Please answer the critical question 3 and 4

Please answer the critical question 3 and 4

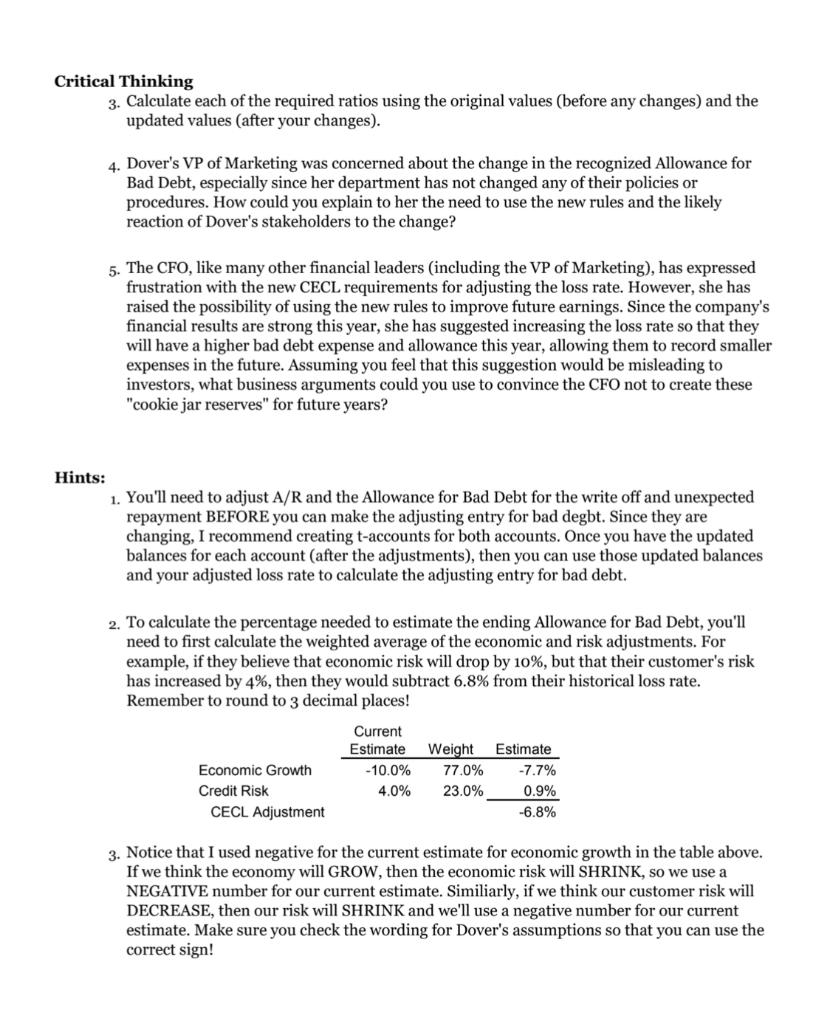

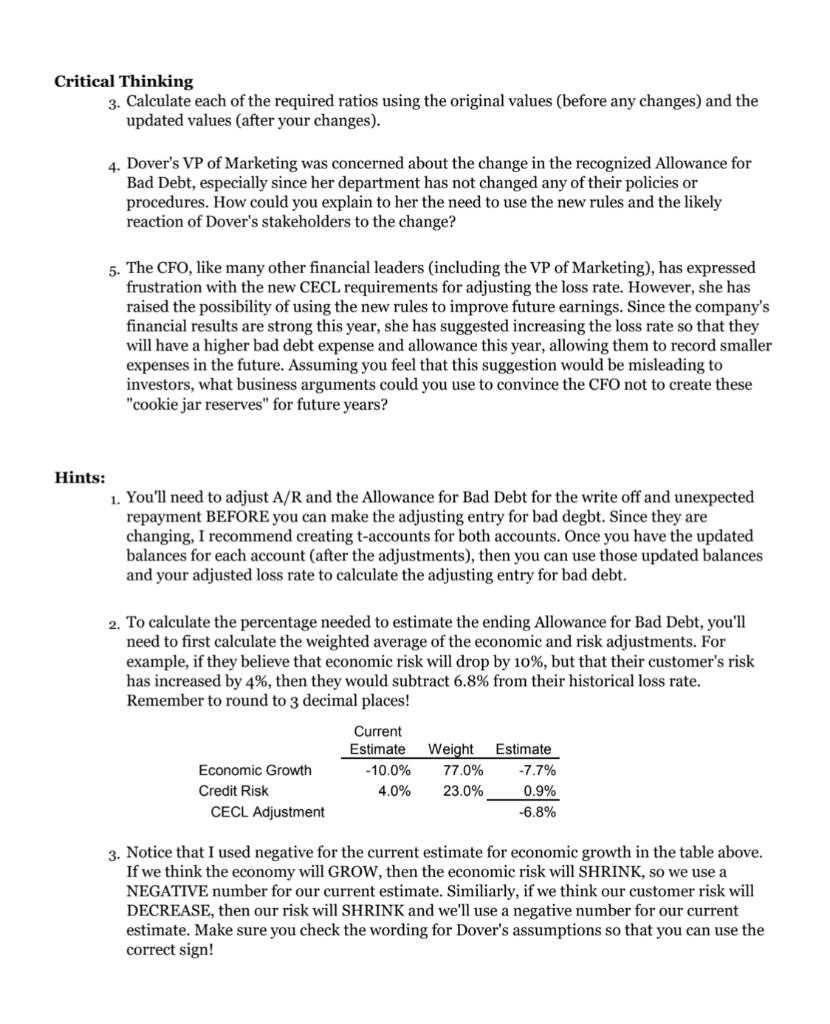

Critical Thinking 3. Calculate each of the required ratios using the original values (before any changes) and the updated values (after your changes). 4. Dover's VP of Marketing was concerned about the change in the recognized Allowance for Bad Debt, especially since her department has not changed any of their policies or procedures. How could you explain to her the need to use the new rules and the likely reaction of Dover's stakeholders to the change? 5. The CFO, like many other financial leaders (including the VP of Marketing), has expressed frustration with the new CECL requirements for adjusting the loss rate. However, she has raised the possibility of using the new rules to improve future earnings. Since the company's financial results are strong this year, she has suggested increasing the loss rate so that they will have a higher bad debt expense and allowance this year, allowing them to record smaller expenses in the future. Assuming you feel that this suggestion would be misleading to investors, what business arguments could you use to convince the CFO not to create these "cookie jar reserves" for future years? Hints: 1. You'll need to adjust A/R and the Allowance for Bad Debt for the write off and unexpected repayment BEFORE you can make the adjusting entry for bad degbt. Since they are changing, I recommend creating t-accounts for both accounts. Once you have the updated balances for each account (after the adjustments), then you can use those updated balances and your adjusted loss rate to calculate the adjusting entry for bad debt. 2. To calculate the percentage needed to estimate the ending Allowance for Bad Debt, you'll need to first calculate the weighted average of the economic and risk adjustments. For example, if they believe that economic risk will drop by 10%, but that their customer's risk has increased by 4%, then they would subtract 6.8% from their historical loss rate. Remember to round to 3 decimal places! 3 Current Estimate - 10.0% 4.0% Economic Growth Credit Risk CECL Adjustment Weight 77.0% 23.0% Estimate -7.7% 0.9% -6.8% 3. Notice that I used negative for the current estimate for economic growth in the table above. If we think the economy will GROW, then the economic risk will SHRINK, so we use a NEGATIVE number for our current estimate. Similiarly, if we think our customer risk will DECREASE, then our risk will SHRINK and we'll use a negative number for our current estimate. Make sure you check the wording for Dover's assumptions so that you can use the correct sign! Intermediate 1 FSR Project Part #4: Receivables Special Note: Now that we have reviewed the basics of the accounting cycle, we are going to simplify things just a bit. Basically, we are going to remove the full COGS calculation and just show one line for COGS (like most companies do in their 10-k). Rather than ask you to redo your work, you will find a new template on our course website in the FSR pt 4 assignment. Please download the template and use it as the basis for the rest of your project Goal: To practice recording accounts receivable, and to observe the effects of write-offs and the estimation of bad debt on the three main financial statements. (See Topic Guides A 5, 6, 42, 43). Information: Under new GAAP (the Current Expected Credit Loss or 'CECL' rules), companies are required to estimate their Allowance for Bad Debt based not only on their historical loss rates but also on current market conditions and future predictions. The accounting process is the same (debit Bad Debt Expense and credit Allowance for Bad Debt), but the estimate is different. Based on the new rules, Dover's management team has decided to adjust their historical rate based on a weighted average of