Please Answer the following questions using the case study and the attachments below.

Questions:

- Forecast the income statements and balance sheets for the next 5 years.

- Is $1,575,000 New Techs total need for external financing?

- What is the break-even level of sales in 2001?

- When do you estimate New Tech will hit break-even?

- Make sure you list all assumptions that were necessary to develop your forecast.

- Using the results of the ratio analysis (discussed in Appendix 2.2) along with your pro formas and break-even analysis, can New Tech make a strong case for a loan to cover all its financial needs?

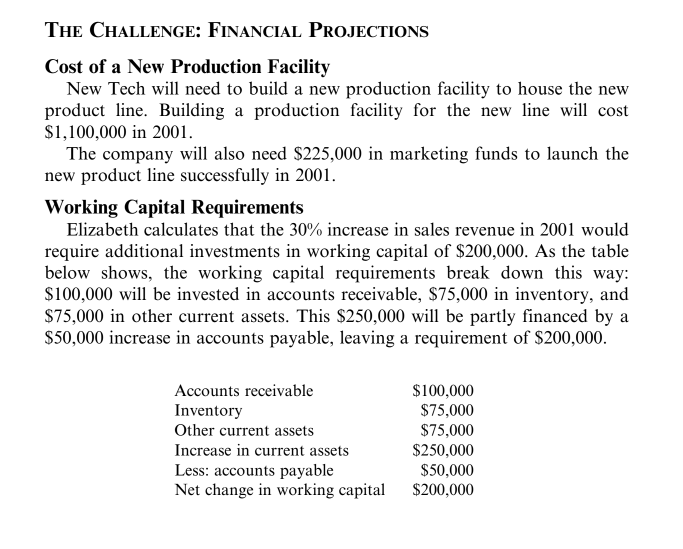

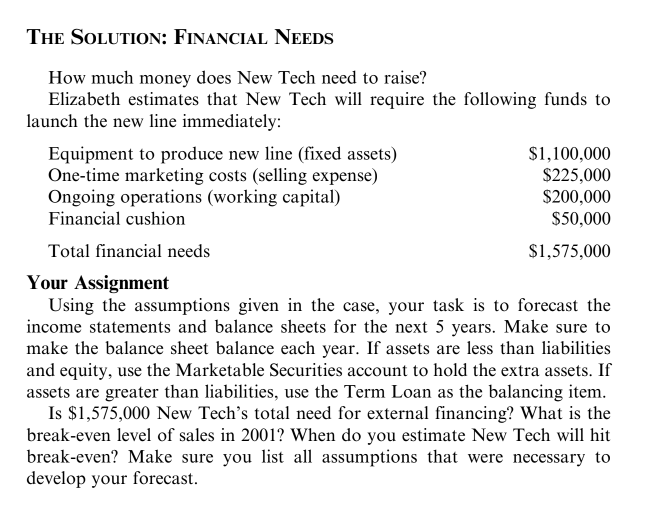

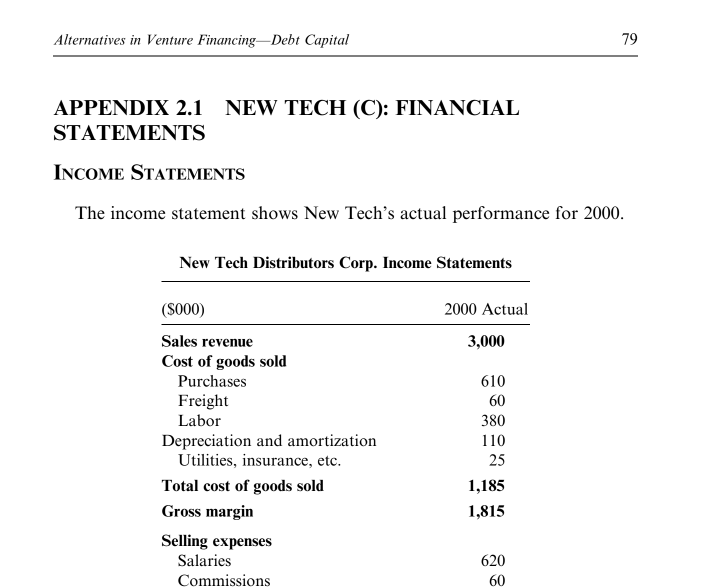

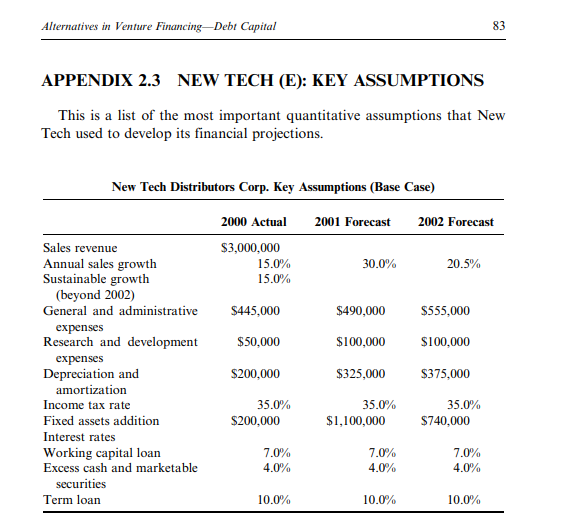

CASE 2.1 NEW TECH (B): HOW MUCH DO THEY NEED? INTRODUCTION How much growth capital will New Tech Distributors need to finance its future growth? Stuart Chip, founder and owner of New Tech Distributors Corp., wants to take his company to a higher level. He is very optimistic about New Tech's expansion program and its capability for producing power modules. He realizes that the key to New Tech's future growth and success is to produce and sell a new line of highly profitable power modules that can provide New Tech with higher margins and improved financial per- formance. He feels that the market for power modules is growing rapidly 76 Alternatives in Venture Financing-Debt Capital and this is the right time to expand. However, Stuart needs growth capital to build new production facilities, market the new line, and fund ongoing operations. See Appendix 2.1 for projected financial statements and other forecasts. THE CHALLENGE: DETERMINING NEEDS Stuart asks Elizabeth Pratt (New Tech's in-house accountant) to take the lead in this project. However, because of the importance and complexity of this proposal, he wants Elizabeth to get as much information as possible from the company's management team to help her in preparing the first draft of the investment proposal. Elizabeth turns to you for assistance in developing the initial forecasts. Elizabeth realizes that potential investors will be asking questions about the assumptions used in producing the financial projections. Investors will also want to explore the assumptions used by management to determine their sales revenue and expenses. She produces a list of key assumptions (see Appendix 2.3). THE CHALLENGE: FINANCIAL PROJECTIONS Cost of a New Production Facility New Tech will need to build a new production facility to house the new product line. Building a production facility for the new line will cost THE CHALLENGE: FINANCIAL PROJECTIONS Cost of a New Production Facility New Tech will need to build a new production facility to house the new product line. Building a production facility for the new line will cost $1,100,000 in 2001. The company will also need $225,000 in marketing funds to launch the new product line successfully in 2001. Working Capital Requirements Elizabeth calculates that the 30% increase in sales revenue in 2001 would require additional investments in working capital of $200,000. As the table below shows, the working capital requirements break down this way: $100,000 will be invested in accounts receivable, $75,000 in inventory, and $75,000 in other current assets. This $250,000 will be partly financed by a $50,000 increase in accounts payable, leaving a requirement of $200,000. Accounts receivable Inventory Other current assets