Answered step by step

Verified Expert Solution

Question

1 Approved Answer

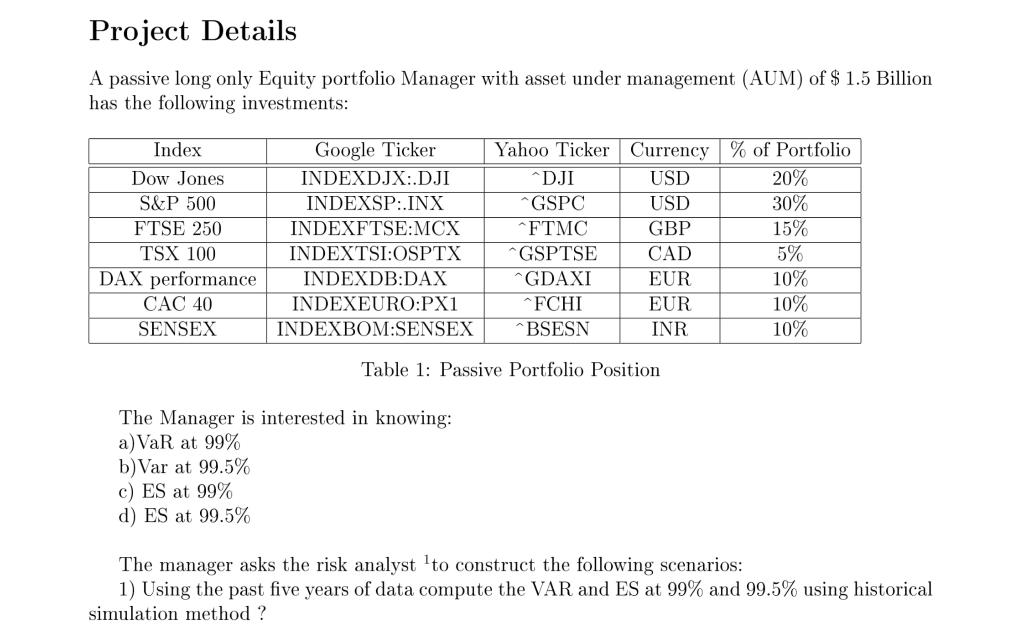

please answer question using excel sheet and provide formulas and work done for question 1, ty A passive long only Equity portfolio Manager with asset

please answer question using excel sheet and provide formulas and work done for question 1, ty

A passive long only Equity portfolio Manager with asset under management (AUM) of $1.5 Billion has the following investments: Table 1: Passive Portfolio Position The Manager is interested in knowing: a) VaR at 99% b) Var at 99.5% c) ES at 99% d) ES at 99.5% The manager asks the risk analyst 1 to construct the following scenarios: 1) Using the past five years of data compute the VAR and ES at 99% and 99.5% using historical simulation method? A passive long only Equity portfolio Manager with asset under management (AUM) of $1.5 Billion has the following investments: Table 1: Passive Portfolio Position The Manager is interested in knowing: a) VaR at 99% b) Var at 99.5% c) ES at 99% d) ES at 99.5% The manager asks the risk analyst 1 to construct the following scenarios: 1) Using the past five years of data compute the VAR and ES at 99% and 99.5% using historical simulation methodStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Handbook Of Loan Syndications And Trading

Authors: Marsh, Lee Shaiman, Bridget Marsh

2nd Edition

1264258526, 978-1264258529