their prediction of general economic risk in their area (weighted at 77%) and on the credit risk of their customers (weighted at 23%), as their loss rate. No adjusting entry has been made this year for bad debt. At the beginning of the year, Dover's collection team reported a historical loss rate of 10.5%. They believe the local economy will shrink by 8.1% and that their average customer's credit risk has decreased by 17.9%. They have also decided to round their calculations to three (3) decimal places for consistency. In addition, the team reported that on December 31, they received word that Harris Company, one of their clients, entered bankruptcy protection, requiring Dover to close their $168,000 account. They also report that they received a $129,000 payment that morning from SSG, Inc. Dover closed SSG's account in July when they believed the company would not be able to pay any of their outstanding bill. No entries have been made for these transactions either. Dover's management would like to know the effect of these adjustments on the following ratios: Quick Ratio ([Cash + Cash Equivalents + net A/R] / Current Liabilities) Accounts Receivable Turnover Ratio (Net Sales / Average net A/R) . Current Ratio Assignment: Calculations 1. Make the appropriate journal entries, if any, to account for the changes in receivables (including any necessary changes to income tax expense). 2. Make any necessary changes to the financial statements. Critical Thinking 3. Calculate each of the required ratios using the original values (before any changes) and the updated values (after your changes). 4. Dover's VP of Marketing was concerned about the change in the recognized Allowance for Bad Debt, especially since her department has not changed any of their policies or procedures. How could you explain to her the need to use the new rules and the likely reaction of Dover's stakeholders to the change? 5. The CFO, like many other financial leaders (including the VP of Marketing), has expressed frustration with the new CECL requirements for adjusting the loss rate. However, she has raised the possibility of using the new rules to improve future earnings. Since the company's financial results are strong this year, she has suggested increasing the loss rate so that they will have a higher bad debt expense and allowance this year, allowing them to record smaller expenses in the future. Assuming you feel that this suggestion would be misleading to investors, what business arguments could you use to convince the CFO not to create these "cookie jar reserves" for future years? Hints: 1. You'll need to adjust A/R and the Allowance for Bad Debt for the write off and unexpected repayment BEFORE you can make the adjusting entry for bad degbt. Since they are changing, I recommend creating t-accounts for both accounts. Once you have the updated balances for each account (after the adjustments), then you can use those updated balances and your adjusted loss rate to calculate the adjusting entry for bad debt. 2. To calculate the percentage needed to estimate the ending Allowance for Bad Debt, you'll need to first calculate the weighted average of the economic and risk adjustments. For example, if they believe that economic risk will drop by 10%, but that their customer's risk has increased by 4%, then they would subtract 6.8% from their historical loss rate. Remember to round to 3 decimal places! 3 Current Estimate - 10.0% 4.0% Economic Growth Credit Risk CECL Adjustment Weight 77.0% 23.0% Estimate -7.7% 0.9% -6.8% 3. Notice that I used negative for the current estimate for economic growth in the table above. If we think the economy will GROW, then the economic risk will SHRINK, so we use a NEGATIVE number for our current estimate. Similiarly, if we think our customer risk will DECREASE, then our risk will SHRINK and we'll use a negative number for our current estimate. Make sure you check the wording for Dover's assumptions so that you can use the correct sign! Critical Thinking 3. Calculate each of the required ratios using the original values (before any changes) and the updated values (after your changes). 