Increase in current assets Less: accounts payable Net change in working capital $100,000 $75,000 $75,000 $250,000 $50,000 $200,000 Alternatives in Venture Financing-Debt Capital 77 Earnings The company paid a dividend of $50,000 in 2000. The amount of divi- dends going for the future has not been determined at this time, so you will need to make an assumption about dividends going forward. Break-Even Point Another element of the proposal that Elizabeth feels is important to calculate is New Tech's break-even point. Before making this calculation, Elizabeth had to discuss with the production manager the level of produc- tion required to cover the fixed and variable costs associated with the new line. To calculate the break-even point, she needs information about the expected unit selling price, expected sales volume, and the marketing vari- able and fixed costs. She also had to go through each item on the income statement and classify all costs under two categories: variable and fixed. After going through this exercise with the management team, she figured out that, in 2001, total variable costs would amount to $1,250,000 and fixed costs, to $2,334,000. She uses the information to determine the amount of revenue that would be required for the company to break even over the forecast period. THE SOLUTION: FINANCIAL NEEDS How much money does New Tech need to raise? Elizabeth estimates that Page ?ch'w40 require the foowing funds to THE SOLUTION: FINANCIAL NEEDS How much money does New Tech need to raise? Elizabeth estimates that New Tech will require the following funds to launch the new line immediately: Equipment to produce new line (fixed assets) $1,100,000 One-time marketing costs (selling expense) $225,000 Ongoing operations (working capital) $200,000 Financial cushion $50,000 Total financial needs $1,575,000 Your Assignment Using the assumptions given in the case, your task is to forecast the income statements and balance sheets for the next 5 years. Make sure to make the balance sheet balance each year. If assets are less than liabilities and equity, use the Marketable Securities account to hold the extra assets. If assets are greater than liabilities, use the Term Loan as the balancing item. Is $1,575,000 New Tech's total need for external financing? What is the break-even level of sales in 2001? When do you estimate New Tech will hit break-even? Make sure you list all assumptions that were necessary to develop your forecast. 78 Alternatives in Venture Financing-Debt Capital Using the results of the ratio analysis (discussed in Appendix 2.2) along with your pro formas and break-even analysis, can New Tech make a strong case for a loan to cover all its financial needs? Alternatives in Venture FinancingDebt Capital 79 APPENDIX 2.1 NEW TECH (C): FINANCIAL STATEMENTS INCOME STATEMENTS The income statement shows New Tech's actual performance for 2000. New Tech Distributors Corp. Income Statements 2000 Actual 3,000 (5000) Sales revenue Cost of goods sold Purchases Freight Labor Depreciation and amortization Utilities, insurance, etc. Total cost of goods sold Gross margin Selling expenses Salaries Commissions 610 60 380 110 25 1,185 1,815 620 60 60 380 110 25 1,185 1,815 620 60 Freight Labor Depreciation and amortization Utilities, insurance, etc. Total cost of goods sold Gross margin Selling expenses Salaries Commissions Travel Advertising Depreciation and amortization Special promotional program Total selling expenses Administrative expenses Salaries Leasing Depreciation and