Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Please answer the # 5-11 multiple choice questions: Textbook: Federal Income Taxation of Corporations and Shareholders, 7th Edition Course: Taxation of Reorganizations & Liquidations 5.

Please answer the # 5-11 multiple choice questions:

Textbook: Federal Income Taxation of Corporations and Shareholders, 7th Edition

Course: Taxation of Reorganizations & Liquidations

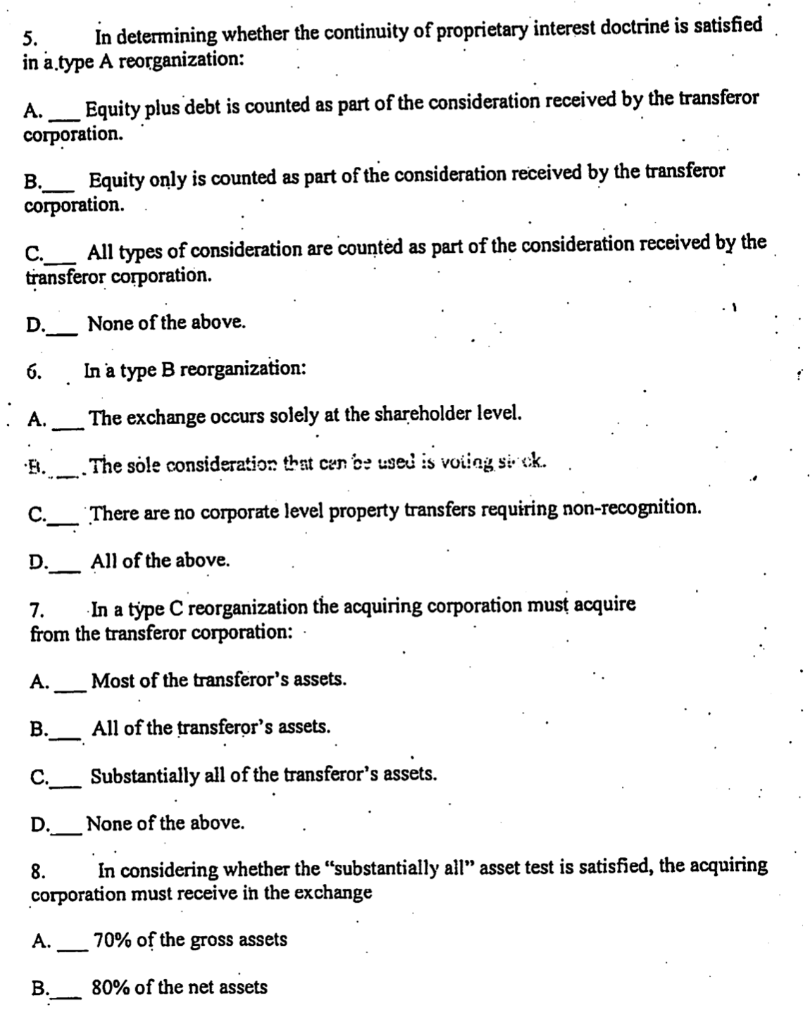

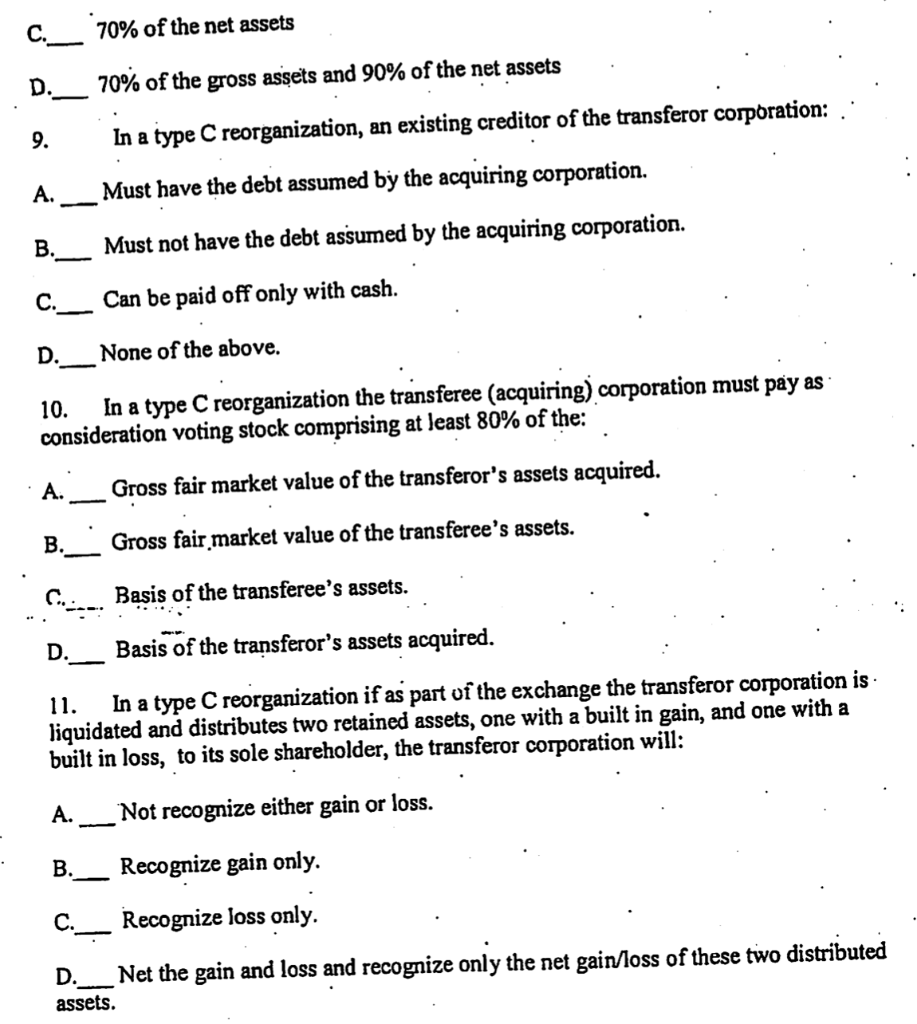

5. in determining whether the continuity of proprietary interest doctrine is satisfied in a.type A reorganization: A. __Equity plus debt is counted as part of the consideration received by the transferor corporation. B._ Equity only is counted as part of the consideration received by the transferor corporation. C._All types of consideration are counted as part of the consideration received by the transferor corporation. D. None of the above. In a type B reorganization: The exchange occurs solely at the shareholder level. B. _ . The sole consideration that can be used is voiing si cik.. c. _ There are no corporate level property transfers requiring non-recognition. D.__ All of the above. 7. In a type C reorganization the acquiring corporation must acquire from the transferor corporation: Most of the transferor's assets. B. _ All of the transferor's assets. C._ Substantially all of the transferor's assets. None of the above. 8. In considering whether the "substantially all" asset test is satisfied, the acquiring corporation must receive in the exchange A. __70% of the gross assets B. _ 80% of the net assets 70% of the net assets D._ 70% of the gross assets and 90% of the net assets 9. In a type C reorganization, an existing creditor of the transferor corporation: .:. A. ___ Must have the debt assumed by the acquiring corporation. B.__ Must not have the debt assumed by the acquiring corporation. c. _ Can be paid off only with cash. D.__ None of the above. 10. In a type C reorganization the transferee (acquiring) corporation must pay as consideration voting stock comprising at least 80% of the: A. _ Gross fair market value of the transferor's assets acquired. Gross fair market value of the transferee's assets. Basis of the transferee's assets. D.__ Basis of the transferor's assets acquired. 11. In a type C reorganization if as part of the exchange the transferor corporation is liquidated and distributes two retained assets, one with a built in gain, and one with a built in loss, to its sole shareholder, the transferor corporation will: A. _ Not recognize either gain or loss. B.__ Recognize gain only. c.__ Recognize loss only. D._ Net the gain and loss and recognize only the net gain/loss of these two distributed assetsStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started