4. Dover's VP of Marketing was concerned about the change in the recognized Allowance for Bad Debt, especially since her department has not changed any of their policies or procedures. How could you explain to her the need to use the new rules and the likely reaction of Dover's stakeholders to the change? 5. The CFO, like many other financial leaders (including the VP of Marketing), has expressed frustration with the new CECL requirements for adjusting the loss rate. However, she has raised the possibility of using the new rules to improve future earnings. Since the company's financial results are strong this year, she has suggested increasing the loss rate so that they will have a higher bad debt expense and allowance this year, allowing them to record smaller expenses in the future. Assuming you feel that this suggestion would be misleading to investors, what business arguments could you use to convince the CFO not to create these "cookie jar reserves" for future years? Hints: 1. You'll need to adjust A/R and the Allowance for Bad Debt for the write off and unexpected repayment BEFORE you can make the adjusting entry for bad degbt. Since they are changing, I recommend creating t-accounts for both accounts. Once you have the updated balances for each account (after the adjustments), then you can use those updated balances and your adjusted loss rate to calculate the adjusting entry for bad debt. 2. To calculate the percentage needed to estimate the ending Allowance for Bad Debt, you'll need to first calculate the weighted average of the economic and risk adjustments. For example, if they believe that economic risk will drop by 10%, but that their customer's risk has increased by 4%, then they would subtract 6.8% from their historical loss rate. Remember to round to 3 decimal places! 3 Current Estimate - 10.0% 4.0% Economic Growth Credit Risk CECL Adjustment Weight 77.0% 23.0% Estimate -7.7% 0.9% -6.8% 3. Notice that I used negative for the current estimate for economic growth in the table above. If we think the economy will GROW, then the economic risk will SHRINK, so we use a NEGATIVE number for our current estimate. Similiarly, if we think our customer risk will DECREASE, then our risk will SHRINK and we'll use a negative number for our current estimate. Make sure you check the wording for Dover's assumptions so that you can use the correct sign! Intermediate 1 FSR Project Part #4: Receivables Special Note: Now that we have reviewed the basics of the accounting cycle, we are going to simplify things just a bit. Basically, we are going to remove the full COGS calculation and just show one line for COGS (like most companies do in their 10-k). Rather than ask you to redo your work, you will find a new template on our course website in the FSR pt 4 assignment. Please download the template and use it as the basis for the rest of your project Goal: To practice recording accounts receivable, and to observe the effects of write-offs and the estimation of bad debt on the three main financial statements. (See Topic Guides A 5, 6, 42, 43). Information: Under new GAAP (the Current Expected Credit Loss or 'CECL' rules), companies are required to estimate their Allowance for Bad Debt based not only on their historical loss rates but also on current market conditions and future predictions. The accounting process is the same (debit Bad Debt Expense and credit Allowance for Bad Debt), but the estimate is different. Based on the new rules, Dover's management team has decided to adjust their historical rate based on a weighted average of their prediction of general economic risk in their area (weighted at 77%) and on the