amortization Research and development Total administrative expenses Total operating costs Operating income Interest income Interest charges Income before taxes Income taxes Income after taxes 60 70 30 17 857 395 50 60 50 555 1,412 403 5 95 313 109 204 80 Alternatives in Venture Financing-Debt Capital New Tech Distributors Corp. Statements of Retained Earnings ($000) Retained earnings (beginning of year) Net earnings for the year Subtotal Dividends Retained earnings (end of year) 2000 Actual 500 204 704 50 654 BALANCE SHEETS The balance sheet shows New Tech's financial structure at the end of 2000. New Tech Distributors Corp. Balance Sheets (5000) 2000 Actual Assets Current assets New Tech Distributors Corp. Balance Sheets (5000) 2000 Actual 20 100 60 450 350 70 84 1,134 Assets Current assets Cash Marketable securities Prepaid expenses Accounts receivable Inventory Other assets Supplies, etc. Total current assets Capital assets Gross capital assets Accumulated depreciation Total net capital assets Goodwill Other assets Total assets Current liabilities Accounts payable Term loan Working capital loan Accruals Current portion of long-term debt 1,775 -560 1,215 45 5 2,399 550 125 50 60 30 Alternatives in Venire Fixing Dah Comital 81 SIS 400 1.215 Total current liabilities Total long-term debes Total liabilities Owners' equity Capital shares Retained earnings Total owners' equity Total liabilities and owners' equity 530 654 1.184 2.399 APPENDIX 2.2 NEW TECH (D): FINANCIAL RATIOS One way to define and measure a company's performance is with finan. cial ratios. Calculate the following financial ratios for each year in the forecast. Is New Tech's performance improving or deteriorating? Use the industry averages in Table 2.2, and the starting point in 2000 as your basis for comparison LIQUIDITY RATIOS Does the company have sufficient cash and near cash to pay its bills and payroll on time? 2000 Actual Liquidity Ratios Current ratio (times) 1.39 Quick ratio (times) 0.96 Sales/accounts receivable 6.67 COGS inventory 3:39 COGS accounts payable 2.15 Sales/working capital LEVERAGE RATIOS What is the proportion of a company's debt versus equity? These ratios display the methods and sources of financing used in acquiring assets and their impact on the earnings available to shareholders. Is the company accumulating too much debt as it moves forward? Note that we can assess the impact of debt by focusing on the income statement as well as the balance sheet. 82 Alternatives in Vantare Financing Debt Capital 2000 Actual Leverage Rates Total debt total assets (percent) 50.63% Long-term debt/equity times) EBIT interest expense PROFITABILITY RATIOS Is the business generating a sufficient return on its investments? These ratios show the relationship between profit and revenue generated, resources employed (assets), and shareholders' equity. Do the company's profitability ratios look adequate to you! 2000 Actual Profitability Ratios % Gross margin to sales 60.50 Operating income sales 13.43 Protit before taxes/sales 10.43 Protit before tax total assets (percent) 13.05 Protit before tax/equity 26.44 Alternatives in Venture FinancingDebt Capital 83 APPENDIX 2.3 NEW TECH (E): KEY ASSUMPTIONS This is a list of the most important quantitative assumptions that New Tech used to develop its financial projections. New Tech Distributors Corp. Key Assumptions (Base Case) 2000 Actual 2001 Forecast 2002 Forecast Sales revenue $3,000,000 Annual sales growth 15.0% 30.0% 20.5% Sustainable growth 15.0% (beyond 