Please answer question in picture 2.

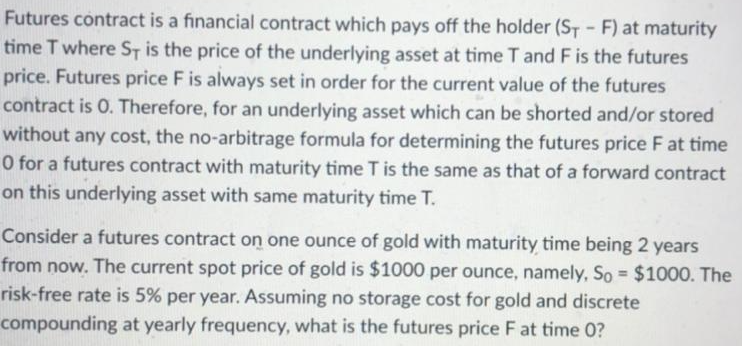

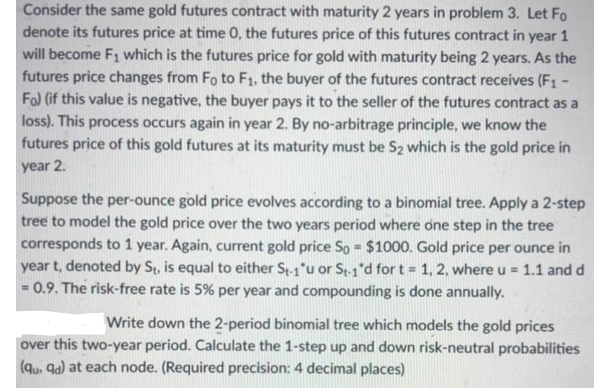

Futures contract is a financial contract which pays off the holder (ST-F) at maturity time T where Sy is the price of the underlying asset at time T and F is the futures price. Futures price F is always set in order for the current value of the futures contract is 0. Therefore, for an underlying asset which can be shorted and/or stored without any cost, the no-arbitrage formula for determining the futures price Fat time O for a futures contract with maturity time T is the same as that of a forward contract on this underlying asset with same maturity time T. Consider a futures contract on one ounce of gold with maturity time being 2 years from now. The current spot price of gold is $1000 per ounce, namely, So = $1000. The risk-free rate is 5% per year. Assuming no storage cost for gold and discrete compounding at yearly frequency, what is the futures price Fat time 0? Consider the same gold futures contract with maturity 2 years in problem 3. Let Fo denote its futures price at time 0, the futures price of this futures contract in year 1 will become F1 which is the futures price for gold with maturity being 2 years. As the futures price changes from Foto F1, the buyer of the futures contract receives (F1 - Fo) (if this value is negative, the buyer pays it to the seller of the futures contract as a loss). This process occurs again in year 2. By no-arbitrage principle, we know the futures price of this gold futures at its maturity must be S2 which is the gold price in year 2. Suppose the per-ounce gold price evolves according to a binomial tree. Apply a 2-step tree to model the gold price over the two years period where one step in the tree corresponds to 1 year. Again, current gold price So - $1000. Gold price per ounce in year t, denoted by St, is equal to either St-1'u or St.1*d for t = 1, 2, where u = 1.1 and d = 0.9. The risk-free rate is 5% per year and compounding is done annually. Write down the 2-period binomial tree which models the gold prices over this two-year period. Calculate the 1-step up and down risk-neutral probabilities (qu. 9a) at each node. (Required precision: 4 decimal places) Futures contract is a financial contract which pays off the holder (ST-F) at maturity time T where Sy is the price of the underlying asset at time T and F is the futures price. Futures price F is always set in order for the current value of the futures contract is 0. Therefore, for an underlying asset which can be shorted and/or stored without any cost, the no-arbitrage formula for determining the futures price Fat time O for a futures contract with maturity time T is the same as that of a forward contract on this underlying asset with same maturity time T. Consider a futures contract on one ounce of gold with maturity time being 2 years from now. The current spot price of gold is $1000 per ounce, namely, So = $1000. The risk-free rate is 5% per year. Assuming no storage cost for gold and discrete compounding at yearly frequency, what is the futures price Fat time 0? Consider the same gold futures contract with maturity 2 years in problem 3. Let Fo denote its futures price at time 0, the futures price of this futures contract in year 1 will become F1 which is the futures price for gold with maturity being 2 years. As the futures price changes from Foto F1, the buyer of the futures contract receives (F1 - Fo) (if this value is negative, the buyer pays it to the seller of the futures contract as a loss). This process occurs again in year 2. By no-arbitrage principle, we know the futures price of this gold futures at its maturity must be S2 which is the gold price in year 2. Suppose the per-ounce gold price evolves according to a binomial tree. Apply a 2-step tree to model the gold price over the two years period where one step in the tree corresponds to 1 year. Again, current gold price So - $1000. Gold price per ounce in year t, denoted by St, is equal to either St-1'u or St.1*d for t = 1, 2, where u = 1.1 and d = 0.9. The risk-free rate is 5% per year and compounding is done annually. Write down the 2-period binomial tree which models the gold prices over this two-year period. Calculate the 1-step up and down risk-neutral probabilities (qu. 9a) at each node. (Required precision: 4 decimal places)