Answered step by step

Verified Expert Solution

Question

1 Approved Answer

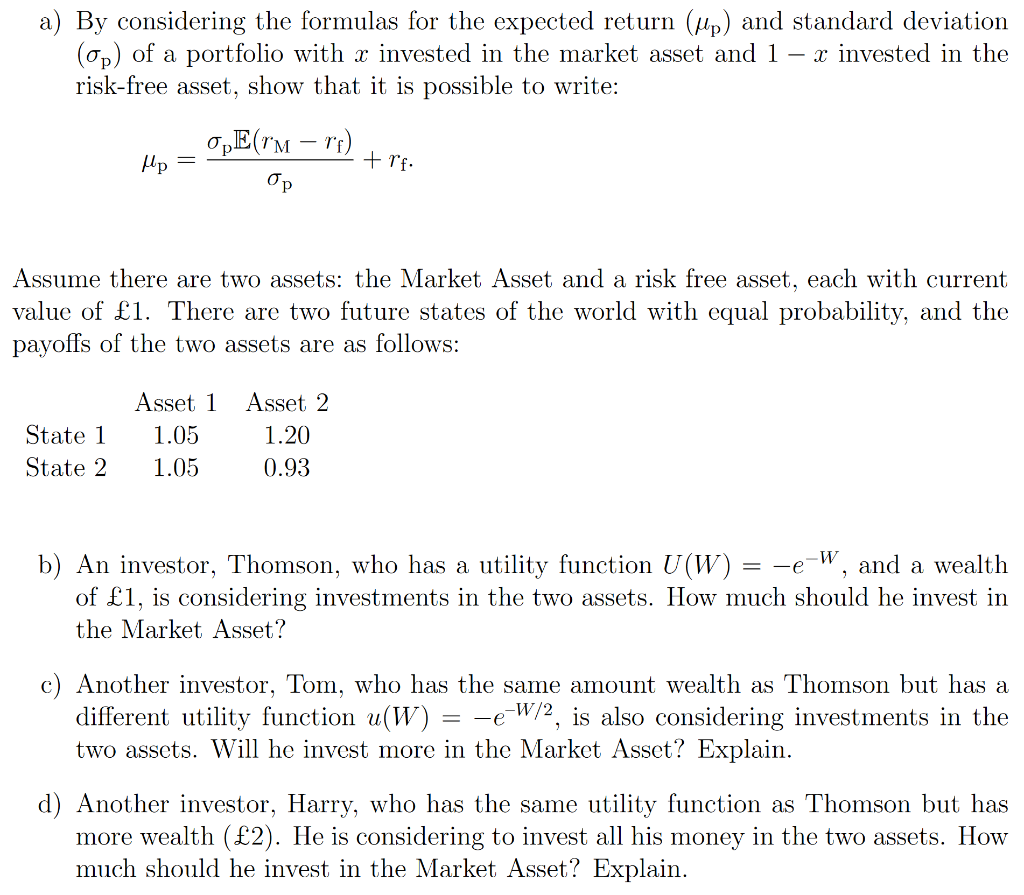

please answer question a) b) c) and d) a) By considering the formulas for the expected return (up) and standard deviation (op) of a portfolio

please answer question a) b) c) and d)

a) By considering the formulas for the expected return (up) and standard deviation (op) of a portfolio with x invested in the market asset and 1 x invested in the risk-free asset, show that it is possible to write: OPE(Tm rf) +rf: Op Assume there are two assets: the Market Asset and a risk free asset, each with current value of 1. There are two future states of the world with equal probability, and the payoffs of the two assets are as follows: State 1 State 2 Asset 1 1.05 1.05 Asset 2 1.20 0.93 = -e b) An investor, Thomson, who has a utility function U(W) -W, and a wealth of 1, is considering investments in the two assets. How much should he invest in the Market Asset? c) Another investor, Tom, who has the same amount wealth as Thomson but has a different utility function u(W) = -e-W/2, is also considering investments in the two assets. Will he invest more in the Market Asset? Explain. d) Another investor, Harry, who has the same utility function as Thomson but has more wealth (2). He is considering to invest all his money in the two assets. How much should he invest in the Market Asset? Explain. a) By considering the formulas for the expected return (up) and standard deviation (op) of a portfolio with x invested in the market asset and 1 x invested in the risk-free asset, show that it is possible to write: OPE(Tm rf) +rf: Op Assume there are two assets: the Market Asset and a risk free asset, each with current value of 1. There are two future states of the world with equal probability, and the payoffs of the two assets are as follows: State 1 State 2 Asset 1 1.05 1.05 Asset 2 1.20 0.93 = -e b) An investor, Thomson, who has a utility function U(W) -W, and a wealth of 1, is considering investments in the two assets. How much should he invest in the Market Asset? c) Another investor, Tom, who has the same amount wealth as Thomson but has a different utility function u(W) = -e-W/2, is also considering investments in the two assets. Will he invest more in the Market Asset? Explain. d) Another investor, Harry, who has the same utility function as Thomson but has more wealth (2). He is considering to invest all his money in the two assets. How much should he invest in the Market Asset? ExplainStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Private Equity Mathematics

Authors: Oliver Gottschalg

1st Edition

1908783508, 9781908783509