2002) General and administrative $445,000 $490,000 $555,000 expenses Research and development $50,000 $100,000 $100,000 expenses Depreciation and $200,000 $325,000 $375,000 amortization Income tax rate 35.0% 35.0% 35.0% Fixed assets addition $200,000 $1,100,000 $740,000 Interest rates Working capital loan 7.0% 7.0% 7.0% Excess cash and marketable 4.0% 4.0% 4.0% securities Term loan 10.0% 10.0% 10.0% CASE 2.1 NEW TECH (B): HOW MUCH DO THEY NEED? INTRODUCTION How much growth capital will New Tech Distributors need to finance its future growth? Stuart Chip, founder and owner of New Tech Distributors Corp., wants to take his company to a higher level. He is very optimistic about New Tech's expansion program and its capability for producing power modules. He realizes that the key to New Tech's future growth and success is to produce and sell a new line of highly profitable power modules that can provide New Tech with higher margins and improved financial per- formance. He feels that the market for power modules is growing rapidly 76 Alternatives in Venture Financing-Debt Capital and this is the right time to expand. However, Stuart needs growth capital to build new production facilities, market the new line, and fund ongoing operations. See Appendix 2.1 for projected financial statements and other forecasts. THE CHALLENGE: DETERMINING NEEDS Stuart asks Elizabeth Pratt (New Tech's in-house accountant) to take the lead in this project. However, because of the importance and complexity of this proposal, he wants Elizabeth to get as much information as possible from the company's management team to help her in preparing the first draft of the investment proposal. Elizabeth turns to you for assistance in developing the initial forecasts. Elizabeth realizes that potential investors will be asking questions about the assumptions used in producing the financial projections. Investors will also want to explore the assumptions used by management to determine their sales revenue and expenses. She produces a list of key assumptions (see Appendix 2.3). THE CHALLENGE: FINANCIAL PROJECTIONS Cost of a New Production Facility New Tech will need to build a new production facility to house the new product line. Building a production facility for the new line will cost THE CHALLENGE: FINANCIAL PROJECTIONS Cost of a New Production Facility New Tech will need to build a new production facility to house the new product line. Building a production facility for the new line will cost $1,100,000 in 2001. The company will also need $225,000 in marketing funds to launch the new product line successfully in 2001. Working Capital Requirements Elizabeth calculates that the 30% increase in sales revenue in 2001 would require additional investments in working capital of $200,000. As the table below shows, the working capital requirements break down this way: $100,000 will be invested in accounts receivable, $75,000 in inventory, and $75,000 in other current assets. This $250,000 will be partly financed by a $50,000 increase in accounts payable, leaving a requirement of $200,000. Accounts receivable Inventory Other current assets Increase in current assets Less: accounts payable Net change in working capital $100,000 $75,000 $75,000 $250,000 $50,000 $200,000 Alternatives in Venture Financing-Debt Capital 77 Earnings The company paid a dividend of $50,000 in 2000. The amount of divi- dends going for the future has not been determined at this time, so you will need to make an assumption about dividends going forward. Break-Even