Answered step by step

Verified Expert Solution

Question

1 Approved Answer

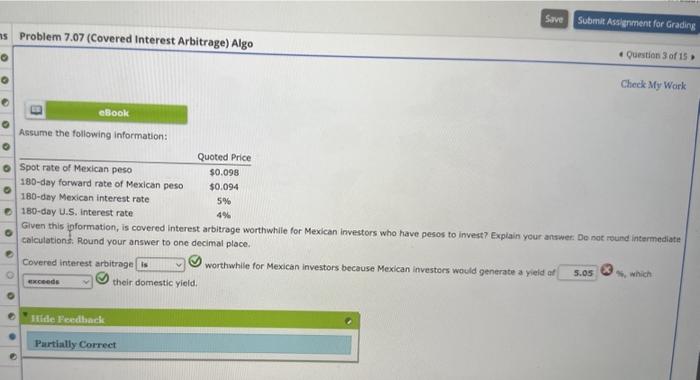

please answer the questions below. each picture has a different picture Assume the following information: Glven this information, is covered interest arbitrage worthwhile for Mexican

please answer the questions below. each picture has a different picture

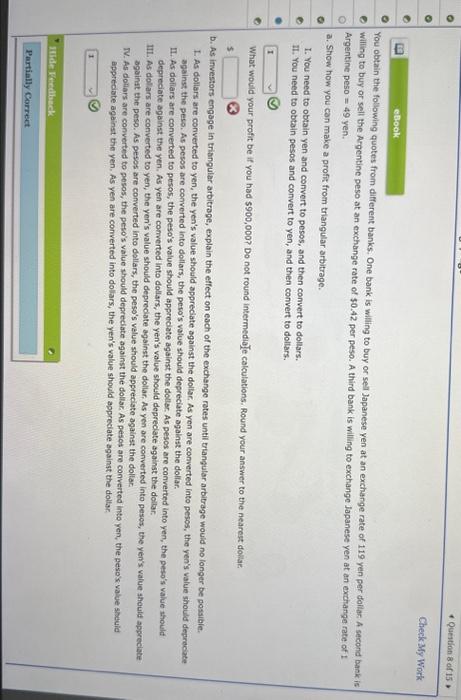

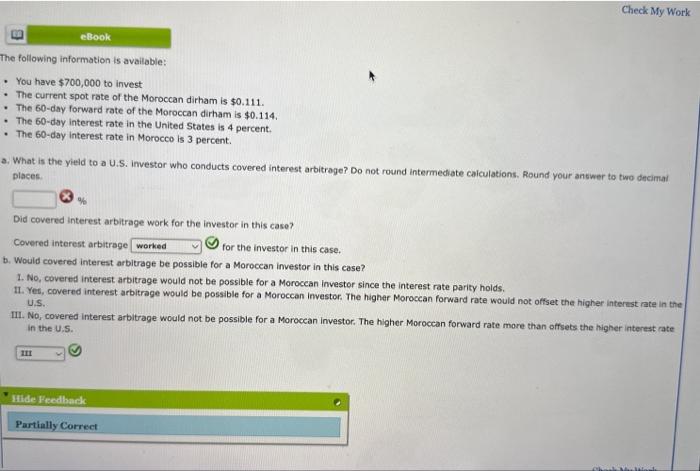

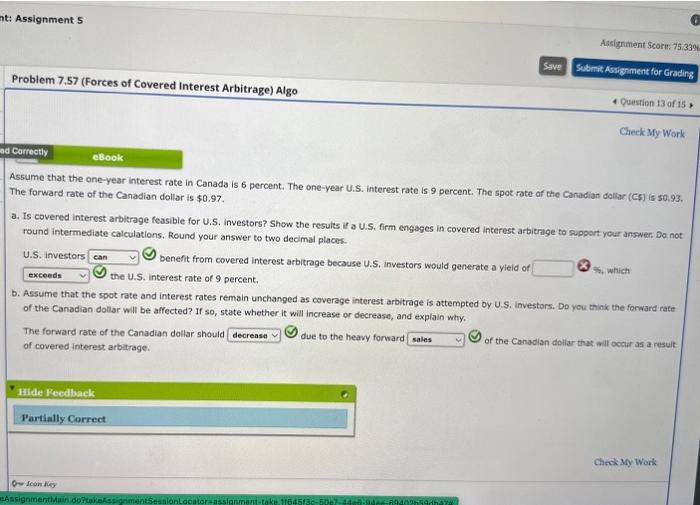

Assume the following information: Glven this information, is covered interest arbitrage worthwhile for Mexican investors who have pesos to invest? Explain your answer De not round interthediate calculations. Round your answer to one decimal place, Covered inserest aroitroge worthwhile for Mexican investors because Mexican investors would generate a yeid of their domestic yield. You obtain the following quotes from different banks. One bank is willing to buy or sell Japanese yen at an exchange rate of 119 yen per doilas A second bank is willing to buy or sell the Argentine peso at an exchange rate of $0.42 per peso. A third bank is willing to exchange Japanese yen at an exchange rate of I Argentine peso =49 yen. a. Show how you can make a profic from triangular arbitrage. I. You need to obtain yen and convert to pesos, and then convert to doliars. II. You need to obtain pesos and convert to yen, and then convert to doltars. What would your profit be if you had 5900,000? Do not round intermediole calculations. Round your answer to the nearest doliae 5 D. As investors engage in triangular arbitrage, explain the effect on each of the exchange rates until trangular arbitrage would no longer be possibie. 1. As dollars are converted to yen, the yen's value should appreciate against the dollar. As yen are converted into pesos, the yen's value should depreciate against the peso. As pesos are converted into dollars, the peso's value should depreciate against the dollar. II. As doliars are converted to pesos, the peso's value should appreciate against the dollar. As pesos are converted into yen, the peso's value should depreciate against the yen. As yen are comverted into dollars, the yen's value should depreclate against the dollar. III. As dollars are converted to yen, the yen's value should depreciate against the dollar, As yen are converted into pesos, the yen's value should appreciate againat the peso. As pesos are converted into dollars, the pess's velue should appreciate against the dollat W. As dollars are converted to pesos, the peso's value should depreciate against the dollar. As pesos are converted into yen, the pesos value sheuld appreciate against the yen. As yen are converted into doliars, the yen's value should appreciate against the dollar. The following information is available: - You have $700,000 to invest - The current spot rate of the Moroccan dirham is $0.111. - The 60 -day forward rate of the Moroccan dirham is $0.114, - The 60 -day interest rate in the United States is 4 percent. - The 60-day interest rate in Morocco is 3 percent. a. What is the yield to a U.S. imvestor who conducts covered interest arbitrage? Do not round intermediate caiculations, Round your ancwer to two decimai places. Did covered interest arbitrage work for the investor in this case? Covered interest arbitrage for the investor in this case. b. Would covered interest arbitrage be possible for a Moreccan investor in this case? 1. No, covered interest arbitrage would not be possible for a Moroccan investor since the interest rate parity holds. 