Answered step by step

Verified Expert Solution

Question

1 Approved Answer

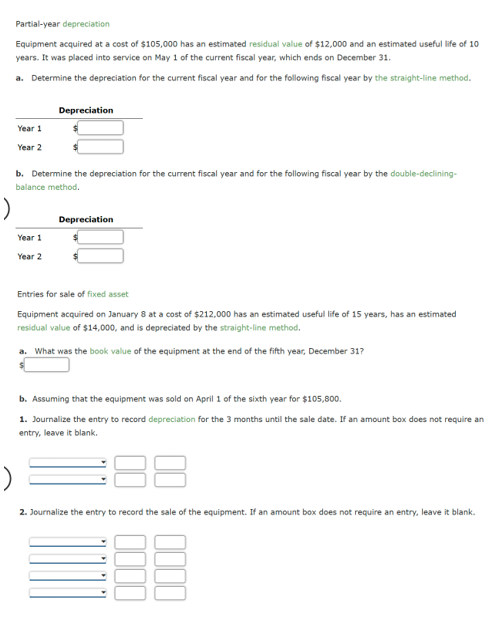

Please answer the following: Partial - year depreciation Equipment acquired at a cost of $ 1 0 5 , 0 0 0 has an estimated

Please answer the following: Partialyear depreciation

Equipment acquired at a cost of $ has an estimated residual value of $ and an estimated useful life of

years. It was placed into service on May of the current fiscal year, which ends on December

a Determine the depreciation for the current fiscal year and for the following fiscal year by the straightline method.

b Determine the depreciation for the current fiscal year and for the following fiscal year by the doubledeclining

balance method.

Depreciation

Entries for sale of fixed asset

Equipment acquired on January at a cost of $ has an estimated useful life of years, has an estimated

residual value of $ and is depreciated by the straightline method,

a What was the book value of the equipment at the end of the fifth year, December

b Assuming that the equipment was sold on April of the sixth year for $

Journalize the entry to record depreciation for the months until the sale date. If an amount box does not require an

entry, leave it blank.

Journalize the entry to record the sale of the equipment. If an amount box does not require an entry, leave it blank. Disposal of fixed asset

Equipment acquired on January at a cost of $ has an estimated useful life of years and an estimated

residual value of $

a What was the annual amount of depreciation for Years using the straightline method of depreciation?

b What was the book value of the equipment on January of Year

$

c Assuming that the equipment was sold on January of Year for $ journalize the entry to record the sale.

If an amount box does not require an entry, leave it blank.

January

d Assuming that the equipment was sold on January of Year for $ instead of $ journalize the

entry to record the sale. If an amount box does not require an entry, leave it blank.

January

:

Depletion entries

Alaska Mining Co acquired mineral rights for $ The mineral deposit is estimated at tons. During

the current year, tons were mined and sold.

a Determine the amount of depletion expense for the current year. Round the depletion rate to two decimal

places.

b Journalize the adjusting entry on December to recognize the depletion expense. If an amount box does not

require an entry, leave it blank.

December Amortization entries

Kleen Company acquired patent rights on January of Year for $ The patent has a useful life equal to its

legal life of years. On January of Year Kleen successfully defended the patent in a lawsuit at a cost of $

a Determine the patent amortization expense for Year ended December

$

b Journalize the adjusting entry on December of Year to recognize the amortization. If an amount box does not

require an entry, leave it blank.

Comparing three depreciation methods

Dexter Industries purchased packaging equipment on January for $ The equipment was expected to have a

useful life of years, or operating hours, and a residual value of $ The equipment was used for

hours during Year hours in Year and hours in Year

Required:

Determine the amount of depreciation expense for the years ending December by a the straightline

method, b the unitsofactivity method, and c the doubledecliningbalance method. Also determine the total

depreciation expense for the years by each method. Do not round intermediate calculations when determining

the depreciation rate. Round the final answers for each year to the nearest whole dollar.

Depreciation Expense

What method yields the highest depreciation expense for Year

What method yields the most depreciation over the year life of the equipment?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Managerial Accounting

Authors: Peter Clarke

2nd Edition

9781907214240