Point Another element of the proposal that Elizabeth feels is important to calculate is New Tech's break-even point. Before making this calculation, Elizabeth had to discuss with the production manager the level of produc- tion required to cover the fixed and variable costs associated with the new line. To calculate the break-even point, she needs information about the expected unit selling price, expected sales volume, and the marketing vari- able and fixed costs. She also had to go through each item on the income statement and classify all costs under two categories: variable and fixed. After going through this exercise with the management team, she figured out that, in 2001, total variable costs would amount to $1,250,000 and fixed costs, to $2,334,000. She uses the information to determine the amount of revenue that would be required for the company to break even over the forecast period. THE SOLUTION: FINANCIAL NEEDS How much money does New Tech need to raise? Elizabeth estimates that Page ?ch'w40 require the foowing funds to THE SOLUTION: FINANCIAL NEEDS How much money does New Tech need to raise? Elizabeth estimates that New Tech will require the following funds to launch the new line immediately: Equipment to produce new line (fixed assets) $1,100,000 One-time marketing costs (selling expense) $225,000 Ongoing operations (working capital) $200,000 Financial cushion $50,000 Total financial needs $1,575,000 Your Assignment Using the assumptions given in the case, your task is to forecast the income statements and balance sheets for the next 5 years. Make sure to make the balance sheet balance each year. If assets are less than liabilities and equity, use the Marketable Securities account to hold the extra assets. If assets are greater than liabilities, use the Term Loan as the balancing item. Is $1,575,000 New Tech's total need for external financing? What is the break-even level of sales in 2001? When do you estimate New Tech will hit break-even? Make sure you list all assumptions that were necessary to develop your forecast. 78 Alternatives in Venture Financing-Debt Capital Using the results of the ratio analysis (discussed in Appendix 2.2) along with your pro formas and break-even analysis, can New Tech make a strong case for a loan to cover all its financial needs? Alternatives in Venture FinancingDebt Capital 79 APPENDIX 2.1 NEW TECH (C): FINANCIAL STATEMENTS INCOME STATEMENTS The income statement shows New Tech's actual performance for 2000. New Tech Distributors Corp. Income Statements 2000 Actual 3,000 (5000) Sales revenue Cost of goods sold Purchases Freight Labor Depreciation and amortization Utilities, insurance, etc. Total cost of goods sold Gross margin Selling expenses Salaries Commissions 610 60 380 110 25 1,185 1,815 620 60 60 380 110 25 1,185 1,815 620 60 Freight Labor Depreciation and amortization Utilities, insurance, etc. Total cost of goods sold Gross margin Selling expenses Salaries Commissions Travel Advertising Depreciation and amortization Special promotional program Total selling expenses Administrative expenses Salaries Leasing Depreciation and amortization Research and development Total administrative expenses Total operating costs Operating income Interest income Interest charges Income before taxes Income taxes Income after taxes 60 70 30 17 857 395 50 60 50 555 1,412 403 5 95 313 109 204 80 Alternatives in Venture Financing-Debt Capital New Tech Distributors Corp. Statements of Retained Earnings ($000) Retained earnings (beginning