1I. Yes, covered interest arbitrage would be possible for a Moroccan investor. The higher Moroccan forward rate would not offset the higher inteizst rate in the U,S. 111. No, covered interest arbitrage would not be possible for a Morocean investor. The higher Moroccan forward rate more than offsets the higher interest rate in the U.5. Assignment 5 Problem 7.57 (Forces of Covered Interest Arbitrage) Algo Asclgniment Scorm: 75. The forward rate of the Canadian dollar is $0.97. a. Is covered interest arbitrage feasible for U.S. investors? Show the results it a U.S. firm engages in covered interest arbitrige to support your answer. Do not round intermediate calculations. Round your answer to two decimal places. U.S. investors benefit from covered interest arbitrage because U.S, investors would generate a yield of the U.S. interest rate of 9 percent. b. Assume that the spot rate and interest rates remain unchanged as coverage interest arbitrage is attempted by U.S. investors. Do you think the forward rate of the Canadian dollar will be affected? If so, state whether it will increase or decrease, and explain why, The forward rate of the Canadian dollar should of covered interest arbitrage. due to the heavy forward of the Canadian dollar that will occir as a resuit. Assume the following information: Glven this information, is covered interest arbitrage worthwhile for Mexican investors who have pesos to invest? Explain your answer De not round interthediate calculations. Round your answer to one decimal place, Covered inserest aroitroge worthwhile for Mexican investors because Mexican investors would generate a yeid of their domestic yield. You obtain the following quotes from different banks. One bank is willing to buy or sell Japanese yen at an exchange rate of 119 yen per doilas A second bank is willing to buy or sell the Argentine peso at an exchange rate of $0.42 per peso. A third bank is willing to exchange Japanese yen at an exchange rate of I Argentine peso =49 yen. a. Show how you can make a profic from triangular arbitrage. I. You need to obtain yen and convert to pesos, and then convert to doliars. II. You need to obtain pesos and convert to yen, and then convert to doltars. What would your profit be if you had 5900,000? Do not round intermediole calculations. Round your answer to the nearest doliae 5 D. As investors engage in triangular arbitrage, explain the effect on each of the exchange rates until trangular arbitrage would no longer be possibie. 