Answered step by step

Verified Expert Solution

Question

1 Approved Answer

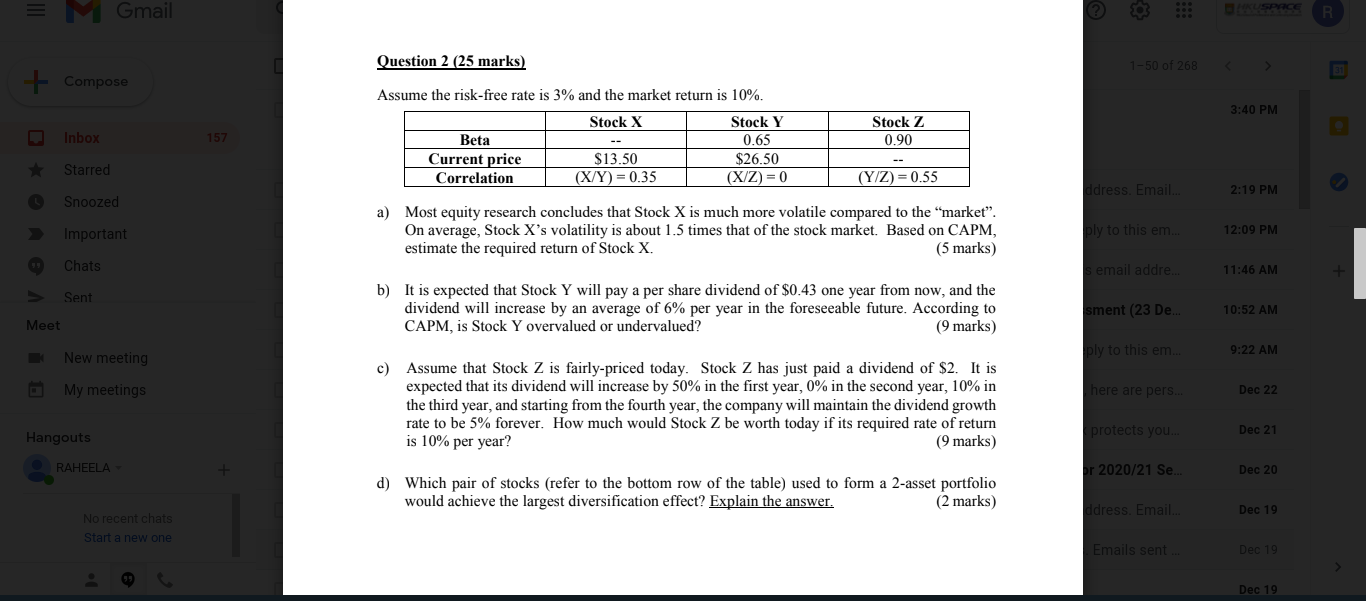

please answer question b NGmail 3 R Question 2 (25 marks) 1-50 of 268 33 + Compose 3:40 PM Stock Z 0.90 Inbox Assume the

please answer question b

NGmail 3 R Question 2 (25 marks) 1-50 of 268 33 + Compose 3:40 PM Stock Z 0.90 Inbox Assume the risk-free rate is 3% and the market return is 10% Stock X Stock Y Beta 0.65 Current price $13.50 $26.50 Correlation (X/Y) = 0.35 (X/Z) = 0 157 Starred (Y/Z) = 0.55 ddress Email 2:19 PM Snoozed Important a) Most equity research concludes that Stock X is much more volatile compared to the "market. On average, Stock X's volatility is about 1.5 times that of the stock market. Based on CAPM, estimate the required return of Stock X. (5 marks) ply to this em... 12:09 PM Chats email addre 11:46 AM Sent b) It is expected that Stock Y will pay a per share dividend of $0.43 one year from now, and the dividend will increase by an average of 6% per year in the foreseeable future. According to CAPM, is Stock Y overvalued or undervalued? (9 marks) sment (23 De. 10:52 AM Meet New meeting 9:22 AM ply to this em.. My meetings here are pers... Dec 22 c) Assume that Stock Z is fairly-priced today. Stock Z has just paid a dividend of $2. It is expected that its dividend will increase by 50% in the first year, 0% in the second year, 10% in the third year, and starting from the fourth year, the company will maintain the dividend growth rate to be 5% forever. How much would Stock Z be worth today if its required rate of return is 10% per year? (9 marks) Hangouts Dec 21 protects you. RAHEELA pr 2020/21 Se. Dec 20 d) Which pair of stocks (refer to the bottom row of the table) used to form a 2-asset portfolio would achieve the largest diversification effect? Explain the answer. (2 marks) ddress. Email.. Dec 19 No recent chats Start a new one Emails sent Dec 19 Dec 19Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Public Finance

Authors: Harvey Rosen, Robert Guell, Ted Gayer

9th Edition

0073511358, 9780073511351