Question

Please answer the following: a) Assuming ABC allocated more accurately, which products were incorrectly priced using the traditional costing method? b) What difficulties might result

Please answer the following:

a) Assuming ABC allocated more accurately, which products were incorrectly priced using the traditional costing method?

b) What difficulties might result from incorrectly budgeted products? (Hint: think about how capital resources should be allocated to the most efficient opportunities).

c) Compare assigned cost per product under both methods. Why has activity-based costing changed the total costs assigned to each product?

d) What were two circumstances with traditional and abs costing would likely yield similar or equal overhead cost

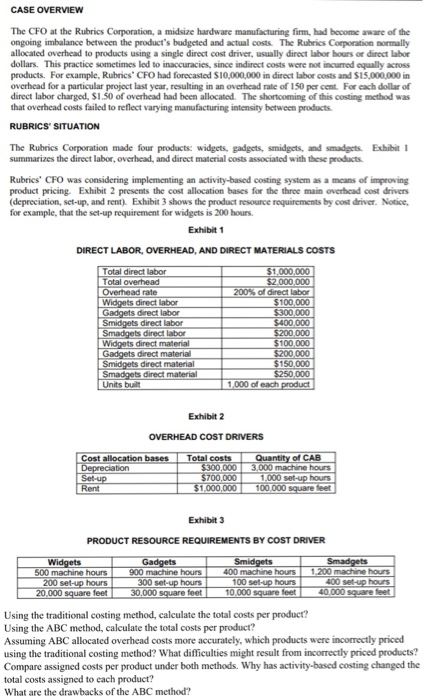

CASE OVERVIEW The CFO at the Rubrics Corporation, a midsize hardware manufacturing firm, had become aware of the ongoing imbalance between the product's budgeted and actual costs The Rubrics Corporation normally allocated overhead to products using a single direct cost driver, usually direct labor hours or direct labor dollars. This practice sometimes led to inaccuracies, since indirect costs were not incurred equally across products. For example, Rubrics' CFO had forecasted $10,000,000 in direct labor costs and $15,000,000 in overhead for a particular project last year, resulting in an overhead rate of 150 per cent. For each dollar of direct labor charged, S1.50 of overhead had been allocated. The shortcoming of this costing method was that overhead costs failed to reflect varying manufacturing intensity between products RUBRICS SITUATION The Rubrics Corporation made four products: widgets, gadgets, smidgets, and smadgets. Exhibit 1 summarizes the direct labor, overhead, and direct material costs associated with these products. Rubrics' CFO was considering implementing an activity-based costing system as a means of improving product pricing. Exhibit 2 presents the cost allocation bases for the three main overhead cost drivers (depreciation, set-up, and rent). Exhibit 3 shows the product resource requirements by cost driver. Notice, for example, that the set-up requirement for widgets is 200 hours. Exhibit 1 DIRECT LABOR, OVERHEAD, AND DIRECT MATERIALS COSTS 1,000,000 000,000 otal direct labor 00,000 $300,000 Gadgets direct labor direct material 100,000 150,000 1,000 of each Exhibit2 OVERHEAD COST DRIVERS Cost costs Quantity of CAB 000 machine hours 00,000 1,000,000 100.000 Exhibit 3 PRODUCT RESOURCE REQUIREMENTS BY COST DRIVER 900 machine hours400 machine hours machine hours machine hours 200 set-up hours feet hours10,000 100 300 400 40.000 feet Using the traditional costing method, calculate the total costs per product? Using the ABC method, calculate the total costs per product? Assuming ABC allocated overhead costs more accurately, which products were incorrectly priced using the traditional costing method? What difficulties might result from incorrectly priced products? Compare assigned costs per product under both methods. Why has activity-based costing changed the total costs assigned to each produet? What are the drawbacks of the ABC methodStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Introduction To Management Accounting With Myaccountinglab And

Authors: Alnoor Bhimani, Charles T. Horngren, Gary L. Sundem, William O. Stratton, Jeff Schatzberg, Dave Burgstahler

1st Edition

1292178116, 978-1292178110