any kind, and that production will occur evenly during the year. Actual Results: On February 1, there is no inventory anywhere in the department, but at February 28 the department has a batch of ten million pennies which are 40% through the production process. All other pennies produced are "sold". During the month of February, the department begins production of 198 million pennies. Each penny requires 2.6 grams of zinc (one kilogram is 1000 grams). The mint buys zinc at a price of $2.5/kilogram. During the month of February, actual overhead costs are $2.1m, $0.42m of which are due to variable costs. Each machine hour actually produces 16,000 pennies, All variances are computed based on the equivalent number of pennies produced, and are closed to cost of goods sold at the end of each month. 2 FUH Cestpeel zinc OFGI 1 BB Centreal = sold & EB - 188m+ 10 Produced 198m 7184 188M Cobston 1ompona ( ps 0 1 2 Output is pennies 2 Cost pools are Direct Materials, Zine, added @ start of process and find overhead added evenly. Cost objects are 188 m pennes sold, and 10m penes wip Folt is allocated on Machine haves > so inputs are zinc & machine hours Actuel impuls Flexst Aulide Stats Zinc Actual iestorate Budget lactulouht Budget Output(a) 198M A 1989 1987 200m 0026 s posks may 10625 S0025 ks/penny Cust/ink) A1.2.5kg 52t/ks 592.4k 24 $2,4/ky total $ 1,287m $1, 235,926 + 1, 188, Owo $1,200, ou A 1991 5 Mout b). P 0026 5 S FoH $21M- $180 11,8M $1,782,000 $7.8 m - 198n zn log 1. Compute the variance which best captures the effect on the direct material cost of the change in output produced (i.e., a direct materials volume variance). (10 points) Direct Materials Volume Variance = $1,782,000 - $1,800,000 = -$18,000 Favorable 3 2. Compute the variance which best captures the effect on the direct materials cost of the change in the amount of zinc used to produce each penny (i.e., a direct materials efficiency variance). (10 points) Direct materials efficiency variance = $1,235,520 - $1,188,000 = $47,520 unfavorable 3. Compute the variance which best captures the effect on the variable overhead cost of the change in the variable overhead rate (i.e., a variable overhead price or spending variance). (10 points) Price Spending Variance = $1,287,000 - $1,235,520 = $51,480 unfavorable 4. Compute the variance which best captures the effect on fixed overhead of the change in produced (i.e., a fixed overhead volume variance). (10 points) Fixed overhead volume variance = $1,800,000 - $1,782,000 = $18,000 unfavorable 4 5. How much will be recorded as cost of goods sold before adjusting for over/under-applied costs. (10 points) $1.8M 6. Note that the sum of the variances computed in parts 1-4 does NOT add up to the total over/under applied cost. Briefly explain why not (2-3 sentences should be sufficient). It is sufficient to point out which variances should be included or excluded in order to arrive at the total over/under applied cost. (15 points) 5 I. U.S. Mint (75 points) One department of the U.S. Mint in Denver produces about half of all U.S. pennies (and nothing else). All questions in this problem relate only to the department which produces pennies. The U.S. Mint has a standard absorption costing system, and uses weighted average for all inventories. This system has two cost pools. Direct material (zinc) is added at the beginning of the production process, and overhead costs (which includes the copper coating) are added evenly during the production process. All overhead costs are allocated based on machine hours. The department's annual static budget called for producing 2.4 billion pennies at a cost of $43.2m, as follows: $14.4m Direct Materials (6 million kilograms of zinc) Overhead Cost (based on 200.000 machine hours) Variable Cost Fixed Cost Total Overhead Cost Total Cost $ 7.2m $21.6m $28.8m $43.2m Note that the static budget assumes that there is no inventory of any kind, and that production will occur evenly during the year. Actual Results: On February 1, there is no inventory anywhere in the department, but at February 28 the department has a batch of ten million pennies which are 40% through the production process. All other pennies produced are "sold". During the month of February, the department begins production of 198 million pennies. Each penny requires 2.6 grams of zinc (one kilogram is 1000 grams). The mint buys zinc at a price of $2.5/kilogram. During the month of February, actual overhead costs are $2.1m, $0.42m of which are due to variable costs. Each machine hour actually produces 16,000 pennies, All variances are computed based on the equivalent number of pennies produced, and are closed to cost of goods sold at the end of each month. 2 FUH Cestpeel zinc OFGI 1 BB Centreal = sold & EB - 188m+ 10 Produced 198m 7184 188M Cobston 1ompona ( ps 0 1 2 Output is pennies 2 Cost pools are Direct Materials, Zine, added @ start of process and find overhead added evenly. Cost objects are 188 m pennes sold, and 10m penes wip Folt is allocated on Machine haves > so inputs are zinc & machine hours Actuel impuls Flexst Aulide Stats Zinc Actual iestorate Budget lactulouht Budget Output(a) 198M A 1989 1987 200m 0026 s posks may 10625 S0025 ks/penny Cust/ink) A1.2.5kg 52t/ks 592.4k 24 $2,4/ky total $ 1,287m $1, 235,926 + 1, 188, Owo $1,200, ou A 1991 5 Mout b). P 0026 5 S FoH $21M- $180 11,8M $1,782,000 $7.8 m - 198n zn log 1. Compute the variance which best captures the effect on the direct material cost of the change in output produced (i.e., a direct materials volume variance). (10 points) Direct Materials Volume Variance = $1,782,000 - $1,800,000 = -$18,000 Favorable 3 2. Compute the variance which best captures the effect on the direct materials cost of the change in the amount of zinc used to produce each penny (i.e., a direct materials efficiency variance). (10 points) Direct materials efficiency variance = $1,235,520 - $1,188,000 = $47,520 unfavorable 3. Compute the variance which best captures the effect on the variable overhead cost of the change in the variable overhead rate (i.e., a variable overhead price or spending variance). (10 points) Price Spending Variance = $1,287,000 - $1,235,520 = $51,480 unfavorable 4. Compute the variance which best captures the effect on fixed overhead of the change in produced (i.e., a fixed overhead volume variance). (10 points) Fixed overhead volume variance = $1,800,000 - $1,782,000 = $18,000 unfavorable 4 5. How much will be recorded as cost of goods sold before adjusting for over/under-applied costs. (10 points) $1.8M 6. Note that the sum of the variances computed in parts 1-4 does NOT add up to the total over/under applied cost. Briefly explain why not (2-3 sentences should be sufficient). It is sufficient to point out which variances should be included or excluded in order to arrive at the total over/under applied cost. (15 points) 5