credit risk of their customers (weighted at 23%), as their loss rate. No adjusting entry has been made this year for bad debt. At the beginning of the year, Dover's collection team reported a historical loss rate of 10.5%. They believe the local economy will shrink by 8.1% and that their average customer's credit risk has decreased by 17.9%. They have also decided to round their calculations to three (3) decimal places for consistency. In addition, the team reported that on December 31, they received word that Harris Company, one of their clients, entered bankruptcy protection, requiring Dover to close their $168,000 account. They also report that they received a $129,000 payment that morning from SSG, Inc. Dover closed SSG's account in July when they believed the company would not be able to pay any of their outstanding bill. No entries have been made for these transactions either. Dover's management would like to know the effect of these adjustments on the following ratios: Quick Ratio ([Cash + Cash Equivalents + net A/R] / Current Liabilities) Accounts Receivable Turnover Ratio (Net Sales / Average net A/R) . Current Ratio Assignment: Calculations 1. Make the appropriate journal entries, if any, to account for the changes in receivables (including any necessary changes to income tax expense). 2. Make any necessary changes to the financial statements. Critical Thinking 3. Calculate each of the required ratios using the original values (before any changes) and the updated values (after your changes). 4. Dover's VP of Marketing was concerned about the change in the recognized Allowance for Bad Debt, especially since her department has not changed any of their policies or procedures. How could you explain to her the need to use the new rules and the likely reaction of Dover's stakeholders to the change? 5. The CFO, like many other financial leaders (including the VP of Marketing), has expressed frustration with the new CECL requirements for adjusting the loss rate. However, she has raised the possibility of using the new rules to improve future earnings. Since the company's financial results are strong this year, she has suggested increasing the loss rate so that they will have a higher bad debt expense and allowance this year, allowing them to record smaller expenses in the future. Assuming you feel that this suggestion would be misleading to investors, what business arguments could you use to convince the CFO not to create these "cookie jar reserves" for future years? Hints: 1. You'll need to adjust A/R and the Allowance for Bad Debt for the write off and unexpected repayment BEFORE you can make the adjusting entry for bad degbt. Since they are changing, I recommend creating t-accounts for both accounts. Once you have the updated balances for each account (after the adjustments), then you can use those updated balances and your adjusted loss rate to calculate the adjusting entry for bad debt. 2. To calculate the percentage needed to estimate the ending Allowance for Bad Debt, you'll need to first calculate the weighted average of the economic and risk adjustments. For example, if they believe that economic risk will drop by 10%, but that their customer's risk has increased by 4%, then they would subtract 6.8% from their historical loss rate. Remember to round to 3 decimal places! 3 Current Estimate - 10.0% 4.0% Economic Growth Credit Risk CECL Adjustment Weight 77.0% 23.0% Estimate -7.7% 0.9% -6.8% 3. Notice that I used negative for the current estimate for economic growth in the table above. If we think the economy will GROW, then the economic risk will SHRINK, so we use a NEGATIVE number for our current estimate. Similiarly, if we think our customer risk will DECREASE, then our risk will SHRINK and we'll use a negative number for our current estimate. Make sure you check the wording for Dover's assumptions so that you can use the correct sign