Please answer the question on the picture

Formula provided

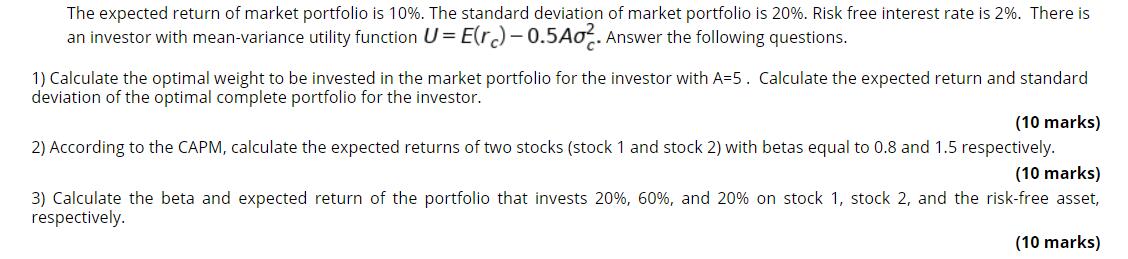

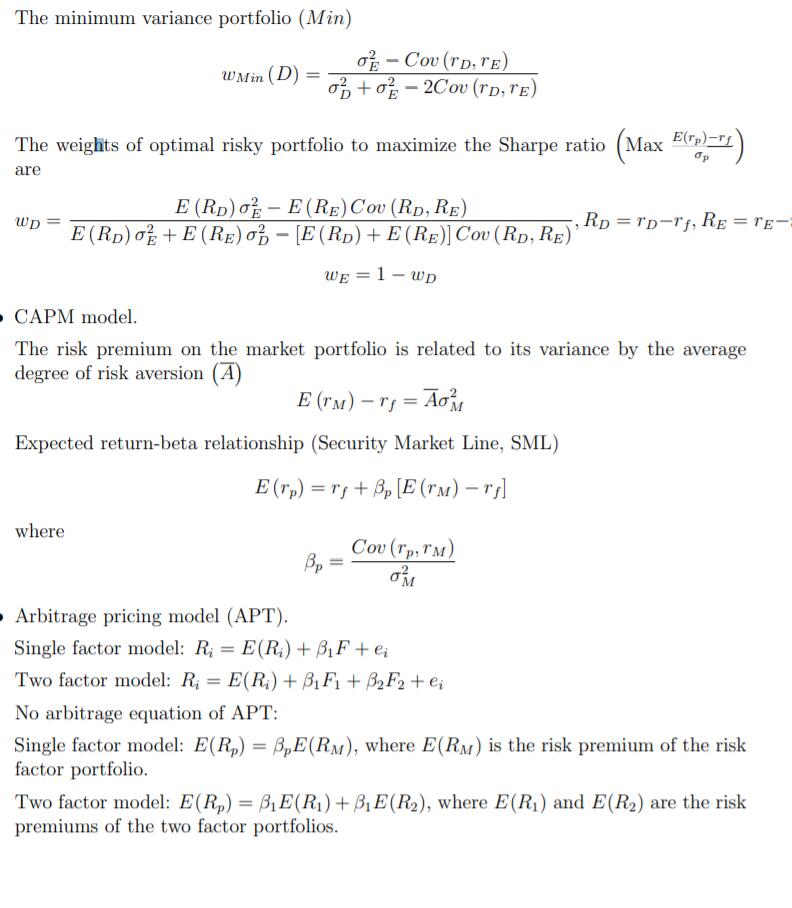

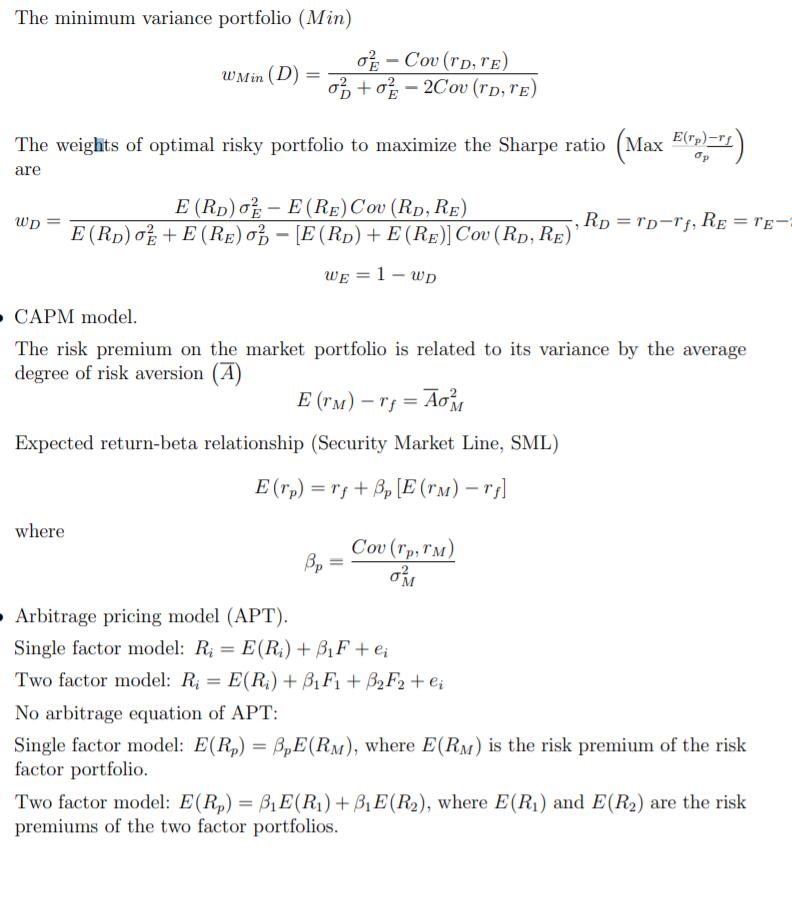

The expected return of market portfolio is '| 0%. The standard deviation of market portfolio is 20%. Risk free interest rate is 2%. There is an investor with meanvariance utility function U = EOE) 0.540%. Answer the following questions. '1) Calculate the optimal weight to be invested in the market portfolio for the investor with A=5. Calculate the expected return and standard deviation ofthe optimal complete portfolio for the investor. {10 marks) 2) According to the CAPM, calculate the expected returns of two stocks (stock'i and stock 2) with betas equal to 0.8 and 1.5 respectively. {10 marks} 3) Calculate the beta and expected return of the portfolio that invests 20%, 60%, and 20% on stock 1, stock 2, and the riskfree asset, respectively. {1 0 marks) Formulas . The percentage margin for buying on margin is Margin= Equity in account Value of securities The percentage maring for short sales is Margin= Equity Vaule of securities owed" Net asset value (NAV) is NAV= Market value of asset minus liabilities Shares Outstanding Mutual Fund Return is Rate of return=WAVi-NAVo+Income and capital gain distributions NAVo . Holding period return (HPR): HPR = Ending price of a share-Beginning price + Cash dividend Beginning price . The expected return (E (r)) and variance (?) : E (r) = Ep(s)r (s) , 2 = Ep(s) [r (s) - E(r)] where p(s) is the probability of each scenario and r (s) is the holding period return in each scenario. . Both