of year) Net earnings for the year Subtotal Dividends Retained earnings (end of year) 2000 Actual 500 204 704 50 654 BALANCE SHEETS The balance sheet shows New Tech's financial structure at the end of 2000. New Tech Distributors Corp. Balance Sheets (5000) 2000 Actual Assets Current assets New Tech Distributors Corp. Balance Sheets (5000) 2000 Actual 20 100 60 450 350 70 84 1,134 Assets Current assets Cash Marketable securities Prepaid expenses Accounts receivable Inventory Other assets Supplies, etc. Total current assets Capital assets Gross capital assets Accumulated depreciation Total net capital assets Goodwill Other assets Total assets Current liabilities Accounts payable Term loan Working capital loan Accruals Current portion of long-term debt 1,775 -560 1,215 45 5 2,399 550 125 50 60 30 Alternatives in Venire Fixing Dah Comital 81 SIS 400 1.215 Total current liabilities Total long-term debes Total liabilities Owners' equity Capital shares Retained earnings Total owners' equity Total liabilities and owners' equity 530 654 1.184 2.399 APPENDIX 2.2 NEW TECH (D): FINANCIAL RATIOS One way to define and measure a company's performance is with finan. cial ratios. Calculate the following financial ratios for each year in the forecast. Is New Tech's performance improving or deteriorating? Use the industry averages in Table 2.2, and the starting point in 2000 as your basis for comparison LIQUIDITY RATIOS Does the company have sufficient cash and near cash to pay its bills and payroll on time? 2000 Actual Liquidity Ratios Current ratio (times) 1.39 Quick ratio (times) 0.96 Sales/accounts receivable 6.67 COGS inventory 3:39 COGS accounts payable 2.15 Sales/working capital LEVERAGE RATIOS What is the proportion of a company's debt versus equity? These ratios display the methods and sources of financing used in acquiring assets and their impact on the earnings available to shareholders. Is the company accumulating too much debt as it moves forward? Note that we can assess the impact of debt by focusing on the income statement as well as the balance sheet. 82 Alternatives in Vantare Financing Debt Capital 2000 Actual Leverage Rates Total debt total assets (percent) 50.63% Long-term debt/equity times) EBIT interest expense PROFITABILITY RATIOS Is the business generating a sufficient return on its investments? These ratios show the relationship between profit and revenue generated, resources employed (assets), and shareholders' equity. Do the company's profitability ratios look adequate to you! 2000 Actual Profitability Ratios % Gross margin to sales 60.50 Operating income sales 13.43 Protit before taxes/sales 10.43 Protit before tax total assets (percent) 13.05 Protit before tax/equity 26.44 Alternatives in Venture FinancingDebt Capital 83 APPENDIX 2.3 NEW TECH (E): KEY ASSUMPTIONS This is a list of the most important quantitative assumptions that New Tech used to develop its financial projections. New Tech Distributors Corp. Key Assumptions (Base Case) 2000 Actual 2001 Forecast 2002 Forecast Sales revenue $3,000,000 Annual sales growth 15.0% 30.0% 20.5% Sustainable growth 15.0% (beyond 2002) General and administrative $445,000 $490,000 $555,000 expenses Research and development $50,000 $100,000 $100,000 expenses Depreciation and $200,000 $325,000 $375,000 amortization Income tax rate 35.0% 35.0% 35.0% Fixed assets addition $200,000 $1,100,000 $740,000 Interest rates Working capital loan 7.0% 7.0% 7.0% Excess cash and marketable 4.0% 4.0% 4.0% securities Term loan 10.0% 10.0% 10.0%