1. As dollars are converted to yen, the yen's value should appreciate against the dollar. As yen are converted into pesos, the yen's value should depreciate against the peso. As pesos are converted into dollars, the peso's value should depreciate against the dollar. II. As doliars are converted to pesos, the peso's value should appreciate against the dollar. As pesos are converted into yen, the peso's value should depreciate against the yen. As yen are comverted into dollars, the yen's value should depreclate against the dollar. III. As dollars are converted to yen, the yen's value should depreciate against the dollar, As yen are converted into pesos, the yen's value should appreciate againat the peso. As pesos are converted into dollars, the pess's velue should appreciate against the dollat W. As dollars are converted to pesos, the peso's value should depreciate against the dollar. As pesos are converted into yen, the pesos value sheuld appreciate against the yen. As yen are converted into doliars, the yen's value should appreciate against the dollar. The following information is available: - You have $700,000 to invest - The current spot rate of the Moroccan dirham is $0.111. - The 60 -day forward rate of the Moroccan dirham is $0.114, - The 60 -day interest rate in the United States is 4 percent. - The 60-day interest rate in Morocco is 3 percent. a. What is the yield to a U.S. imvestor who conducts covered interest arbitrage? Do not round intermediate caiculations, Round your ancwer to two decimai places. Did covered interest arbitrage work for the investor in this case? Covered interest arbitrage for the investor in this case. b. Would covered interest arbitrage be possible for a Moreccan investor in this case? 1. No, covered interest arbitrage would not be possible for a Moroccan investor since the interest rate parity holds. 1I. Yes, covered interest arbitrage would be possible for a Moroccan investor. The higher Moroccan forward rate would not offset the higher inteizst rate in the U,S. 111. No, covered interest arbitrage would not be possible for a Morocean investor. The higher Moroccan forward rate more than offsets the higher interest rate in the U.5. Assignment 5 Problem 7.57 (Forces of Covered Interest Arbitrage) Algo Asclgniment Scorm: 75. The forward rate of the Canadian dollar is $0.97. a. Is covered interest arbitrage feasible for U.S. investors? Show the results it a U.S. firm engages in covered interest arbitrige to support your answer. Do not round intermediate calculations. Round your answer to two decimal places. U.S. investors benefit from covered interest arbitrage because U.S, investors would generate a yield of the U.S. interest rate of 9 percent. b. Assume that the spot rate and interest rates remain unchanged as coverage interest arbitrage is attempted by U.S. investors. Do you think the forward rate of the Canadian dollar will be affected? If so, state whether it will increase or decrease, and explain why, The forward rate of the Canadian dollar should of covered interest arbitrage. due to the heavy forward of the Canadian dollar that will occir as a resuit Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Advances In Financial Machine Learning

Authors: Marcos Lopez De Prado

1st Edition

1119482089, 978-1119482086