the expected return and variance grow at a rate of investment horizon. Risk premium . Sharpe ratio Standard deviation of excess return . Portfolio (C) by one risk free asset (f) with weight (1 -y) and one risky asset (P) with weight y : E(rc) = rs+ y [E (rp) - rs] oc = yop The Capital Allocation Line (CAL) E( rc) = rs + [E (TP) - rigc OP The optimal choice for an investor with utility function U = E (rc) - } Act is y* = E(TP) - If Aop . Portfolio (P) by one low risk asset (D) with weight wp and one high risk asset (E) with weight we = 1 - wp E(TP) = WDE (TD) + WEE (TE) op = wpop + who?- BOE + 2WDWECOU (TD, TE) = 1202 + 2WDWEPODGE 30% + WEOF+ where p is the correlation beween ro and rE.The minimum variance portfolio (Min) OF - Cov (rD, TE) WMin (D) = 62 + 03 - 2Cou (rD, TE) The weights of optimal risky portfolio to maximize the Sharpe ratio (Max (";)- are E (RD) OF - E(RE) Cov (RD, RE) WP = E(RD) of + E(RE) OB - [E (RD) + E(RE)] Cov ( RD, RE) RD = TD-TJ, RE = TE- WE=1 - WD CAPM model. The risk premium on the market portfolio is related to its variance by the average degree of risk aversion (A) E(TM) - TS = AOM Expected return-beta relationship (Security Market Line, SML) E(rp) = ry + Bp [E(rM) - rs] where Bp = Cov (TP, TM) OM Arbitrage pricing model (APT). Single factor model: R. = E(Ri) + BFte; Two factor model: Ri = E(R;) + Bi F1 + B2 F2 + ei No arbitrage equation of APT: Single factor model: E(Rp) = BpE(RM), where E(RM) is the risk premium of the risk factor portfolio. Two factor model: E(Rp) = BIE(R1) + BIE(R2), where E(R,) and E(R2) are the risk premiums of the two factor portfolios